Answered step by step

Verified Expert Solution

Question

1 Approved Answer

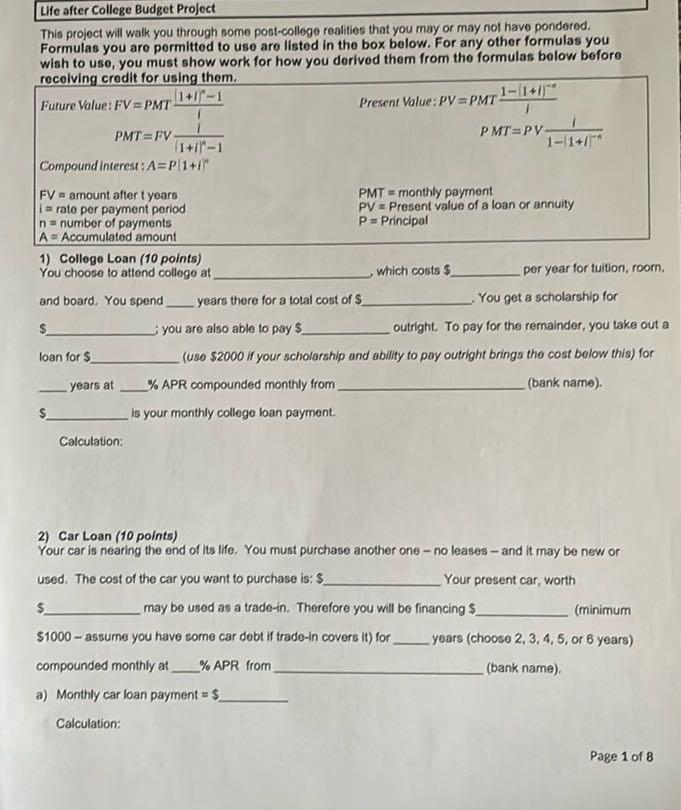

Life after College Budget Project This project will walk you through some post-college realities that you may or may not have pondered. Formulas you

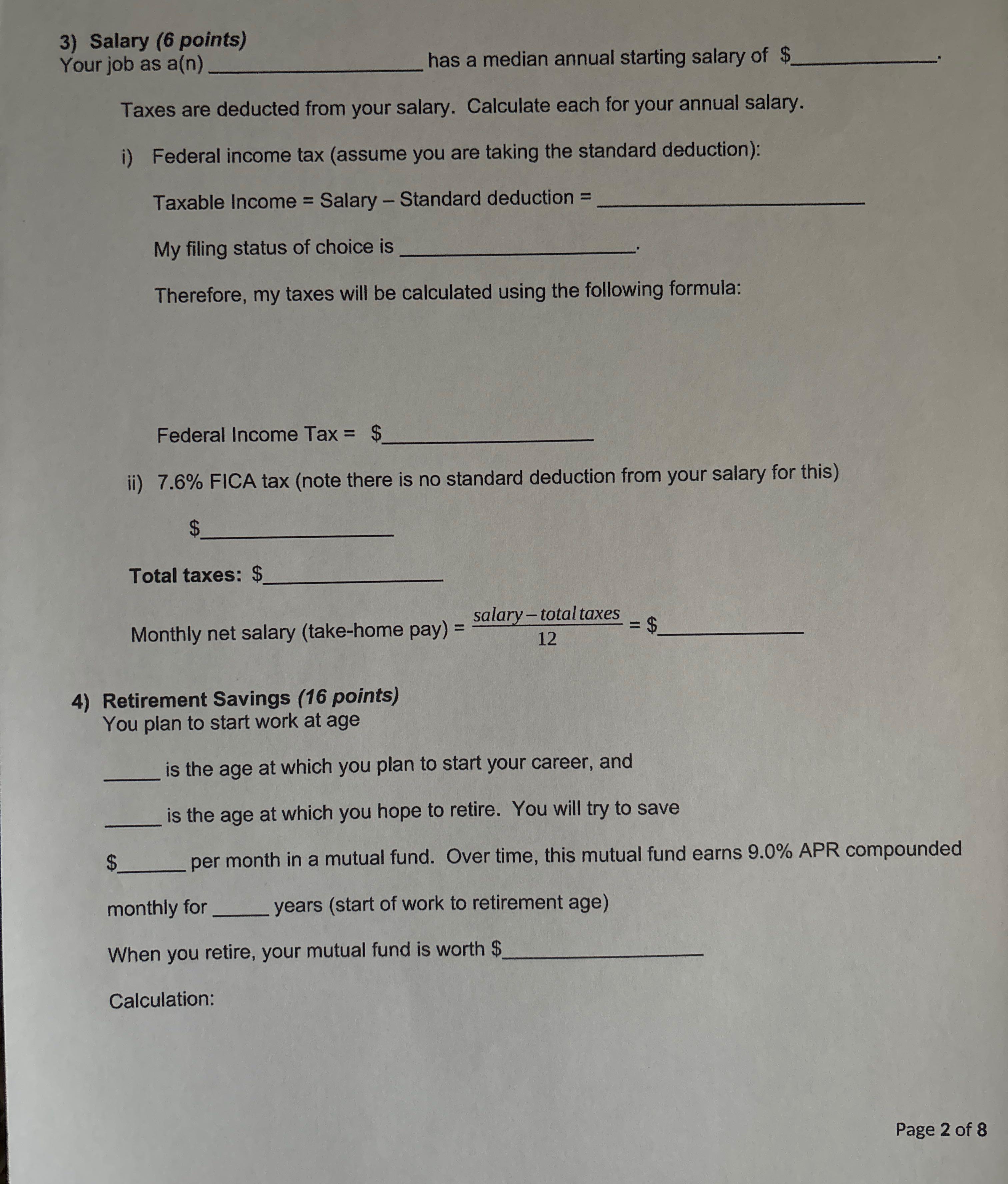

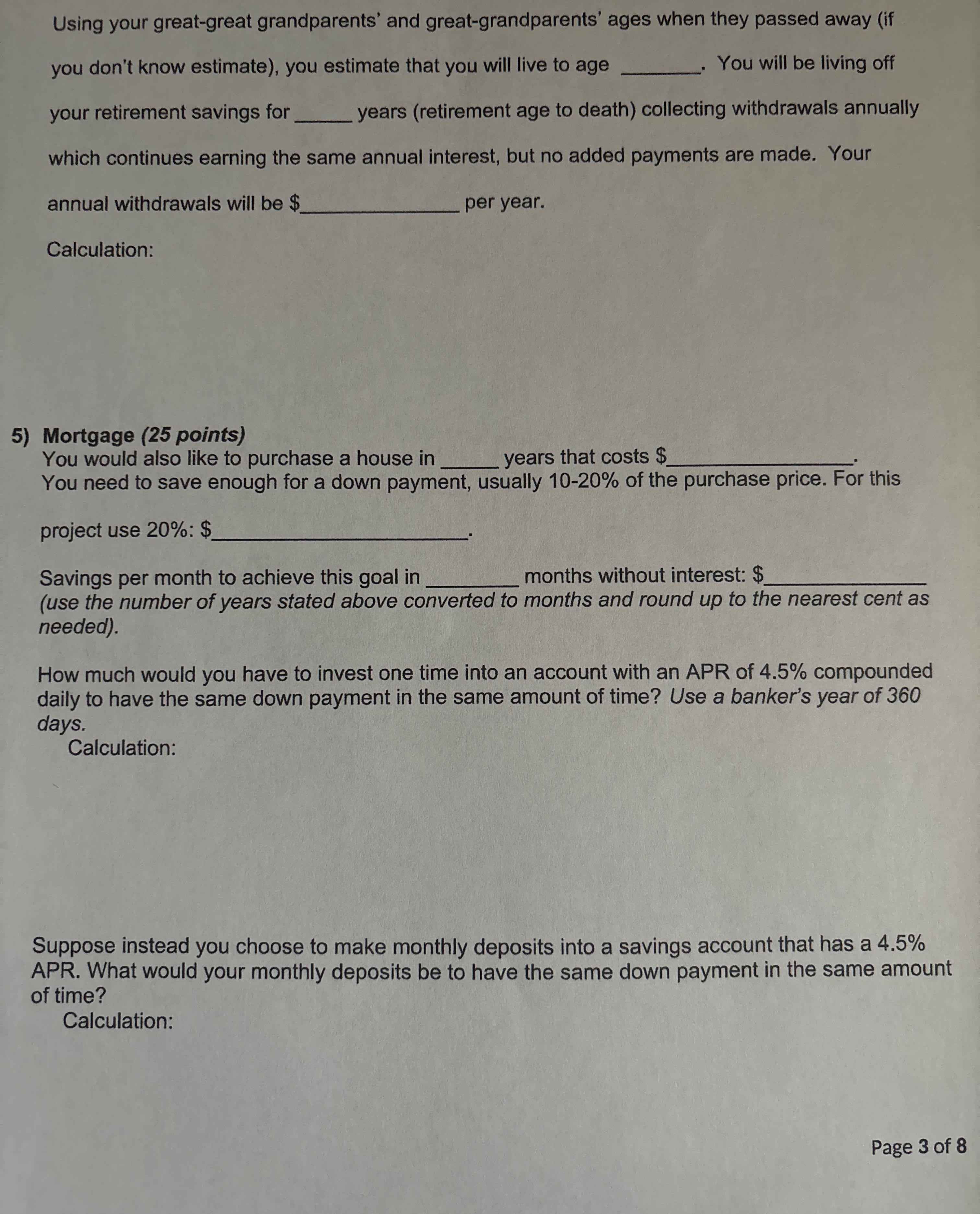

Life after College Budget Project This project will walk you through some post-college realities that you may or may not have pondered. Formulas you are permitted to use are listed in the box below. For any other formulas you wish to use, you must show work for how you derived them from the formulas below before receiving credit for using them. Future Value: FV=PMT- PMT=FV- 1+1-1 (1+1)-1 Compound Interest: A= P(1+1 FV amount after t years: irate per payment period number of payments n A Accumulated amount 1) College Loan (10 points) You choose to attend college at, 1-141) Present Value: PV=PMT- PMT=PV 1-1+/ PMT monthly payment PV Present value of a loan or annuity P = Principal which costs $ per year for tuition, roorn, and board. You spend years there for a total cost of $ You get a scholarship for you are also able to pay $ loan for $ outright. To pay for the remainder, you take out a (use $2000 if your scholarship and ability to pay outright brings the cost below this) for years at % APR compounded monthly from. (bank name). is your monthly college loan payment. Calculation: 2) Car Loan (10 points) Your car is nearing the end of its life. You must purchase another one-no leases - and it may be new or used. The cost of the car you want to purchase is: $ Your present car, worth may be used as a trade-in. Therefore you will be financing $ $1000 assume you have some car debt if trade-in covers it) for. compounded monthly at % APR from (minimum years (choose 2, 3, 4, 5, or 6 years) (bank name). a) Monthly car loan payment = $ Calculation: Page 1 of 8 3) Salary (6 points) Your job as a(n) has a median annual starting salary of $ Taxes are deducted from your salary. Calculate each for your annual salary. i) Federal income tax (assume you are taking the standard deduction): Taxable Income = Salary - Standard deduction = My filing status of choice is Therefore, my taxes will be calculated using the following formula: Federal Income Tax = $ ii) 7.6% FICA tax (note there is no standard deduction from your salary for this) Total taxes: $ Monthly net salary (take-home pay) = 4) Retirement Savings (16 points) You plan to start work at age salary-total taxes = $ 12 is the age at which you plan to start your career, and is the age at which you hope to retire. You will try to save per month in a mutual fund. Over time, this mutual fund earns 9.0% APR compounded monthly for years (start of work to retirement age) When you retire, your mutual fund is worth $ Calculation: Page 2 of 8 Using your great-great grandparents' and great-grandparents' ages when they passed away (if you don't know estimate), you estimate that you will live to age You will be living off your retirement savings for _ years (retirement age to death) collecting withdrawals annually which continues earning the same annual interest, but no added payments are made. Your annual withdrawals will be $ Calculation: per year. 5) Mortgage (25 points) You would also like to purchase a house in years that costs $ You need to save enough for a down payment, usually 10-20% of the purchase price. For this project use 20%: $ Savings per month to achieve this goal in months without interest: $ (use the number of years stated above converted to months and round up to the nearest cent as needed). How much would you have to invest one time into an account with an APR of 4.5% compounded daily to have the same down payment in the same amount of time? Use a banker's year of 360 days. Calculation: Suppose instead you choose to make monthly deposits into a savings account that has a 4.5% APR. What would your monthly deposits be to have the same down payment in the same amount of time? Calculation: Page 3 of 8 When purchasing the home, you would then finance $ for _ years (choose from either 15, 20, or 30) at % APR compounded monthly from (bank name). Monthly payment: $ Calculation: With this payment, how much will you eventually pay for your house? (monthly payment x months + down-payment) $ Calculation: Suppose you could only afford to pay half the monthly payment you found for the mortgage. How long would it take to pay off the mortgage? Work solving for n (please remember, you may only use the formulas on the first page of this document and need to show the steps for solving for n below): Page 4 of 8 6) Other Expenses (4 points) a) What other expenses will you be responsible for when you graduate and live on your own? Electric/Water/Sewage/Trash/Natural Gas Phone Gasoline (for car) Food Renter insurance Auto insurance Cable/streaming Internet Rent Other Expenses: TOTAL: $ 7) Monthly Balance (4 points) Net monthly salary - (college pmt + car pmt + mutual fund pmt + down pmt savings + mo. expenses) + + + + ) = $ 8) Credit Cards (20 points) a) Will credit cards help? The average undergraduate student leaves college with a diploma and around $2750 in credit card debt (graduate students, $4800). Suppose you have a credit card with a balance of $2750 and an interest rate of 19.8% APR. The minimum payment is $45.00. The amount of interest due each month is figured as current balance, where r is the rate (in decimal form) and n is 12. Fill in the table, making minimum payments. n Month Current balance Interest Payment Amount applied to principal 1 $2750.00 $45.38 $45.00 -$0.38 2 $2750.38 $45.00 345 $45.00 $45.00 $45.00 19 6 $45.00 7 $45.00 8 $45.00 9 $45.00 10 $45.00 11 $45.00 Page 5 of 8 12 $45.00 b) Will you ever be out of debt with the credit card company? Explain by using the Present value formula and solving for n. Work solving for n: c) Suppose you begin making a monthly payment of $75.00. Fill in the table. Current Month Interest Payment balance 1 $2750.00 $45.38 $75.00 Amount applied to principal $29.62 234567 $75.00 $75.00 $75.00 $75.00 $75.00 $75.00 8 $75.00 9 $75.00 10 $75.00 Page 6 of 8 Month Current balance Interest Payment Amount applied to principal 11 $75.00 12 $75.00 d) Will you ever be out of debt? Explain by using the Present value formula and solving for n. Work solving for n: e) How much must you pay per month to be out of debt in two years? Calculation: Page 7 of 8 9) (5 points) Type a brief summary about this assignment (6+ complete sentences, 1-2 paragraphs). What surprised you most in this unit? * What are a few other things that you have learned? * Describe at least one thing you will do this year to improve your financial future. * How else has this unit changed the plans that you have for your future (as a college student and when beginning your career)? Page 8 of 8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 College Loan Given Cost of college per year X Scholarship Y Loan amount Z if Z 2000 then Z 2000 Loan duration A years APR B Monthly payment formula ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

663e6d162ec08_956478.pdf

180 KBs PDF File

663e6d162ec08_956478.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Cases An Interactive Learning Approach

Authors: Steven M Glover, Douglas F Prawitt

4th Edition

0132423502, 978-0132423502