Question: Let (X1, Y1), . . . , (Xm Y), be a random sample from a bivariate normal distribution with parameters p1,p2,af,a,p. (Note: (X1,Y1), ..., (XmYn)

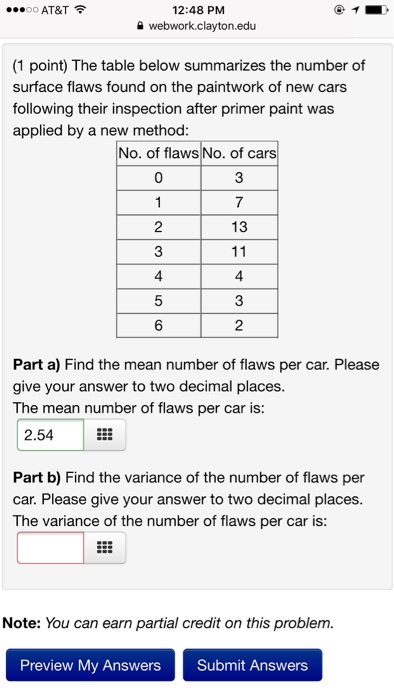

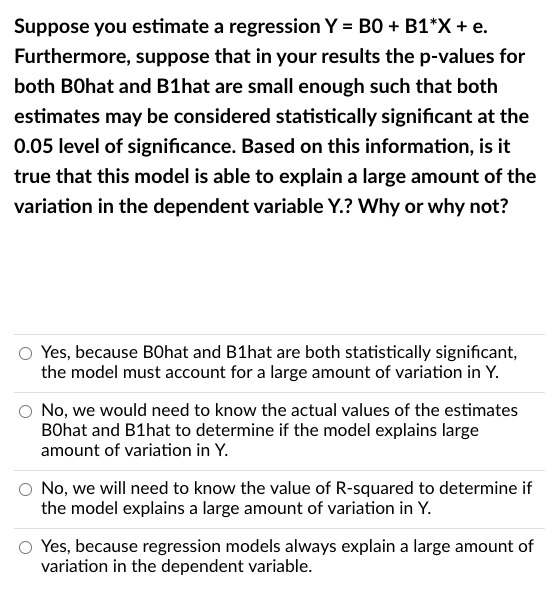

Let (X1, Y1), . . . , (Xm Y\"), be a random sample from a bivariate normal distribution with parameters p1,p2,af,a,p. (Note: (X1,Y1), ..., (XmYn) are independent). What is the joint distribution of (X, f\")? Hint: Find the joint moment generating function of (X, 17) and oompare it to the joint moment generating function of multivariate normal distribution. OOOOO AT&T S 12:48 PM A webwork.clayton.edu (1 point) The table below summarizes the number of surface flaws found on the paintwork of new cars following their inspection after primer paint was applied by a new method: No. of flaws No. of cars 0 3 7 2 13 11 4 4 5 3 6 2 Part a) Find the mean number of flaws per car. Please give your answer to two decimal places. The mean number of flaws per car is: 2.54 Part b) Find the variance of the number of flaws per car. Please give your answer to two decimal places. The variance of the number of flaws per car is: Note: You can earn partial credit on this problem. Preview My Answers Submit AnswersSuppose you estimate a regression Y = ED + 31*X + e. Furthermore, suppose that in your results the p-values for both BDhat and Blhat are small enough such that both estimates may be considered statistically signicant at the 0.05 level of signicance. Based on this information, is it true that this model is able to explain a large amount of the variation in the dependent variable Y.? Why or why net? Ci Yes. because Bhat and Eilhat are both statistically signicant, the model must account for a large amount of variation in Y. (I) No, we would need to know the actual values of the estimates Bhat and Bihat to determine if the model explains large amount of variation in 'r'. C) No, we will need to know the value of R-squared to determine if the model explains a large amount of variation in Y. C: Yes. because regression models always explain a large amount of variation in the dependent variable

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts