Answered step by step

Verified Expert Solution

Question

1 Approved Answer

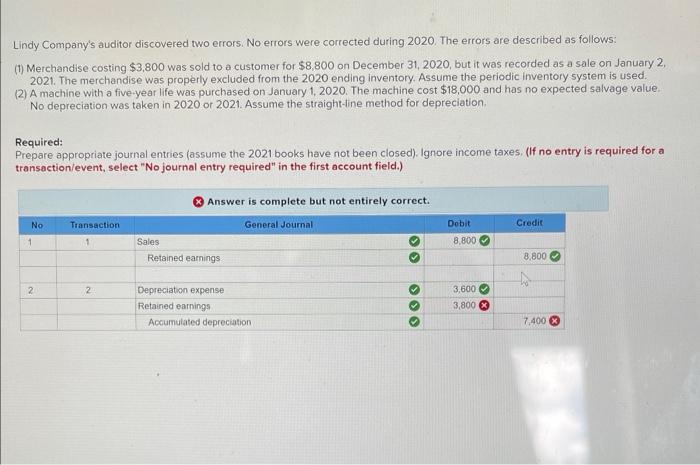

Lindy Company's auditor discovered two errors. No errors were corrected during 2020. The errors are described as follows: (1) Merchandise costing $3,800 was sold

Lindy Company's auditor discovered two errors. No errors were corrected during 2020. The errors are described as follows: (1) Merchandise costing $3,800 was sold to a customer for $8,800 on December 31, 2020, but it was recorded as a sale on January 2, 2021. The merchandise was properly excluded from the 2020 ending inventory. Assume the periodic inventory system is used. (2) A machine with a five-year life was purchased on January 1, 2020. The machine cost $18,000 and has no expected salvage value. No depreciation was taken in 2020 or 2021. Assume the straight-line method for depreciation. Required: Prepare appropriate journal entries (assume the 2021 books have not been closed). Ignore income taxes. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) 1 Answer is complete but not entirely correct. General Journal Debit Credit 8,800 8,800 No Transaction 1 Sales Retained earnings 2 2 Depreciation expense Retained earnings Accumulated depreciation, 3,600 3,800 7,400

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting Volume 1

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy

12th Canadian edition

119-49633-5, 1119496497, 1119496330, 978-1119496496