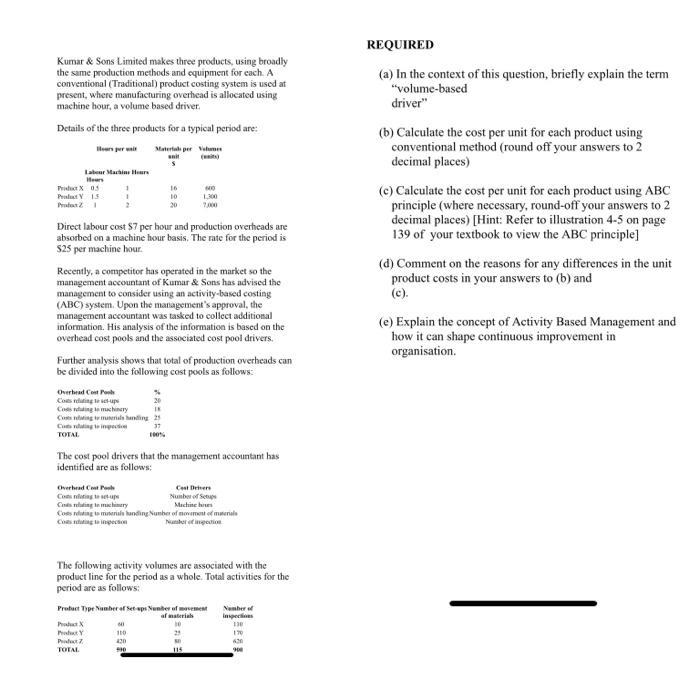

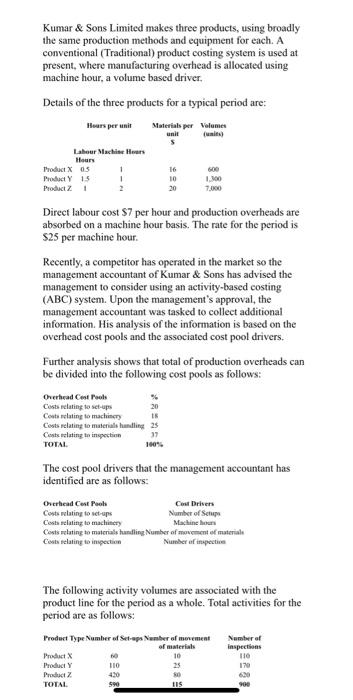

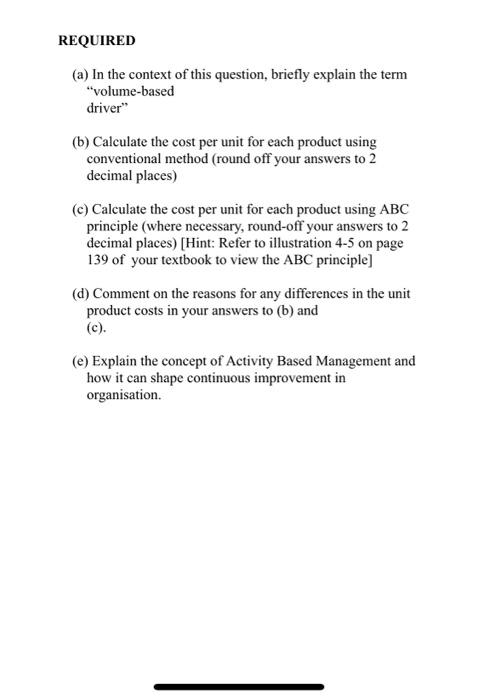

Kumar & Sons Limited makes three products, using broadly the same production methods and equipment for each. A conventional (Traditional) product costing system is used at present, where manufacturing overhead is allocated using machine hour, a volume based driver Details of the three products for a typical period are: Hell Material per me REQUIRED (a) In the context of this question, briefly explain the term "volume-based driver" (b) Calculate the cost per unit for each product using conventional method (round off your answers to 2 decimal places) (c) Calculate the cost per unit for each product using ABC principle (where necessary, round-off your answers to 2 decimal places) [Hint: Refer to illustration 4-5 on page 139 of your textbook to view the ABC principle] (d) Comment on the reasons for any differences in the unit product costs in your answers to (b) and lalaar Martila tar- PulY IS Prato 1 10 20 1.300 (e) Explain the concept of Activity Based Management and how it can shape continuous improvement in organisation. Direct labour cost $7per hour and production overheads are absorbed on a machine hour basis. The rate for the period is $25 per machine hour Recently, a competitor has operated in the market so the management accountant of Kumar & Sons has advised the management to consider using an activity-based costing (ABC) system. Upon the management's approval, the management accountant was tasked to collect additional information. His analysis of the information is based on the overhead cost pools and the associated cost pool drivers. Further analysis shows that total of production overheads can be divided into the following cast pools as follows: Overhead Cost Penh Coding Cosing schery Casting terms and 25 Catering 100% The cost pool drivers that the management accountant has identified are as follows: Overhead Cle Coster Consigtsup Number of Consoliday in mclamery Machines Cossing te mrekunding Number of womende inpam TOTAL The following activity volumes are associated with the product line for the period as a whole. Total activities for the period are as follows: Protort Type Nomber of Setaps Number of movement Number after Inspecs PY Pa TOTAL 115 Kumar & Sons Limited makes three products, using broadly the same production methods and equipment for each. A conventional (Traditional) product costing system is used at present, where manufacturing overhead is allocated using machine hour, a volume based driver. Details of the three products for a typical period are: Hars per unit Materials per volumes unit s Latour Machine Productos 1 Product Y15 1 Product Z1 2 16 10 1.100 Direct labour cost $7 per hour and production overheads are absorbed on a machine hour basis. The rate for the period is S25 per machine hour. Recently, a competitor has operated in the market so the management accountant of Kumar & Sons has advised the management to consider using an activity-based costing (ABC) system. Upon the management's approval, the management accountant was tasked to collect additional information. His analysis of the information is based on the overhead cost pools and the associated cost pool drivers. Further analysis shows that total of production overheads can be divided into the following cost pools as follows: Overhead Coat Pools Costs relating to set-ups 20 Costs relating to machine Costs relating to materials handling 25 Costs relating to inspection 37 TOTAL The cost pool drivers that the management accountant has identified are as follows: Overhead Cost Pooh Ces Drivers Costs relating to set-ups Number of Scrup Costelating to machinery Machines Costis melating to materials funding Number of movement of material Cosselating to inspection Number of inspectie The following activity volumes are associated with the product line for the period as a whole. Total activities for the period are as follows: Product Type Number of Setapa Namber of meement of materials 10 25 Number of inspections 110 170 110 Product Product Product TOTAL 590 TIS 900 REQUIRED (a) In the context of this question, briefly explain the term "volume-based driver" (b) Calculate the cost per unit for each product using conventional method (round off your answers to 2 decimal places) (c) Calculate the cost per unit for each product using ABC principle (where necessary, round-off your answers to 2 decimal places) [Hint: Refer to illustration 4-5 on page 139 of your textbook to view the ABC principle] (d) Comment on the reasons for any differences in the unit product costs in your answers to (b) and (c). (e) Explain the concept of Activity Based Management and how it can shape continuous improvement in organisation