Answered step by step

Verified Expert Solution

Question

1 Approved Answer

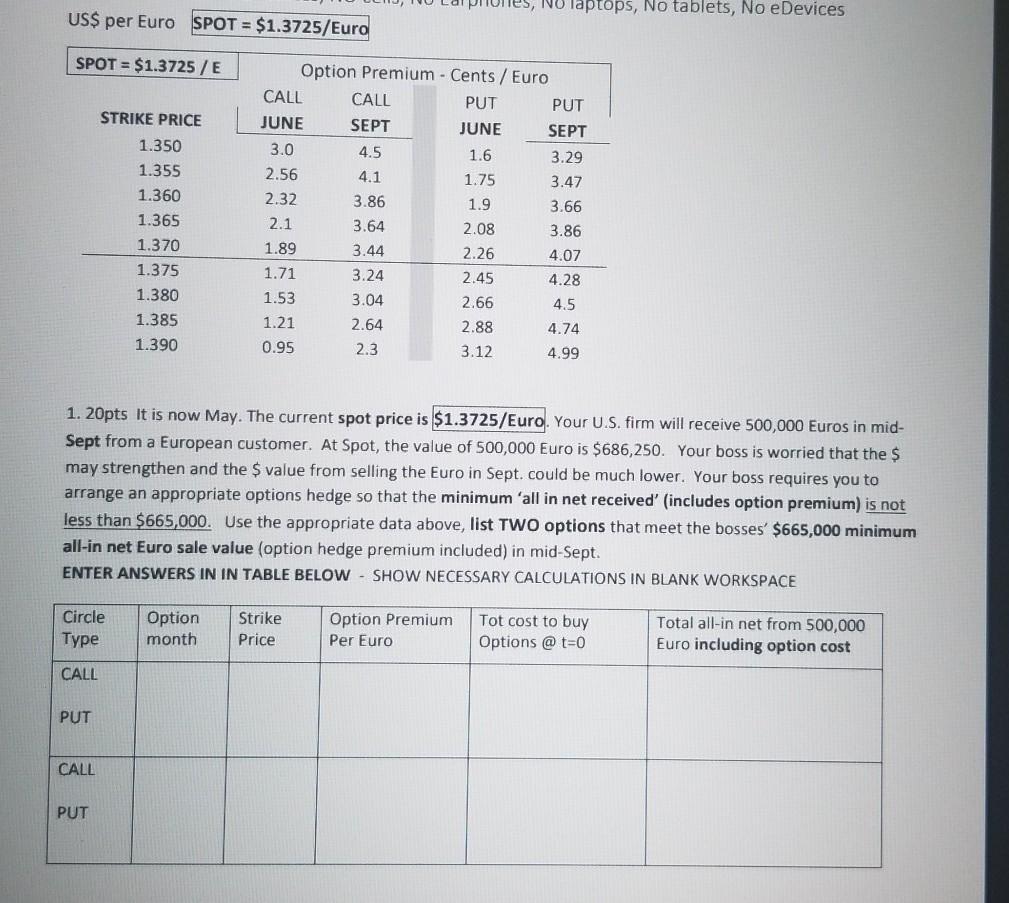

les, NO laptops, No tablets, No e Devices US$ per Euro SPOT = $1.3725/Euro SPOT = $1.3725 / E 3.86 STRIKE PRICE 1.350 1.355 1.360

les, NO laptops, No tablets, No e Devices US$ per Euro SPOT = $1.3725/Euro SPOT = $1.3725 / E 3.86 STRIKE PRICE 1.350 1.355 1.360 1.365 1.370 1.375 1.380 1.385 1.390 Option Premium - Cents / Euro CALL CALL PUT PUT JUNE SEPT JUNE SEPT 3.0 4.5 1.6 3.29 2.56 4.1 1.75 3.47 2.32 1.9 3.66 2.1 3.64 2.08 3.86 1.89 3.44 2.26 4.07 1.71 3.24 2.45 4.28 1.53 3.04 2.66 4.5 1.21 2.64 2.88 4.74 0.95 2.3 3.12 4.99 1. 20pts It is now May. The current spot price is $1.3725/Euro. Your U.S. firm will receive 500,000 Euros in mid- Sept from a European customer. At Spot, the value of 500,000 Euro is $686,250. Your boss is worried that the $ may strengthen and the $ value from selling the Euro in Sept. could be much lower. Your boss requires you to arrange an appropriate options hedge so that the minimum 'all in net received' (includes option premium) is not less than $665,000. Use the appropriate data above, list TWO options that meet the bosses' $665,000 minimum all-in net Euro sale value (option hedge premium included) in mid-Sept. ENTER ANSWERS IN IN TABLE BELOW - SHOW NECESSARY CALCULATIONS IN BLANK WORKSPACE Circle Type Option month Strike Price Option Premium Per Euro Tot cost to buy Options @t=0 Total all-in net from 500,000 Euro including option cost CALL PUT CALL PUT

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance In Theory And Practice

Authors: Holley Ulbrich

2nd Edition

041558597X, 978-0415585972