Answered step by step

Verified Expert Solution

Question

1 Approved Answer

last assignment before I graduate. I need a second option please! would appreciate any help I can get.. thank you! Culver Radio, Inc. As Clyde

last assignment before I graduate. I need a second option please! would appreciate any help I can get.. thank you!

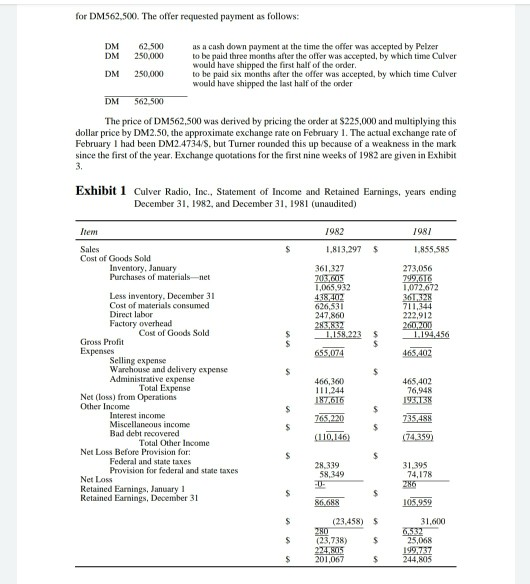

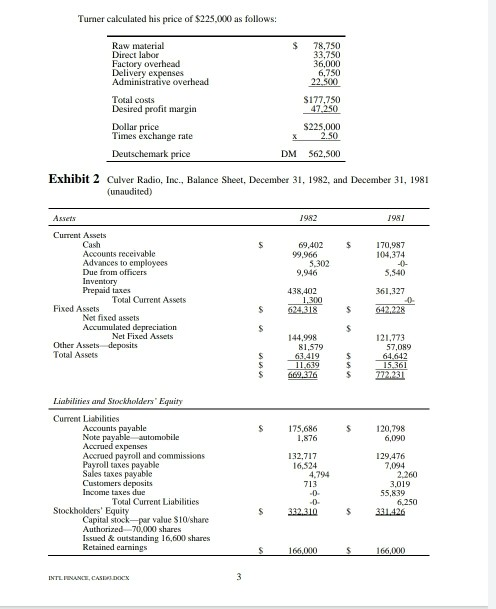

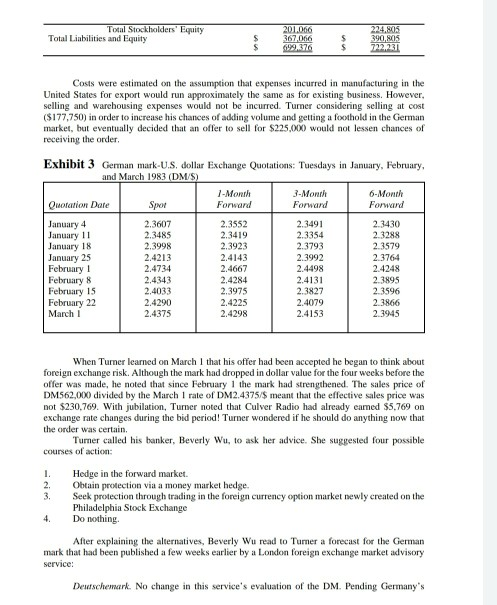

Culver Radio, Inc. As Clyde Turner, president and owner of Culver Radio, entered his Los Angeles office on March 1, 1983, he received a cable indicating acceptance of Culver's offer to supply Klaus Pelzer, a West German distributor, with approximately one quartier million dollars of radio equipment for the remote opening of gates and garages in industrial plants and parking lots. the cable also indicated that Pelzer had wired the requested deposit of DM62,500 directly to Culver's West Los Angeles bank that same day. Turner hoped the German order would mark the beginning of Culver's return to being profitable. Culver's 1982 net loss of S24,000 had been the combined result of a general recession in the United States and a lack of marketing effort to find new customers. Culver Radio was formed in the mid-1960s to manufacture radio-activated controls for opening residential garage doors, California's boom in residential construction and the increase in suburban single family residences with two-car garages created the potential. The level of affluence of new home buyers in the 1960s and 1970s led to a willingness to spend about $400 to be able to open a garage door without having to first get our of the car. Sales rose rapidly and profits were more than adequate. In 1979. however, new housing construction tapered off Culver's high quality meant that the replacement market was virtually zero, and sales began to slip. Turner realized as early as 1978 that the suburban residential market would not regain its former strength, so he tumed to development of an industrial version of his basic product. The industrial model was for use by delivery trucks and other vehicles entering or leaving warehouse compounds where security was important. An approaching or departing truck would notify plant security by radio of a desire to pass through the gate, but final control of the gate remained with plant security Security could either activate the gates to open automatically on radio request from the truck, a common procedure during daylight hours, or it could control the actual gate directly opening it after verification that the vehicle and driver were indeed authorized to enter or leave The industrial model proved particularly useful in inner city areas where crime was a problem. Sales of the industrial model in 1980 were good, but the recession of 1981 and 1982 caused a leveling out of sales volume while costs continued to rise with inflation. In 1981 Culver Radio experienced an operating loss, but interest income and profit from selling older equipment offset the loss. Net income for the year was positive. The 1982 operating loss was larger and was not offset by nonoperating income. Financial statements for Culver Radio for 1981 and 1982 appear in Exhibits 1 and 2 To use idle capacity. Turner decided in 1982 to stress exports. A few foreign firms had purchased Culver's gate openers for use in their home country and had been pleased with the result. Culver Radio itself, however, had never solicited a foreign order. After discussion with the U.S. Department of Commerce International Marketing Center in Los Angeles, Turner contacted Klaus Pelzer, an industrial radio distributor in Karlsruhe, Germany. Turner flew to Frankfurt to demonstrate the Culver industrial model to Pelzer, and by Christmas of 1982 Pelzer indicated an interest in becoming the German distributor if costs seemed reasonable. On February 1, 1983, Turner offered to sell Pelzer a shipment of radios and gate openers INTENANCE for DM562.500. The offer requested payment as follows: DM DM 62.500 250.000 as a cash down payment at the time the offer was accepted by Pelzer to be paid three months after the offer was accepted, by which time Culver would have shipped the first half of the order to be paid six months after the offer was accepted, by which time Culver would have shipped the last half of the order DM 250.000 DM562500 The price of DM562,500 was derived by pricing the order at $225,000 and multiplying this dollar price by DM2.50, the approximate exchange rate on February 1. The actual exchange rate of February I had been DM2.4734/S, but Tumer rounded this up because of a weakness in the mark since the first of the year. Exchange quotations for the first nine weeks of 1982 are given in Exhibit Exhibit 1 Culver Radio, Inc., Statement of Income and Retained Earnings, years ending December 31, 1982, and December 31, 1981 (unaudited) 1982 1987 1.813.297 S LASS SS Sales Cost of Goods Sold Inventory, January Purchases of materials net 361,327 713,605 1.045.932 438,402 626,531 247.860 2N3X37 158.223 273,056 799.616 1.072.672 3611328 222,912 260,200 1.194,456 5 655,0724 465.402 Less inventory. December 31 Cost of materials consumed Direct labor Factory overhead Cost of Goods Sold Gross Profit Expenses Selling expense Warehouse and delivery expense Administrative expense Total Expense Net (ons) from Operations Other Income Interest income Miscellaneous income Rad debt recovered Total Other Income Net Loss Before Provision for Federal and state taxes Provision for federal and state taxes Net Los Retained Earnings, January 1 Retained Earnings, December 31 466.00 111.244 187,676 465 402 76.948 19.13 765,220 (110.146) (74,359) 2119 31,395 74.178 286 10359 (23.458) 11.000 (23.738) 2015 201.067 1992737 204 205 Tumer calculated his price of $225,000 as follows: $ 78.750 32.750 Raw material Direct labor Factory overhead Delivery expenses Administrative overhead 360 6.750 22.500 Total costs Desired profit margin $177,750 47.250 Dollar price Times exchange rate S25.000 2.50 X DM Deutschemark price 562,500 Exhibit 2 Culver Radio, Inc., Balance Sheet, December 31, 1982, and December 31, 1981 (unaudited) 98 69.402 99.966 5302 9,946 170,987 104,374 5,540 Current Assets Cash Accounts receivable Advances to employees Due from officers Inventory Prepaid taxes Total Current Assets Fixed Assets Net fixed assets Accumulated depreciation Net Fixed Assets Other A ls deposits Total Assets 438,402 1.300 624.318 361,327 . 642.228 144,098 81.579 63.419 11.639 66976 121.273 57,089 64.642 15,361 777.231 Liabilities and ScheldenEquity 175.686 1.576 5 120,798 6.090 Current Liabilities Accounts payable Note payable automobile Accrued expenses Accrued payroll and commissions Payroll taxes payable Sales taxes payable Customer deposits Income taxes due Total Current Liabilities Stockholders' Equity Capital stock par value SIO Share Authorized 70.000 shares Issued & outstanding 16.600 shares Retained earnings 132,717 16524 4.794 713 -0- 129.476 70 2260 2019 55.839 6750 331,426 332 310 S $ 166,000 $ 166,000 INTLNCLCARBOX Total Stockholders' Equity Total Liabilities and Equity S 20.000 367,056 699 376 224.805 390.05 22 Costs were estimated on the assumption that expenses incurred in manufacturing in the United States for export would run approximately the same as for existing business. However, selling and warehousing expenses would not be incurred. Turner considering selling at cost ($177,750) in order to increase his chances of adding volume and getting a foothold in the German market, but eventually decided that an offer to sell for $225.000 would not lessen chances of receiving the order. Exhibit 3 German mark-U.S. dollar Exchange Quotations: Tuesdays in January, February and March 1983 (DMS) 7- Month 3- Month 6-Month Out Date SI Forward Forward Forward January 4 January 11 January 18 January 25 February 1 February 8 February 15 February 22 March 1 2.3607 23485 2.3998 2.4213 2.4734 2.4343 2.4033 2.4290 2.4375 2.3552 2.3419 2.3923 2.4143 2.4667 2.4284 2.3975 2.4225 2.4298 2.3491 23354 2.3793 2.3992 2.4498 2.4131 2.3827 2.4079 2.4153 2430 2.3288 2.3579 23764 24248 2.3895 23596 2166 2. 1945 When Turner learned on March 1 that his offer had been accepted he began to think about foreign exchange risk. Although the mark had dropped in dollar value for the four weeks before the offer was made, he noted that since February 1 the mark had strengthened. The sales price of DM562,000 divided by the March I rate of DM2.4375/$ meant that the effective sales price was not $230,769. With jubilation, Tumer noted that Culver Radio had already camed 55,769 on exchange rate changes during the bid period! Turner wondered if he should do anything now that the order was certain Tumer called his banker, Beverly Wu, to ask her advice. She suggested four possible courses of action: Hedge in the forward market Obtain protection via a money market hedge. Seek protection through trading in the foreign currency option market newly created on the Philadelphia Stock Exchange Do nothing 4. After explaining the alternatives, Beverly Wu read to Turner a forecast for the German mark that had been published a few weeks earlier by a London foreign exchange market advisory service: Deutschemark. No change in this service's evaluation of the DM. Pending Germany's March Selections the DM will attract a following as a dollar alternative, but the following is based on its historical attractions and weight, it is more of a Pavlovian reaction than the choice of careful analysis. The German election was between Helmut Kohl of the conservative Christian Democratic Party and Hans-Jochen Vogel, a former mayor of Munich and the leader of the Social Democrats. A major part of the election campaign centered on whether U.S. Pershing 11 and cruise missiles should be stationed on German soil. The Kohl forces generally favored continued close links with NATO and the US military, while Vogel demanded that the US and Soviets sign an arms agreement that would make it unnecessary for NATO to install the Pershing and cruise missiles. Since US. missiles were involved, Turner speculated that the turn of the election might influence the direction of the Deutschemark/dollar exchange rate. However, he knew he would have to make a decision before the election. The four alternatives described by the hanker were as follows: 1. Hedge in the Forward Market In the forward market one sells marks for dollars, or vice versa, today, at a fixed price, with delivery to be accomplished at some future date, such as within one, three, or six months. The advantage of the procedure that Turner would be assured of a fixed number of dollars when the mark sales proceeds were received. Turner noted that the three month forward price was DM2,4153/S and the six-month price was DM2.3945/5, meaning that more dollars would be received per mark in the future than al present. The banker explained that this was because interest rates and inflation in Germany at that moment were below comparable US rates. She reported that the German bank prime rate was 12.0% while the U.S. bank prime was 15.0%. Three-month and six-month government bill rates were 10.0% in Germany and 13.6% in the United States 2. Hedge in the Money Market Beverly Wu explained that her bank would be able to arrange for Culver Radio to borrow marks from a bank in Germany. The rate charged would be one percentage point above the German bank prime. Should Tumer want, he could borrow marks in Germany today, exchange those marks for dollars at once in the spot market, and in three or six months use the mark sales proceeds to repay the German loans. 3. Hedge with Foreign Currency Options In December 1982 the Philadelphia Stock Exchange began trading in foreign currency options. Options were available in five currencies and in multiples of standard sized contracts: DM SF Deutschemarks Swiss francs British pounds Canadian dollars Japanese yen 62,500 per contract 62.500 per contract 12.500 per contract 50,000 per contract 6,250,000 per contract CS A person wanting to buy an option on 50,000, for example, would purchase four contracts: ES0000/12.500 = 4 contracts Foreign currency options expire on the Saturday preceding the third Wednesday of the expiration month, and expiration months are March, June, September, and December Thus all contracts for June 1983 expire on June 11, 1983, and all September 1983 contracts INTENANCE.CADOCX expire on September 17, 1983. To obtain protection for September 1, Turner would have to buy contracts that expire on September 17, and then sell the contracts 17 days before they expire. This should not be a problem as a ready market existed. Each contract has an exercise or "strike price expressed in "U.S. terms, that is, the U.S. dollar price of the foreign currency. This is the reciprocal of European terms," which is the way interbank trading is conducted. All strike prices are stated in two cent intervals thus, mark options might have strike prices of 38, 40, 42, 44c. etc. One strike price is usually the rounded price nearest the spot rate at the time the contract is written An option contract also has a purchase price or "premium. According to the Wall Street Journal a "Deutschemark June 42" put could be purchased for 1.17 cents (e.g., S0.0117) per mark and a "September 42" put could be purchased for 1.48 cents (S0.0148) per mark, June 42" means a contract that expires the following June and has a strike price of $0.42 per mark. "Put" means the option to deliver marks and receive dollars, whereas "call" means the option to deliver dollars and receive marks. A June 42 call could be purchased for 1.60 cents, and a September 42 call could be purchased for 1.88 cents. If the spot price of a mark were less than 42 in June, the holder of a put option could deliver marks and be assured of receiving 42e for each mark. However, if the spot price of a mark were above 42e, a person could simply sell any available marks at the higher spot price and let the option expire. 4. Do Nothing To do nothing would mean simply waiting until the sales proceeds were received in June and September and at that time exchange marks received for dollars at the ten current spot price. The amount received might be more or less than anticipated, depending upon trends in the spot price Other Factors On notification from his bank of the receipt of the DM62,500 deposit, Tumer sold the marks for dollars at once, receiving $25.641 at the spot price of DM2.4375/$. Turner estimated that the long run weighted average after-tax cost of capital for Culver Radio was 24%. Culver Radio was too small to raise long-term debt funds, so it relied mainly on its equity for long-term financing INTLINANCE

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting Volume 2

Authors: Thomas Beechy, Joan Conrod, Elizabeth Farrell, Ingrid McLeod-Dick

7th Edition

1259108023, 9781259108020