Question

Krishna was determined not to be one of the millions too frail to work, too poor to retire. Armed with his recently acquired knowledge of

Krishna was determined not to be one of the millions too frail to work, too poor to retire. Armed with his recently acquired knowledge of the time value of money, he set his Kleenex box aside and reached for the Chapter 4 & 5 Template that he received from his Financial Management course at NYU. He intends to have a plan and is determined to start the first day of 2022.

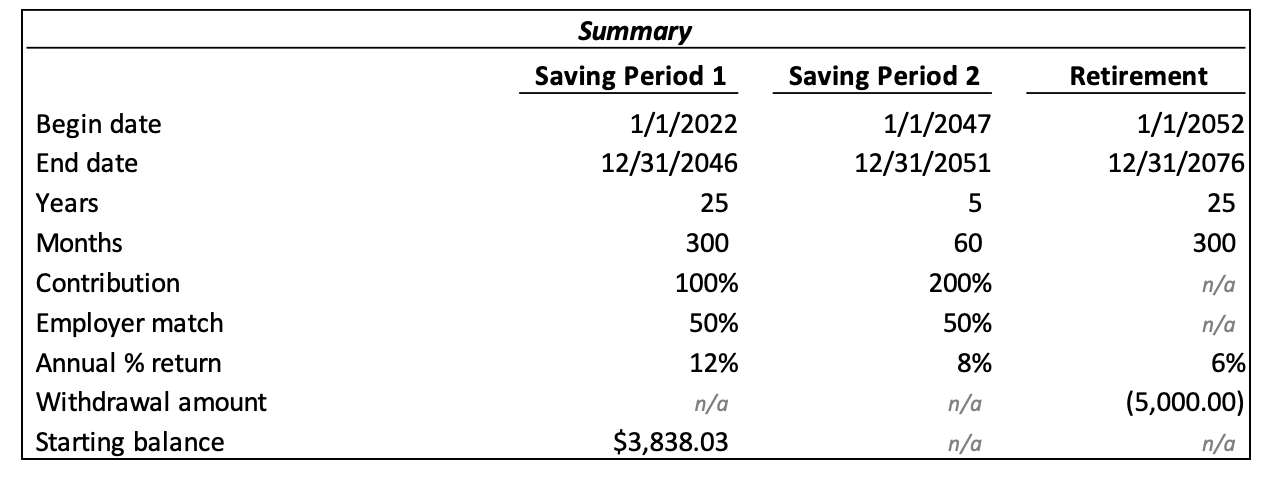

Any plan or forecast requires certain assumptions, he figures, and his first assumption was that he will retire early at the age of 60. Krishna will be 30 years old at the beginning of 2022. In retirement, he wants to be able to withdraw $5,000 from his savings account each last day of the month for the 25 years of his retirement (beginning January 1, 2052 through and including December 31, 2076).

His plan is to use a 401(k) account. He logs into his 401(k) account to realize that he will have a mere $3,838.03 in his account at the beginning of 2022. He plans to start his first monthly contribution to his savings account on January 31, 2022 and intends to keep contributing the same amount on the last day of every month for 30 years.

Figuring in the early years he can be more aggressive and will have the time to ride out natural cycles in the markets, he intended to invest in funds with a heavier weight in stocks than bonds for the first 25 years (the first 300 months from January 1, 2022 through and including December 31, 2046). His assumption is that he will earn an annual rate of return of 12%, compounded monthly.

For the five years before his retirement (from January 1, 2047 through and including December 31, 2051), Krishna realizes he will want to be more conservative with his investments because he will be in less of a position to weather any serious drops in the markets. He intends to rebalance his portfolio to favor bonds and less risky stocks that will earn an annual rate of return of 8%, compounded monthly.

In retirement (from January 1, 2052 through and including December 31, 2076), Krishna plans to shift his investments to certificates of deposits and the most conservative investment choices which he expects will yield an annual rate of return of 6%, compounded monthly.

He is also assuming that his employers will match his contribution during the 30-year savings period at the rate of 50%. In other words, for every $1 that Krishna contributes to his account, his employers will contribute $0.50, so that $1.50 is deposited into his account.

He also assumes that, in the last 5 years before his retirement, he will be making a higher salary and will be in a better position to contribute more to the account. He plans to double the amount of the contributions to his account compared to the first 25 years.

At the conclusion of his retirement, Krishna would like to donate $1.15 to NYU to fund overworked and underpaid adjunct faculty.

(Table with picture)

How much should Krishna begin contributing monthly on January 31, 2022?

-

$150.00

-

$200.00

-

$212.06

-

$249.86

-

$270.97

-

$314.79

-

$415.47

-

$1,098.49

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Beat The Market Win With Proven Stock Selection And Market Timing Tools

Authors: Gerald Appel

1st Edition

0132359170,0137154526