Answered step by step

Verified Expert Solution

Question

1 Approved Answer

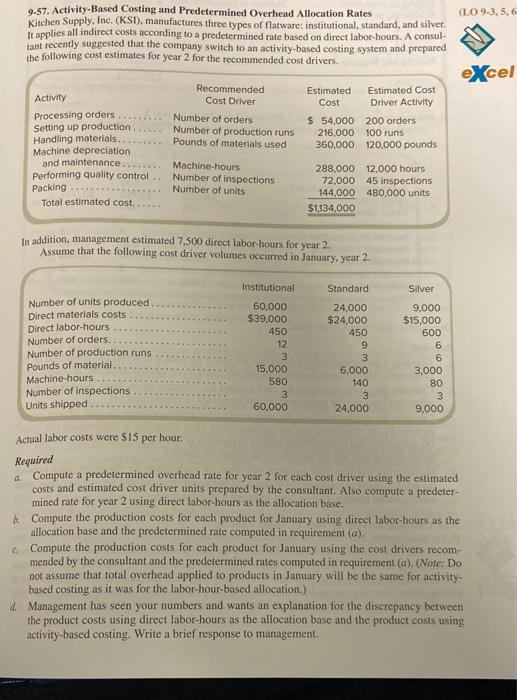

(LO 9-3,5,6 9-57. Activity-Based Costing and Predetermined Overhead Allocation Rates Kitchen Supply, Inc. (KSI), manufactures three types of flatware: institutional, standard, and silver It applies

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Financial Resources

Authors: Mick Broadbent, John Cullen

3rd Edition

1138134546, 978-1138134546