Answered step by step

Verified Expert Solution

Question

1 Approved Answer

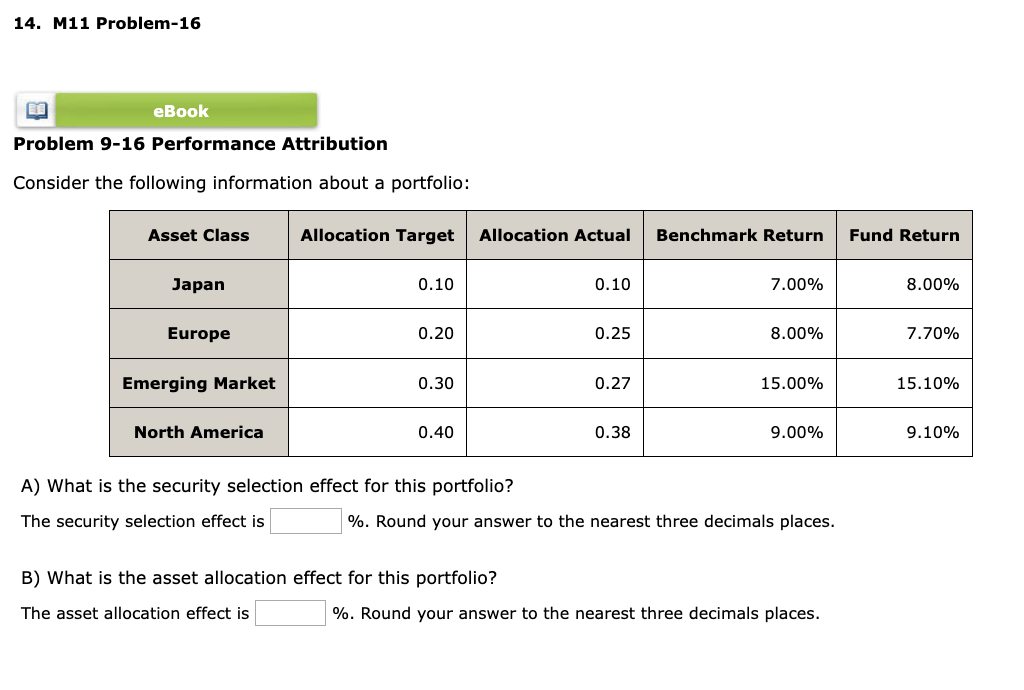

M 1 1 Problem - 1 6 Problem 9 - 1 6 Performance Attribution Consider the following information about a portfolio: table [ [

M Problem

Problem Performance Attribution

Consider the following information about a portfolio:

tableAsset Class,Allocation Target,Allocation Actual,Benchmark Return,Fund ReturnJapanEuropeEmerging Market,North America,

A What is the security selection effect for this portfolio?

The security selection effect is Round your answer to the nearest three decimals places.

B What is the asset allocation effect for this portfolio?

The asset allocation effect is Round your answer to the nearest three decimals places.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Financial Management

Authors: Glen Arnold, James Pickford

2nd Edition

0582821762, 978-0582821767