Answered step by step

Verified Expert Solution

Question

1 Approved Answer

looking for step by step solution as to how to solve. looking for formula to use, so that it can be applied to similar questions

looking for step by step solution as to how to solve. looking for formula to use, so that it can be applied to similar questions like this

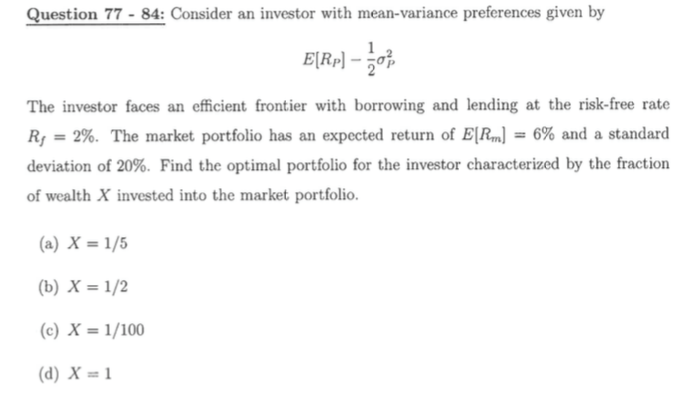

Question 77-84: Consider an investor with mean-variance preferences given by The investor faces an efficient frontier with borrowing and lending at the risk-free rate R, = 2%. The market portfolio has an expected return of Elk, 6% and a standard deviation of 20%. Find the optimal portfolio for the investor characterized by the fraction of wealth X invested into the market portfolio (a) X = 1/5 (b) X = 1/2 (c) X = l/100 (d) X= 1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

7th Edition

0073368717, 978-0073368719