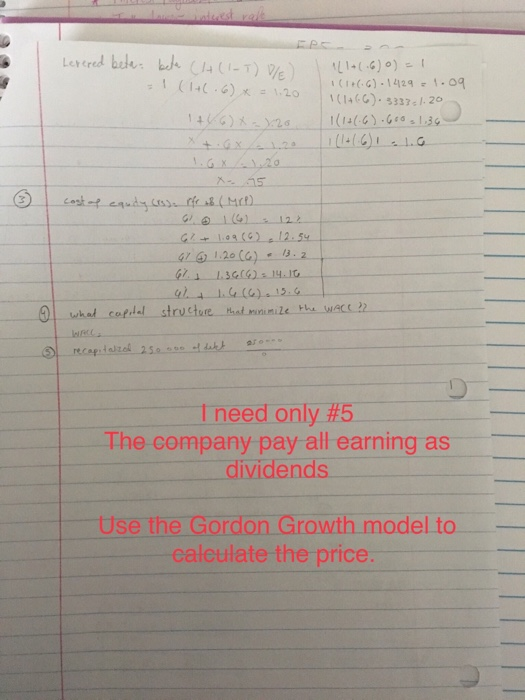

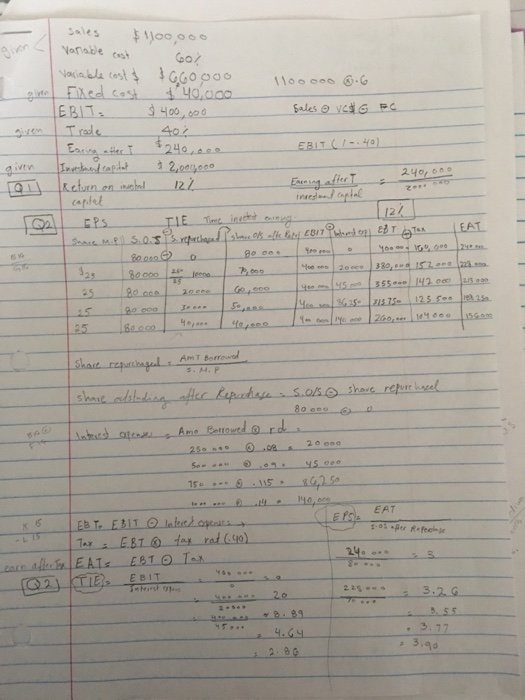

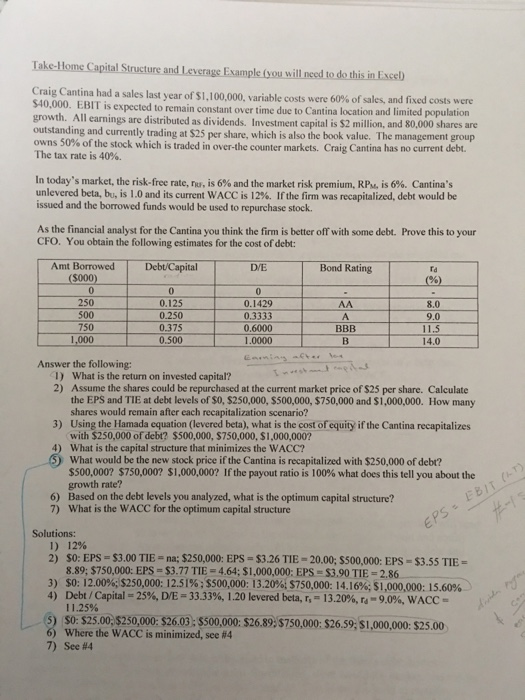

Levered beta: bele (+(1-T) D/E -! (1+(6) * = 120 (1+(6) 0) = 1 (+6). 1429 = 1.09 (160). 3337.1.20 1(1+(-6).600 31.36 ( (Met ) G?+ 1.09(6) 12.54 G7 6 1.20 (6) 13.2 6% 1.36(6): 14.16 4% 1.6 (6) 15.6 structure that minimize the WACC ? o what capital 3 recapitatzel 250.00 of dett a I need only #5 The company pay all earning as dividends Use the Gordon Growth model to caleulate the price. Sales $100,000 Varese cast Go Variable cost $ $660000 go fixed cost $40.000 1100 cos 6.6 EBIT. $ 400,000 sales @ VGAG PC given Trade 40% Erning after I $240,000 EBIT (-40) Inostrand capitat $2,002000 Return on instal 12% Emning after I 24 caplet EPS TIE Time inertest mining [122 Shane Mel .0.5. srprethana shu 05_sdk boty EBUT Pintere) og EBT @TeX B00600 8 00_ Yoon 80000 16 2 ,000 4 20 380, od 152 80. 2 6 . 0 5 . 1355 142.000 BO COD Jos 350 315 75 125 180000 40,000 | 40,000 10 con/ 140 000 1260,00 104000 EAT 2. 43 25 isom Shase reputihapel. Am F Bopreme share adstuding after Reportase 5.0/5 Interest ofense Amo Borrowed @rd. shave report has EBT. ERIT Infecette Tax EBT tax rat 6.40) aceh EATS ESTOIX @2) TIE, EDIT 24. - 3 3.2. Take Home Capital Structure and leverage Example you will need to do this in Excel Craig Cantina had a sales last year of $1,100,000, variable costs were 60% of sales, and fixed costs were $40,000. EBIT is expected to remain constant over time due to Cantina location and limited population growth. All earnings are distributed as dividends. Investment capital is $2 million, and 80,000 shares are outstanding and currently trading at $25 per share, which is also the book value. The management group owns 50% of the stock which is traded in over the counter markets. Craig Cantina has no current debt. The tax rate is 40%. In today's market, the risk-free rate, u, is 6% and the market risk premium, RP, is 6%. Cantina's unlevered beta, b is 1.0 and its current WACC is 12%. If the firm was recapitalized, debt would be issued and the borrowed funds would be used to repurchase stock As the financial analyst for the Cantina you think the firm is better off with some debt. Prove this to your CFO. You obtain the following estimates for the cost of debt: Amt Borrowed (5000) Debt/Capital D/E / Bond Rating 0 250 500 750 1,000 0.125 0.250 0.375 0.500 0 0.1429 0.3333 0.6000 1.0000 AA A BBB Answer the following: 1) What is the return on invested capital? 2) Assume the shares could be repurchased at the current market price of $25 per share. Calculate the EPS and TIE at debt levels of $0, $250,000, $500,000, $750,000 and $1,000,000. How many shares would remain after each recapitalization scenario? 3) Using the Hamada equation (levered beta), what is the cost of equity if the Cantina recapitalizes with $250,000 of debt? $500,000, $750,000 $1,000,000? 4) What is the capital structure that minimizes the WACC? 5 What would be the new stock price if the Cantina is recapitalized with $250,000 of debt? $500,000? $750,0007 $1,000,0007 If the payout ratio is 100% what does this tell you about the growth rate? 6) Based on the debt levels you analyzed, what is the optimum capital structure? 7) What is the WACC for the optimum capital structure EBIT (LT) EPS Solutions: 1) 12% 2) $0: EPS - $3.00 TIE-na; $250,000: EPS-$3.26 TIE-20.00, S500,000: EPS = $3.55 TIE- 8.89; $750,000: EPS - $3.77 TIE - 4.64; $1,000,000: EPS = $3.90 TIE-2.86 3) SO: 12.00%, $250,000: 12.51%, $500,000: 13.20% $750,000: 14.16% 51,000,000: 15,60% 4) Debt / Capital -25%, D/E - 33.33%, 1.20 levered beta, T, - 13.20%, -9.0%, WACC 11.25% 5) SO: $25.00, $250,000: $26.03: $500,000: $26.89; $750,000: $26.59; S1,000,000: $25.00 6) Where the WACC is minimized, see #4 7) See #4 Levered beta: bele (+(1-T) D/E -! (1+(6) * = 120 (1+(6) 0) = 1 (+6). 1429 = 1.09 (160). 3337.1.20 1(1+(-6).600 31.36 ( (Met ) G?+ 1.09(6) 12.54 G7 6 1.20 (6) 13.2 6% 1.36(6): 14.16 4% 1.6 (6) 15.6 structure that minimize the WACC ? o what capital 3 recapitatzel 250.00 of dett a I need only #5 The company pay all earning as dividends Use the Gordon Growth model to caleulate the price. Sales $100,000 Varese cast Go Variable cost $ $660000 go fixed cost $40.000 1100 cos 6.6 EBIT. $ 400,000 sales @ VGAG PC given Trade 40% Erning after I $240,000 EBIT (-40) Inostrand capitat $2,002000 Return on instal 12% Emning after I 24 caplet EPS TIE Time inertest mining [122 Shane Mel .0.5. srprethana shu 05_sdk boty EBUT Pintere) og EBT @TeX B00600 8 00_ Yoon 80000 16 2 ,000 4 20 380, od 152 80. 2 6 . 0 5 . 1355 142.000 BO COD Jos 350 315 75 125 180000 40,000 | 40,000 10 con/ 140 000 1260,00 104000 EAT 2. 43 25 isom Shase reputihapel. Am F Bopreme share adstuding after Reportase 5.0/5 Interest ofense Amo Borrowed @rd. shave report has EBT. ERIT Infecette Tax EBT tax rat 6.40) aceh EATS ESTOIX @2) TIE, EDIT 24. - 3 3.2. Take Home Capital Structure and leverage Example you will need to do this in Excel Craig Cantina had a sales last year of $1,100,000, variable costs were 60% of sales, and fixed costs were $40,000. EBIT is expected to remain constant over time due to Cantina location and limited population growth. All earnings are distributed as dividends. Investment capital is $2 million, and 80,000 shares are outstanding and currently trading at $25 per share, which is also the book value. The management group owns 50% of the stock which is traded in over the counter markets. Craig Cantina has no current debt. The tax rate is 40%. In today's market, the risk-free rate, u, is 6% and the market risk premium, RP, is 6%. Cantina's unlevered beta, b is 1.0 and its current WACC is 12%. If the firm was recapitalized, debt would be issued and the borrowed funds would be used to repurchase stock As the financial analyst for the Cantina you think the firm is better off with some debt. Prove this to your CFO. You obtain the following estimates for the cost of debt: Amt Borrowed (5000) Debt/Capital D/E / Bond Rating 0 250 500 750 1,000 0.125 0.250 0.375 0.500 0 0.1429 0.3333 0.6000 1.0000 AA A BBB Answer the following: 1) What is the return on invested capital? 2) Assume the shares could be repurchased at the current market price of $25 per share. Calculate the EPS and TIE at debt levels of $0, $250,000, $500,000, $750,000 and $1,000,000. How many shares would remain after each recapitalization scenario? 3) Using the Hamada equation (levered beta), what is the cost of equity if the Cantina recapitalizes with $250,000 of debt? $500,000, $750,000 $1,000,000? 4) What is the capital structure that minimizes the WACC? 5 What would be the new stock price if the Cantina is recapitalized with $250,000 of debt? $500,000? $750,0007 $1,000,0007 If the payout ratio is 100% what does this tell you about the growth rate? 6) Based on the debt levels you analyzed, what is the optimum capital structure? 7) What is the WACC for the optimum capital structure EBIT (LT) EPS Solutions: 1) 12% 2) $0: EPS - $3.00 TIE-na; $250,000: EPS-$3.26 TIE-20.00, S500,000: EPS = $3.55 TIE- 8.89; $750,000: EPS - $3.77 TIE - 4.64; $1,000,000: EPS = $3.90 TIE-2.86 3) SO: 12.00%, $250,000: 12.51%, $500,000: 13.20% $750,000: 14.16% 51,000,000: 15,60% 4) Debt / Capital -25%, D/E - 33.33%, 1.20 levered beta, T, - 13.20%, -9.0%, WACC 11.25% 5) SO: $25.00, $250,000: $26.03: $500,000: $26.89; $750,000: $26.59; S1,000,000: $25.00 6) Where the WACC is minimized, see #4 7) See #4