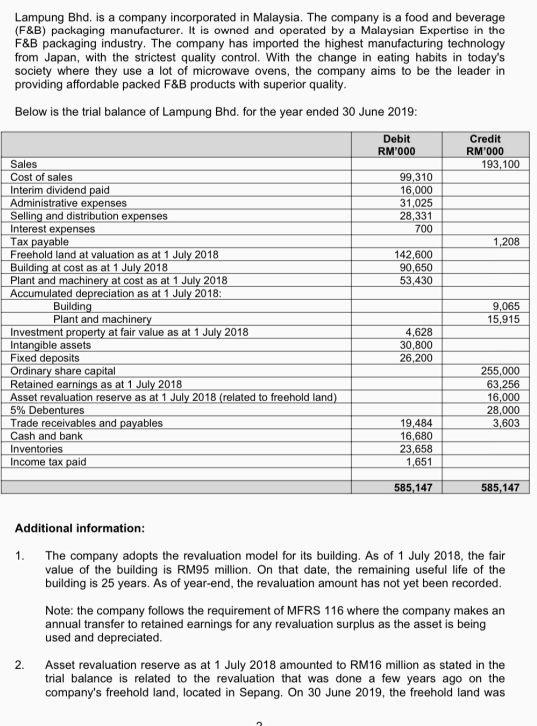

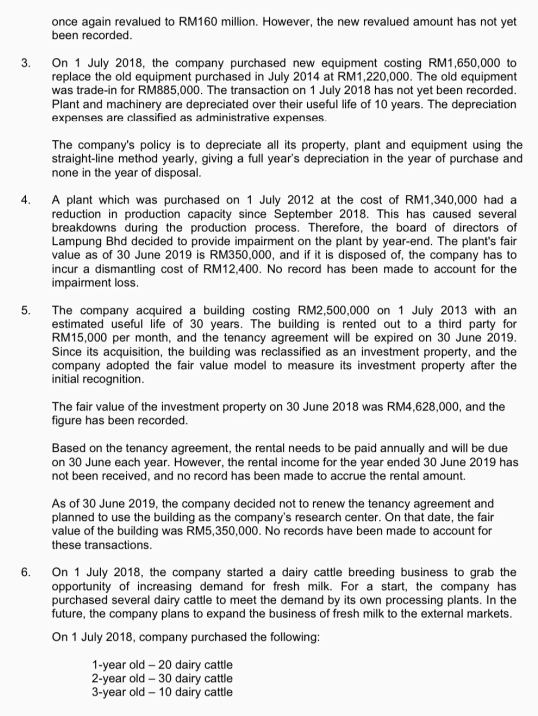

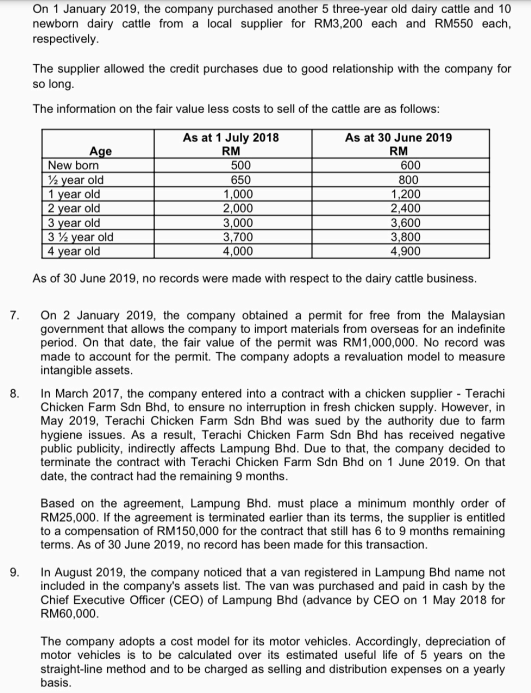

Lampung Bhd. is a company incorporated in Malaysia. The company is a food and beverage (F&B) packaging manufacturer. It is owned and operated by a Malaysian Expertise in the F&B packaging industry. The company has imported the highest manufacturing technology from Japan, with the strictest quality control. With the change in eating habits in today's society where they use a lot of microwave ovens, the company aims to be the leader in providing affordable packed F&B products with superior quality. Below is the trial balance of Lampung Bhd. for the year ended 30 June 2019: Debit Credit RM'000 RM'000 Sales 193,100 Cost of sales 99,310 16,000 Interim dividend paid Administrative expenses 31,025 Selling and distribution expenses Interest expenses 28,331 700 Tax payable 1,208 142,600 Freehold land at valuation as at 1 July 2018 Building at cost as at 1 July 2018 90,650 53,430 Plant and machinery at cost as at 1 July 2018 Accumulated depreciation as at 1 July 2018: Building 9,065 Plant and machinery 15,915 4,628 Investment property at fair value as at 1 July 2018 Intangible assets 30,800 Fixed deposits 26,200 Ordinary share capital 255,000 Retained earnings as at 1 July 2018 63,256 Asset revaluation reserve as at 1 July 2018 (related to freehold land) 16,000 5% Debentures 28,000 3,603 Trade receivables and payables 19,484 16,680 Cash and bank Inventories Income tax paid 23,658 1,651 585,147 585,147 Additional information: 1. The company adopts the revaluation model for its building. As of 1 July 2018, the fair value of the building is RM95 million. On that date, the remaining useful life of the building is 25 years. As of year-end, the revaluation amount has not yet been recorded. Note: the company follows the requirement of MFRS 116 where the company makes an annual transfer to retained earnings for any revaluation surplus as the asset is being used and depreciated. 2. Asset revaluation reserve as at 1 July 2018 amounted to RM16 million as stated in the trial balance is related to the revaluation that was done a few years ago on the company's freehold land, located in Sepang. On 30 June 2019, the freehold land was once again revalued to RM160 million. However, the new revalued amount has not yet been recorded. 3. On 1 July 2018, the company purchased new equipment costing RM1,650,000 to replace the old equipment purchased in July 2014 at RM1,220,000. The old equipment was trade-in for RM885,000. The transaction on 1 July 2018 has not yet been recorded. Plant and machinery are depreciated over their useful life of 10 years. The depreciation expenses are classified as administrative expenses. The company's policy is to depreciate all its property, plant and equipment using the straight-line method yearly, giving a full year's depreciation in the year of purchase and none in the year of disposal. 4. A plant which was purchased on 1 July 2012 at the cost of RM1,340,000 had a reduction in production capacity since September 2018. This has caused several breakdowns during the production process. Therefore, the board of directors of Lampung Bhd decided to provide impairment on the plant by year-end. The plant's fair value as of 30 June 2019 is RM350,000, and if it is disposed of, the company has to incur a dismantling cost of RM12,400. No record has been made to account for the impairment loss. 5. The company acquired a building costing RM2,500,000 on 1 July 2013 with an estimated useful life of 30 years. The building is rented out to a third party for RM15,000 per month, and the tenancy agreement will be expired on 30 June 2019. Since its acquisition, the building was reclassified as an investment property, and the company adopted the fair value model to measure its investment property after the initial recognition. The fair value of the investment property on 30 June 2018 was RM4,628,000, and the figure has been recorded. Based on the tenancy agreement, the rental needs to be paid annually and will be due on 30 June each year. However, the rental income for the year ended 30 June 2019 has not been received, and no record has been made to accrue the rental amount. As of 30 June 2019, the company decided not to renew the tenancy agreement and planned to use the building as the company's research center. On that date, the fair value of the building was RM5,350,000. No records have been made to account for these transactions. 6. On 1 July 2018, the company started a dairy cattle breeding business to grab the opportunity of increasing demand for fresh milk. For a start, the company has purchased several dairy cattle to meet the demand by its own processing plants. In the future, the company plans to expand the business of fresh milk to the external markets. On 1 July 2018, company purchased the following: 1-year old -20 dairy cattle 2-year old -30 dairy cattle 3-year old - 10 dairy cattle On 1 January 2019, the company purchased another 5 three-year old dairy cattle and 10 newborn dairy cattle from a local supplier for RM3,200 each and RM550 each, respectively. The supplier allowed the credit purchases due to good relationship with the company for so long. The information on the fair value less costs to sell of the cattle are as follows: As at 1 July 2018 As at 30 June 2019 Age RM RM 500 600 New born year old 1 year old 650 800 1,000 1,200 2 year old 2,000 2,400 3 year old 3,000 3,600 3,800 3 year old 4 year old 3,700 4,000 4,900 As of 30 June 2019, no records were made with respect to the dairy cattle business. 7. On 2 January 2019, the company obtained a permit for free from the Malaysian government that allows the company to import materials from overseas for an indefinite period. On that date, the fair value of the permit was RM1,000,000. No record was made to account for the permit. The company adopts a revaluation model to measure intangible assets. 8. In March 2017, the company entered into a contract with a chicken supplier - Terachi Chicken Farm Sdn Bhd, to ensure no interruption in fresh chicken supply. However, in May 2019, Terachi Chicken Farm Sdn Bhd was sued by the authority due to farm hygiene issues. As a result, Terachi Chicken Farm Sdn Bhd has received negative public publicity, indirectly affects Lampung Bhd. Due to that, the company decided to terminate the contract with Terachi Chicken Farm Sdn Bhd on 1 June 2019. On that date, the contract had the remaining 9 months. Based on the agreement, Lampung Bhd. must place a minimum monthly order of RM25,000. If the agreement is terminated earlier than its terms, the supplier is entitled to a compensation of RM150,000 for the contract that still has 6 to 9 months remaining terms. As of 30 June 2019, no record has been made for this transaction. 9. In August 2019, the company noticed that a van registered in Lampung Bhd name not included in the company's assets list. The van was purchased and paid in cash by the Chief Executive Officer (CEO) of Lampung Bhd (advance by CEO on 1 May 2018 for RM60,000. The company adopts a cost model for its motor vehicles. Accordingly, depreciation of motor vehicles is to be calculated over its estimated useful life of 5 years on the straight-line method and to be charged as selling and distribution expenses on a yearly basis. 10. On 29 June 2019, the company declared a final ordinary dividend of RM12 million for the financial year ended 30 June 2019. No payment and no records are made to account for the transaction. 11. 5% debenture refers to a debt instrument issued by the company on 1 July 2014. The debenture is not backed by any company's assets as collateral and has a maturity period of 15 years. The debenture carries a coupon rate of 5% per annum and pays the coupon semiannually. The principle amount is due upon maturity. 12. The current year's tax rate is 25%. After an authorized tax agent does the tax calculation, the company's income tax expense for the year ended 30 June 2019 was estimated at RM1,512,000. Calculation of the tax expense considers all related expenses and income, such as expenses that are not allowed to be tax-deductible, double deduction expenses, and capital allowance of the company's assets. 13. The financial statements for the year ended 30 June 2019 were signed and authorized by the board members for publication on 15 September 2019. Required: f. Refer to additional information (10), explain the appropriate accounting treatment if the company declares the ordinary final dividend on 15 July 2019. (50 Marks) Lampung Bhd. is a company incorporated in Malaysia. The company is a food and beverage (F&B) packaging manufacturer. It is owned and operated by a Malaysian Expertise in the F&B packaging industry. The company has imported the highest manufacturing technology from Japan, with the strictest quality control. With the change in eating habits in today's society where they use a lot of microwave ovens, the company aims to be the leader in providing affordable packed F&B products with superior quality. Below is the trial balance of Lampung Bhd. for the year ended 30 June 2019: Debit Credit RM'000 RM'000 Sales 193,100 Cost of sales 99,310 16,000 Interim dividend paid Administrative expenses 31,025 Selling and distribution expenses Interest expenses 28,331 700 Tax payable 1,208 142,600 Freehold land at valuation as at 1 July 2018 Building at cost as at 1 July 2018 90,650 53,430 Plant and machinery at cost as at 1 July 2018 Accumulated depreciation as at 1 July 2018: Building 9,065 Plant and machinery 15,915 4,628 Investment property at fair value as at 1 July 2018 Intangible assets 30,800 Fixed deposits 26,200 Ordinary share capital 255,000 Retained earnings as at 1 July 2018 63,256 Asset revaluation reserve as at 1 July 2018 (related to freehold land) 16,000 5% Debentures 28,000 3,603 Trade receivables and payables 19,484 16,680 Cash and bank Inventories Income tax paid 23,658 1,651 585,147 585,147 Additional information: 1. The company adopts the revaluation model for its building. As of 1 July 2018, the fair value of the building is RM95 million. On that date, the remaining useful life of the building is 25 years. As of year-end, the revaluation amount has not yet been recorded. Note: the company follows the requirement of MFRS 116 where the company makes an annual transfer to retained earnings for any revaluation surplus as the asset is being used and depreciated. 2. Asset revaluation reserve as at 1 July 2018 amounted to RM16 million as stated in the trial balance is related to the revaluation that was done a few years ago on the company's freehold land, located in Sepang. On 30 June 2019, the freehold land was once again revalued to RM160 million. However, the new revalued amount has not yet been recorded. 3. On 1 July 2018, the company purchased new equipment costing RM1,650,000 to replace the old equipment purchased in July 2014 at RM1,220,000. The old equipment was trade-in for RM885,000. The transaction on 1 July 2018 has not yet been recorded. Plant and machinery are depreciated over their useful life of 10 years. The depreciation expenses are classified as administrative expenses. The company's policy is to depreciate all its property, plant and equipment using the straight-line method yearly, giving a full year's depreciation in the year of purchase and none in the year of disposal. 4. A plant which was purchased on 1 July 2012 at the cost of RM1,340,000 had a reduction in production capacity since September 2018. This has caused several breakdowns during the production process. Therefore, the board of directors of Lampung Bhd decided to provide impairment on the plant by year-end. The plant's fair value as of 30 June 2019 is RM350,000, and if it is disposed of, the company has to incur a dismantling cost of RM12,400. No record has been made to account for the impairment loss. 5. The company acquired a building costing RM2,500,000 on 1 July 2013 with an estimated useful life of 30 years. The building is rented out to a third party for RM15,000 per month, and the tenancy agreement will be expired on 30 June 2019. Since its acquisition, the building was reclassified as an investment property, and the company adopted the fair value model to measure its investment property after the initial recognition. The fair value of the investment property on 30 June 2018 was RM4,628,000, and the figure has been recorded. Based on the tenancy agreement, the rental needs to be paid annually and will be due on 30 June each year. However, the rental income for the year ended 30 June 2019 has not been received, and no record has been made to accrue the rental amount. As of 30 June 2019, the company decided not to renew the tenancy agreement and planned to use the building as the company's research center. On that date, the fair value of the building was RM5,350,000. No records have been made to account for these transactions. 6. On 1 July 2018, the company started a dairy cattle breeding business to grab the opportunity of increasing demand for fresh milk. For a start, the company has purchased several dairy cattle to meet the demand by its own processing plants. In the future, the company plans to expand the business of fresh milk to the external markets. On 1 July 2018, company purchased the following: 1-year old -20 dairy cattle 2-year old -30 dairy cattle 3-year old - 10 dairy cattle On 1 January 2019, the company purchased another 5 three-year old dairy cattle and 10 newborn dairy cattle from a local supplier for RM3,200 each and RM550 each, respectively. The supplier allowed the credit purchases due to good relationship with the company for so long. The information on the fair value less costs to sell of the cattle are as follows: As at 1 July 2018 As at 30 June 2019 Age RM RM 500 600 New born year old 1 year old 650 800 1,000 1,200 2 year old 2,000 2,400 3 year old 3,000 3,600 3,800 3 year old 4 year old 3,700 4,000 4,900 As of 30 June 2019, no records were made with respect to the dairy cattle business. 7. On 2 January 2019, the company obtained a permit for free from the Malaysian government that allows the company to import materials from overseas for an indefinite period. On that date, the fair value of the permit was RM1,000,000. No record was made to account for the permit. The company adopts a revaluation model to measure intangible assets. 8. In March 2017, the company entered into a contract with a chicken supplier - Terachi Chicken Farm Sdn Bhd, to ensure no interruption in fresh chicken supply. However, in May 2019, Terachi Chicken Farm Sdn Bhd was sued by the authority due to farm hygiene issues. As a result, Terachi Chicken Farm Sdn Bhd has received negative public publicity, indirectly affects Lampung Bhd. Due to that, the company decided to terminate the contract with Terachi Chicken Farm Sdn Bhd on 1 June 2019. On that date, the contract had the remaining 9 months. Based on the agreement, Lampung Bhd. must place a minimum monthly order of RM25,000. If the agreement is terminated earlier than its terms, the supplier is entitled to a compensation of RM150,000 for the contract that still has 6 to 9 months remaining terms. As of 30 June 2019, no record has been made for this transaction. 9. In August 2019, the company noticed that a van registered in Lampung Bhd name not included in the company's assets list. The van was purchased and paid in cash by the Chief Executive Officer (CEO) of Lampung Bhd (advance by CEO on 1 May 2018 for RM60,000. The company adopts a cost model for its motor vehicles. Accordingly, depreciation of motor vehicles is to be calculated over its estimated useful life of 5 years on the straight-line method and to be charged as selling and distribution expenses on a yearly basis. 10. On 29 June 2019, the company declared a final ordinary dividend of RM12 million for the financial year ended 30 June 2019. No payment and no records are made to account for the transaction. 11. 5% debenture refers to a debt instrument issued by the company on 1 July 2014. The debenture is not backed by any company's assets as collateral and has a maturity period of 15 years. The debenture carries a coupon rate of 5% per annum and pays the coupon semiannually. The principle amount is due upon maturity. 12. The current year's tax rate is 25%. After an authorized tax agent does the tax calculation, the company's income tax expense for the year ended 30 June 2019 was estimated at RM1,512,000. Calculation of the tax expense considers all related expenses and income, such as expenses that are not allowed to be tax-deductible, double deduction expenses, and capital allowance of the company's assets. 13. The financial statements for the year ended 30 June 2019 were signed and authorized by the board members for publication on 15 September 2019. Required: f. Refer to additional information (10), explain the appropriate accounting treatment if the company declares the ordinary final dividend on 15 July 2019. (50 Marks)