Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Large Mart has previously attempted to develop a study pillow which would have allowed students to upload study material into their brain whilst sleeping. However,

Large Mart has previously attempted to develop a study pillow which would have allowed students to upload study material into their brain whilst sleeping. However, Large Mart has recently discovered that an American company called Bpple already holds a patent for this type of device. As a result, Large Mart has given up on its development attempts and decided to sell the Bpple product, which is called iSLEEP.

In order to sell the iSLEEP, Large Mart has rented a second store in Armidale. Large Mart signs a 12 month renting contract on 1st May 201x. The rent for the store will be $400 per month and the renting contract requires Large Mart to pay rent at the beginning of each quarter, starting on 1st May 201x (rent to be paid for the remainder of that quarter). This means that that the rent paid on 1st May 201x is for the months of May 201x and June 201x.

As soon as the renting contract for the new store is signed, Large Mart employs two UNE students (Chuck and Morgan). Chuck and Morgan are employed for 15 hours per person each month. Their job is to organise an iSLEEP fan site on Facebook. Chuck and Morgan start their jobs on 1st May 201x and will be paid $30 per hour. On 31st May 201x the HR department planned to pay Chuck and Morgan for the work they completed during the month. However, before the HR department can make the transfer, it notices that Chuck and Morgan have not provided Large Mart with their bank account details and, as a result, Large Mart is unable to pay Chuck and Morgan for their work. After the HR department sends Chuck and Morgan and email, they forward their bank account details to Large Mart on 10th June 201x and Large Mart is finally able to pay Chuck and Morgan for the work they have completed in May 201x. Large Mart makes the payment on 10th June 201x.

The furniture in the new store is designed and manufactured in China. An important part of the store design is a big bed on which customers can lie to test the iSLEEP before purchasing it. The bed is delivered on 1st June 201x. On that day, Large Mart also receives an invoice of $40,000 from the Chinese designer/manufacturer of the bed. When the bed was produced in China, the director of the Large Mart sales department travelled to the Chinese designer/manufacturer to approve solutions to production problems. Without this approval from the director of the Large Mart sales department, the production process could not have continued. The director of the sales department did not make any other stops during his trip to China and only met with the design/manufacturing team of the bed. The overall expenditure associated with the sales directors visit to China was $12,000. The cost of the trip will be paid to the travel agent on the last day of June 201x (you should assume that the expenditure of $12,000 for the directors trip to China was incurred on 1st June).

After the new store is completed, Large Mart orders 50 iSLEEPs from Bpple for a price of $800 per iSLEEP, and these iSLEEPs arrive on 1st June 201x, and are paid via bank transfer 10 days later after Large Mart deducts a 10% early payment discount. After this initial purchase, the following purchase and sales transactions take place within the new store:

On 5th June 201x, Large Mart purchases another 60 iSLEEPS from Bpple for $750 per iSLEEP. The iSLEEPs arrive on the same day and Large Mart pays this new delivery of iSLEEPS on the next day without deducting any early payment discounts.

On 7th June 201x UNE purchases 100 iSLEEPs for the library for a price of $2,500 per iSLEEP on credit. Two days later UNE returns 20 of the purchased iSLEEPs because there is not enough space in the library for all 100 iSLEEPs. Large Mart is able to return the 20 iSLEEPS to its sales stock as they are unopened. On the day the iSLEEPS are returned, Large Mart also sends an adjusted invoice to UNE. UNE then pays the remaining iSLEEPs on 10th June 201x, after deducting an early payment discount of 5% from the invoice.

On 12th June 201x, Large Mart purchases a further 50 iSLEEPs for a price of $700 per iSLEEP. The iSLEEPs arrive on the same day and Large Mart pays the invoice two days later after deducting a 10% early payment discount.

On 1st July 201x, Large Mart leases a company car for the service department of the new store (called the Nerd Herd). The duration of the lease is 7 years, and the car has an expected useful life of 8 years. The lease contract requires Large Mart to pay $10,000 (via bank transfer) on 30th June of each year during the lease period. The lease contract states that Large Mart can cancel the lease at any time during the lease period after paying a penalty that is equal to 70% of the outstanding lease payments. If Large Mart does not cancel the lease, Large Mart will take over the ownership of the car at the end of the lease period. The interest rate implicit in the lease is 19%. Large Mart decided to enter into the lease agreement instead of purchasing the car because the purchase price would have been $47,000 and Large Mart did not have sufficient cash resources to make such a purchase at that time.

IMPORTANT NOTE: Large Mart has decided to use the exemption rules outlined in AASB 16, paragraphs 5-8 for all leased items to which these exemptions apply.

Please answer the following questions about the scenario outlined above:

Question 1) Provide all journal entries that are necessary in the books of Large Mart to account for the renting contract for the new store and all associated payments for the month of May 201x (and explain your journal entries) (1.5 marks).

Question 2) Provide all journal entries that are necessary in the books of Large Mart to account for the work that Chuck and Morgan have done during the month of May 201x, as well as the payment of wages to Chuck and Morgan on 10 June 201x (and explain your journal entries) (2 marks).

Question 3) Decide whether or not the expenditures associated with the China trip of the sales director are part of the cost of the bed (and provide a detailed explanation for your decision) (0.5 marks) and provide all journal entries that are necessary in the books of Large Mart to account for the purchase and delivery of the bed, assuming that all costs associated with the bed will be paid at a later date (1.0 mark).

Question 4) Provide all journal entries that are necessary in the books of Large Mart to account for all inventory purchase and sales transactions (including the payment and receipt of funds) of the new store, assuming that Large Mart uses a perpetual inventory system on a first-in-first-out basis (5.0 marks).

Question 5) Calculate the total Cost of Goods Sold (COGS) for the financial year ended 30 June 201x (1.0 mark), the value of all iSLEEPS that remain in the inventory account at the end of the year (the 30 June 201x) (1.0 mark), and the total amount of revenue that Large Mark collected through the sale of iSLEEPs during the year ended 30 June 201x (0.5 marks) (and outline all necessary calculations).

Question 6) Determine whether the lessor will have to account for the outlined car lease as an operating lease or a finance lease, AND provide a detailed explanation for your decision (2.5 marks).

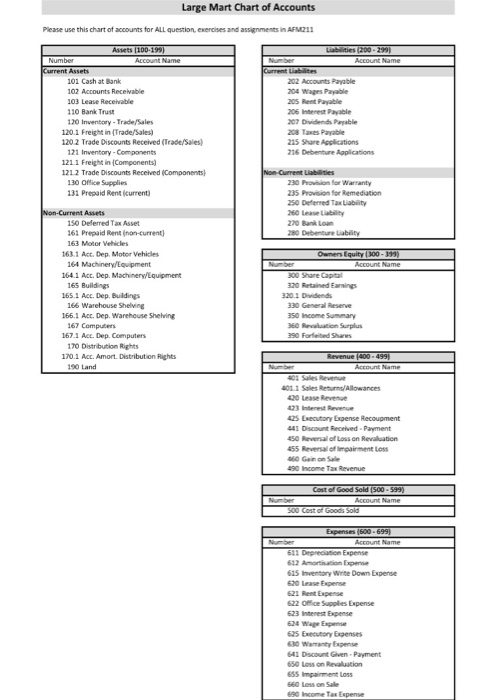

Remember to use the Large Mart Chart of Accounts to answer these questions.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Your Payment Cards Processes Systems And Applications A Step By Step PCIDSS Compliant Audit Program A Practice Guide For Payment Card Brands Issuers Acquirers Processors And Switches

Authors: Nwabueze Ohia

1st Edition

1521799229, 978-1521799222