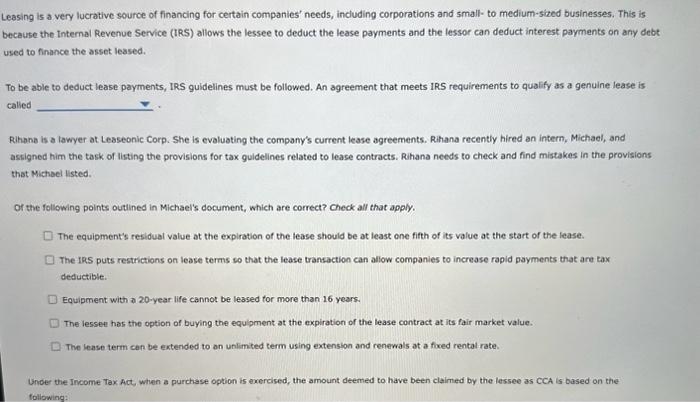

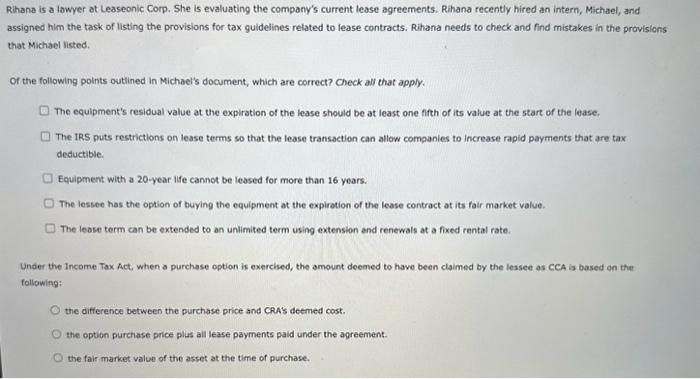

Leasing is a very lucrative source of financing for certain companies' needs, including corporations and small- to medium-sized businesses. This is because the Internal Revenue Service (IRS) allows the lessee to deduct the lease payments and the lessor can deduct interest payments on any debt used to finance the asset leased. To be able to deduct lease payments, IRS guidelines must be followed. An agreement that meets IRS requirements to qualify as a genuine lease is calied Rihana is a lawyer at Leaseonic Corp. She is evaluating the company's current lease agreements. Rihana recently hired an intern, Michael, and askigned him the task of listing the provisions for tax guldelines related to lease contracts. Rihana needs to check and find mistakes in the provisions that Michoel listed. of the following points outined in Michael's document, which are correct? Check all that apply. The equipment's residual value at the expiration of the lease should be at least one fifth of its value at the start of the lease. The IRS puts restrictions on lease terms so that the lease transaction can allow companies to increase rapid payments that are tax deductible. Equipment with a 20 -year life cannot be leased tor more than 16 years. The lessee has the option of buying the equipment at the expiration of the lease contract at its fair market value. The lease term cen be extended to on unlimited term using extension and renewals at a fixed rental rate. Under the Income Tax Act, when a purchase option is exercised, the amount deemed to have been claimed by the lessee as ccA is based on the Rihana is a lawyer at Leaseonic Corp. She is evaluating the company's current lease agreements. Rihana recently hired an intern, Michael, and assigned him the task of listing the provisions for tax guidelines related to lease contracts. Rihana needs to check and find mistakes in the provisions that Michael listed. Of the following points outlined in Michael's document, which are correct? Check all that apply. The equipment's residual value at the expiration of the lease should be at least one fifth of its value at the start of the lease. The IRS puts restrictions on lease terms so that the lease transaction can allow companies to increase rapid payments that are tax deductible. Equipment with a 20 -year life cannot be leased for more than 16 years. The lessee has the option of buying the equipment at the expiration of the lease contract at its fair market value. The lease term can be extended to an unlimited term using extension and renewals at a fixed rental rate. Under the Income Tax Act, when a purchase option is exercised, the amount deemed to have been claimed by the lessee as ceA is based on the following: the difference between the purchase price and CRAs deemed cost. the option purchase price plus all lease payments paid under the agreement. the fair market value of the asset at the time of purchase