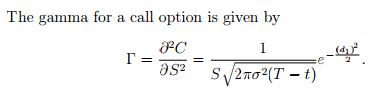

Question

Let?s say that stock in Amalgamated Boll Weevils (ABW) has an expected annual return of 9%, an annual volatility of 30%, and a current price

Let?s say that stock in Amalgamated Boll Weevils (ABW) has an expected annual return of 9%, an annual volatility of 30%, and a current price of 60 dollars per share. The risk free interest rate is 4%. Let?s say you own a call on ABW with a strike of 79 dollars per share and an expiration 3/4 of a year from now.

If you own the call option on ABW described above, how much ABW stock would you need to buy or sell to keep the total delta of your portfolio equal to zero? (This means that you will have completely ?delta hedged? your portfolio, which is also called making your portfolio ?delta neutral?.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of European Fixed Income Securities

Authors: Frank J. Fabozzi, Moorad Choudhry

1st Edition

0471430390, 978-0471430391