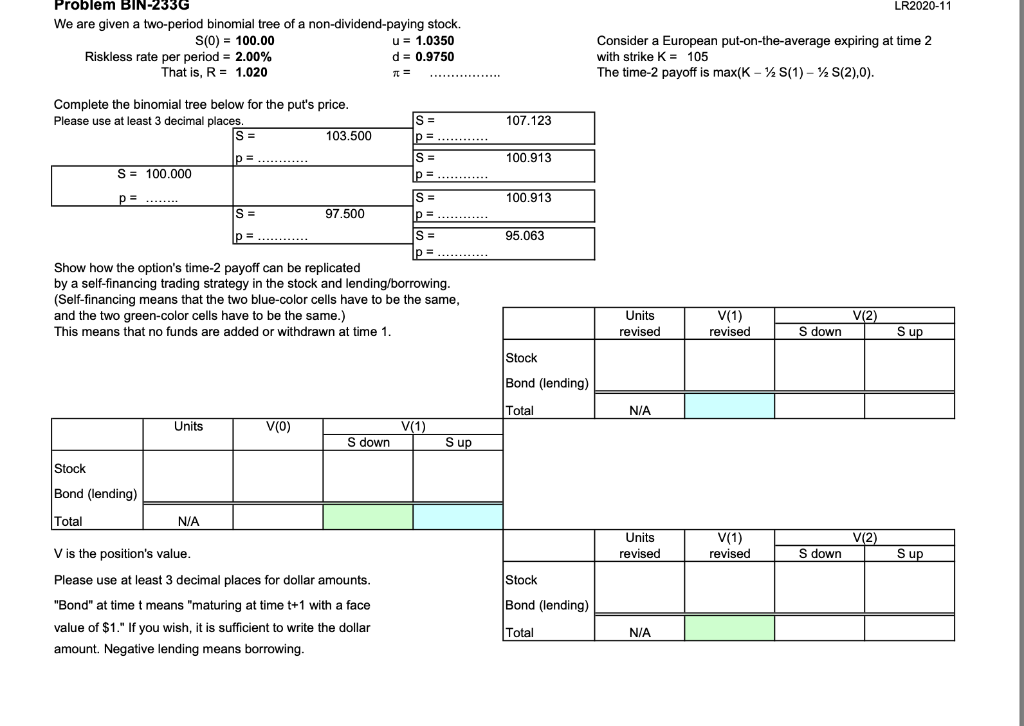

LR2020-11 Problem BIN-2336 We are given a two-period binomial tree of a non-dividend-paying stock. S(0) = 100.00 u= 1.0350 Riskless rate per period = 2.00% d = 0.9750 That is, R = 1.020 7 = Consider a European put-on-the-average expiring at time 2 with strike K = 105 The time-2 payoff is max(K - S(1) - S(2),0). Complete the binomial tree below for the put's price. Please use at least 3 decimal places. SE 103.500 107.123 S = p = S = 100.913 S = 100.000 p= 100.913 95.063 p= ...... S = S = 97.500 p = ....... P = ..... S = = p = Show how the option's time-2 payoff can be replicated by a self-financing trading strategy in the stock and lending/borrowing. (Self-financing means that the two blue-color cells have to be the same, and the two green-color cells have to be the same.) This means that no funds are added or withdrawn at time 1. V(2) Units revised V(1) revised S down Sup Stock Bond (lending) Total N/A Units V(0) V(1) S down Sup Stock Bond (lending) Total N/A V(2) Units revised V(1) revised V is the position's value. S down Sup Stock Bond (lending) Please use at least 3 decimal places for dollar amounts. "Bond" at time t means "maturing at time t+1 with a face value of $1." If you wish, it is sufficient to write the dollar amount. Negative lending means borrowing. Total N/A LR2020-11 Problem BIN-2336 We are given a two-period binomial tree of a non-dividend-paying stock. S(0) = 100.00 u= 1.0350 Riskless rate per period = 2.00% d = 0.9750 That is, R = 1.020 7 = Consider a European put-on-the-average expiring at time 2 with strike K = 105 The time-2 payoff is max(K - S(1) - S(2),0). Complete the binomial tree below for the put's price. Please use at least 3 decimal places. SE 103.500 107.123 S = p = S = 100.913 S = 100.000 p= 100.913 95.063 p= ...... S = S = 97.500 p = ....... P = ..... S = = p = Show how the option's time-2 payoff can be replicated by a self-financing trading strategy in the stock and lending/borrowing. (Self-financing means that the two blue-color cells have to be the same, and the two green-color cells have to be the same.) This means that no funds are added or withdrawn at time 1. V(2) Units revised V(1) revised S down Sup Stock Bond (lending) Total N/A Units V(0) V(1) S down Sup Stock Bond (lending) Total N/A V(2) Units revised V(1) revised V is the position's value. S down Sup Stock Bond (lending) Please use at least 3 decimal places for dollar amounts. "Bond" at time t means "maturing at time t+1 with a face value of $1." If you wish, it is sufficient to write the dollar amount. Negative lending means borrowing. Total N/A