Answered step by step

Verified Expert Solution

Question

1 Approved Answer

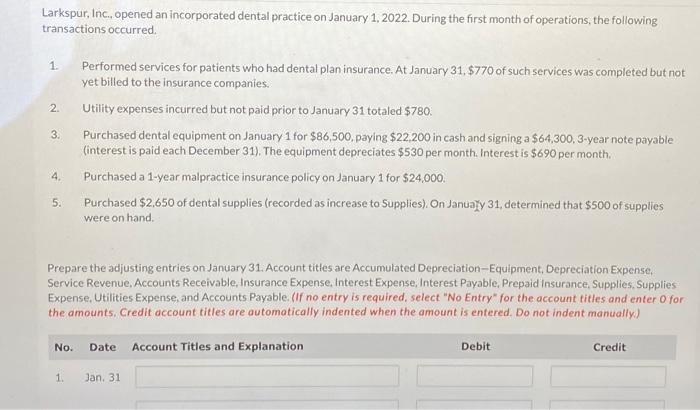

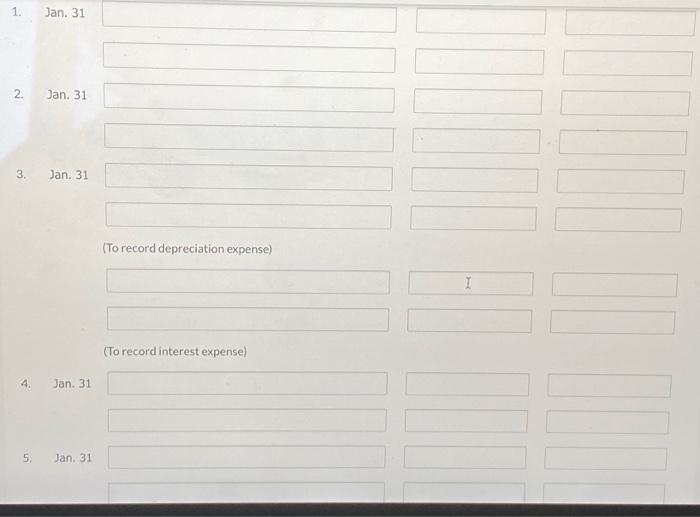

Larkspur, Inc., opened an incorporated dental practice on January 1,2022. During the first month of operations, the following transactions occurred. 1. Performed services for patients

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting A Practical Approach Chapters 1-25

Authors: Jeffrey Slater, Mike Deschamps

15th Edition

0137504284, 9780137504282