made up company -- Kipling will use the Accrual Method of accounting due to the size of their business. Kipling is owned by VF Corporation, a publicly traded business that owns an abundance of apparel companies, including The North Face, Timberland, and Vans. For VF Corporation and Kipling to get the most accurate picture of Kiplings profitability, they want to record their revenues as they are earned and their expenses as soon as they are incurred. As a large retail company where sales fluctuate by season, Kipling tracks their numbers quarterly. An accrual method gives a more accurate look at their profitability for the year.

Kipling will use a target price pricing strategy to determine the selling price. Currently, masks on the market range from $8 to $25 in price. Currently, all masks of the same type as Kipling masks are selling out in minutes as different retailers continue to replenish their website every few days. With demand being so high and Kipling being a well-known brand, a slight mark-up from the lower end of the price range will still remain competitive while still being conscious of the profit Kipling is aiming to make. Kipling masks will be priced at $12. Kipling currently produces fabric bags and accessories, meaning they already possess the necessary machinery and materials to produce masks. Non-medical grade masks are not expensive to produce; Kipling can produce the mask for 50 cents. The markup on Kipling masks is 2,300%, leaving Kipling with a large profit margin.

Create a 1year Master Budget (refers page 254 & 255 in the textbook) for the business/project.

Prepare Cash budget (and/or Cash Flow statement) and provide a brief analysis of cash flows from Operation, Investing and Financing activities (Cash flow statement analysis)

Break Even Analysis, Target Profit and Margin of Safety in units and Sales Dollars for the Business/Project

Discuss the Return on Investment and/or Economic Value Added for the business/program/project to measure its projected performance.

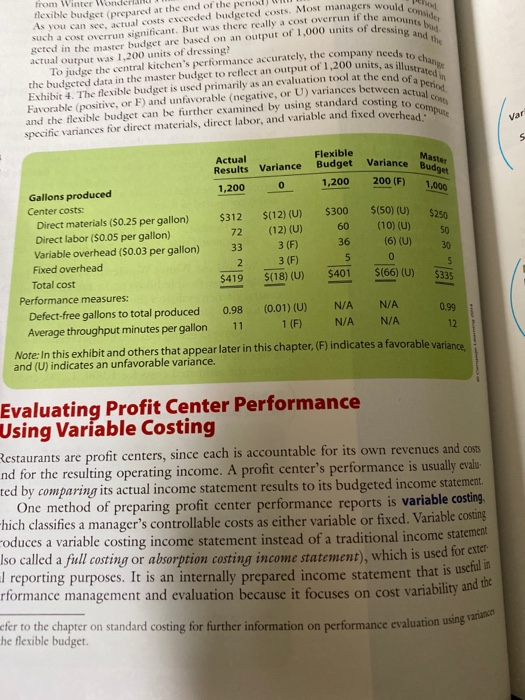

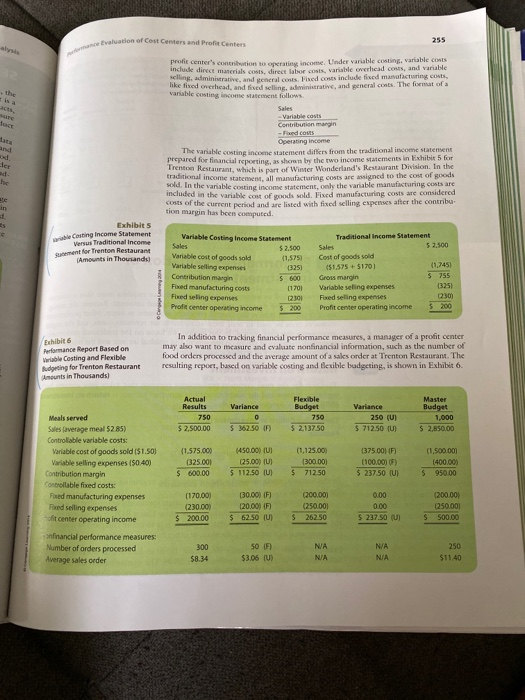

yod consider e amounts bus Aressing and the As to change Wustrated in from Winter Wonder Flexible budget prepared at the end of the period As you can see, actual costs exceeded budgeted costs. Most managers would such a cost overrun significant. But was there really a cost overrun if the amo geted in the master budget are based on an output of 1,000 units of dressin actual output was 1.200 units of dressing? To judge the central kitchen's performance accurately, the company needs to the budgeted data in the master budget to reflect an output of 1,200 units, as illus Exhibit +. The flexible budget is used primarily as an evaluation tool at the end of Favorable positive, or F) and unfavorable (negative, or U) variances between a and the flexible budget can be further examined by using standard costing to specific variances for direct materials, direct labor, and variable and fixed overbe end of a period ucen actual cos g, to compus 1,000 Flexible Actual Mas Results Variance Budget Variance Bester Gallons produced 1,200 0 1,200 200 (F) Center costs: $312 $(12) (0) $300 $(50) (U). Direct materials (50.25 per gallon) (12) (U) (10) (U) Direct labor ($0.05 per gallon) Variable overhead ($0.03 per gallon) 33 3 (F) (6) (0) Fixed overhead 3 (F) $419 Total cost $40 $(18) (U) $(66) (U) $335 Performance measures: Defect-free gallons to total produced 0.98 (0.01) (0) N/A N/A Average throughput minutes per gallon 11 1 (F) 1 (F) N/A N/A Note: In this exhibit and others that appear later in this chapter, (F) indicates a favorable varian and (U) indicates an unfavorable variance. 0.99 Evaluating Profit Center Performance Using Variable Costing Restaurants are profit centers, since each is accountable for its own revenues and costs nd for the resulting operating income. A profit center's performance is usually evalu- ted by comparing its actual income statement results to its budgeted income statement One method of preparing profit center performance reports is variable costing, hich classifies a manager's controllable costs as either variable or fixed. Variable costing, roduces a variable costing income statement instead of a traditional income statemem Iso called a full costing or absorption costing income statement), which is used for en a reporting purposes. It is an internally prepared income statement that is use rformance management and evaluation because it focuses on cost va aluation because it focuses on cost variability and the cfer to the chapter on standard costing for further information on performance evaluation using he flexible budget dation using variance tion of Cost Center ProfCentrs 255 center's t nuk merials ministrati and nike head and l variable cost income s raining direta s als His e ar fos Under variable cu v antable con yaralle tweed OS, and variable included manufacturing Cu n eral Cont. The formato e -Variations Contribuon margin The varie costing samm en from the traditional income statement duran ts in het Trento Restaurant, which is punter Wonderland Restaurant Division. In the traditional income statement, all manufacturing conte n ed to the cost of goods sold. In the variable costing income statement, only the variable manufacturing costs are included in the variable cost of gods sold. Fixed manufacturing costs are considered costs of the current period and are listed with fixed selling expenses after the contribu tion margin has been computed. Exhibits Casting Income Statement Versus Traditional income for Trenton Restaurant Amounts in Thousands Variable Costing Income Statement $ 2.500 Variable cost of goods sold (1.575) 3259 Combo 5600 a cturing costs Traditional income Statement Sales 5 2.500 Cost of goods sold 51.575 +5170) Gross margin Variabeling expenses Foedseling expenses Profitcenter operating income 5 200 F Profit center operating income $ 200 thibite Performance Report Based on wable Costing and Flexible Miting for Trenton Restaurant unts in Thousands) In addition to tracking financial performance measures, a manager of a profit center may also want to measure and evaluate nonfinancial information, such as the number of food orders processed and the average amount of a sales order at Trenton Restaurant. The resulting report, based on variable costing and flexible budgeting, is shown in Exhibit 6. Actual Results Variance Budget 750 Variance 250 (0) 5 712.50 Master Budget 1.000 5 205000 5 2.50000 5 362.50 5 213750 11.575.00 (325.00 $ 600.00 1450.00 (U) 125.00) U) 5112.50 (U) (1.135.00 (300 DOI 712.50 (375.00 (100.000) $ 23750 (U) (1.500.00 1400 950.00 $ Meals served Severage meat $285) Controllable variable costs Variable cost of goods sold ($1.50) Valable selling expenses (50.40) Contribution margin Controllable fixed costs Foxed manufacturing expenses ad selling expenses center operating income financial performance measures Number of orders processed Average sales order 0.00 (170.000 10.00 $ 200.00 30.000 FT 120.00) $ 62.50 000.00 (250.00 26250 0.00 (200.00 050001 500.00 $ $ 237.50 (U $ SO 53.06 NA NA NA NA 58.34 ) $11.40 yod consider e amounts bus Aressing and the As to change Wustrated in from Winter Wonder Flexible budget prepared at the end of the period As you can see, actual costs exceeded budgeted costs. Most managers would such a cost overrun significant. But was there really a cost overrun if the amo geted in the master budget are based on an output of 1,000 units of dressin actual output was 1.200 units of dressing? To judge the central kitchen's performance accurately, the company needs to the budgeted data in the master budget to reflect an output of 1,200 units, as illus Exhibit +. The flexible budget is used primarily as an evaluation tool at the end of Favorable positive, or F) and unfavorable (negative, or U) variances between a and the flexible budget can be further examined by using standard costing to specific variances for direct materials, direct labor, and variable and fixed overbe end of a period ucen actual cos g, to compus 1,000 Flexible Actual Mas Results Variance Budget Variance Bester Gallons produced 1,200 0 1,200 200 (F) Center costs: $312 $(12) (0) $300 $(50) (U). Direct materials (50.25 per gallon) (12) (U) (10) (U) Direct labor ($0.05 per gallon) Variable overhead ($0.03 per gallon) 33 3 (F) (6) (0) Fixed overhead 3 (F) $419 Total cost $40 $(18) (U) $(66) (U) $335 Performance measures: Defect-free gallons to total produced 0.98 (0.01) (0) N/A N/A Average throughput minutes per gallon 11 1 (F) 1 (F) N/A N/A Note: In this exhibit and others that appear later in this chapter, (F) indicates a favorable varian and (U) indicates an unfavorable variance. 0.99 Evaluating Profit Center Performance Using Variable Costing Restaurants are profit centers, since each is accountable for its own revenues and costs nd for the resulting operating income. A profit center's performance is usually evalu- ted by comparing its actual income statement results to its budgeted income statement One method of preparing profit center performance reports is variable costing, hich classifies a manager's controllable costs as either variable or fixed. Variable costing, roduces a variable costing income statement instead of a traditional income statemem Iso called a full costing or absorption costing income statement), which is used for en a reporting purposes. It is an internally prepared income statement that is use rformance management and evaluation because it focuses on cost va aluation because it focuses on cost variability and the cfer to the chapter on standard costing for further information on performance evaluation using he flexible budget dation using variance tion of Cost Center ProfCentrs 255 center's t nuk merials ministrati and nike head and l variable cost income s raining direta s als His e ar fos Under variable cu v antable con yaralle tweed OS, and variable included manufacturing Cu n eral Cont. The formato e -Variations Contribuon margin The varie costing samm en from the traditional income statement duran ts in het Trento Restaurant, which is punter Wonderland Restaurant Division. In the traditional income statement, all manufacturing conte n ed to the cost of goods sold. In the variable costing income statement, only the variable manufacturing costs are included in the variable cost of gods sold. Fixed manufacturing costs are considered costs of the current period and are listed with fixed selling expenses after the contribu tion margin has been computed. Exhibits Casting Income Statement Versus Traditional income for Trenton Restaurant Amounts in Thousands Variable Costing Income Statement $ 2.500 Variable cost of goods sold (1.575) 3259 Combo 5600 a cturing costs Traditional income Statement Sales 5 2.500 Cost of goods sold 51.575 +5170) Gross margin Variabeling expenses Foedseling expenses Profitcenter operating income 5 200 F Profit center operating income $ 200 thibite Performance Report Based on wable Costing and Flexible Miting for Trenton Restaurant unts in Thousands) In addition to tracking financial performance measures, a manager of a profit center may also want to measure and evaluate nonfinancial information, such as the number of food orders processed and the average amount of a sales order at Trenton Restaurant. The resulting report, based on variable costing and flexible budgeting, is shown in Exhibit 6. Actual Results Variance Budget 750 Variance 250 (0) 5 712.50 Master Budget 1.000 5 205000 5 2.50000 5 362.50 5 213750 11.575.00 (325.00 $ 600.00 1450.00 (U) 125.00) U) 5112.50 (U) (1.135.00 (300 DOI 712.50 (375.00 (100.000) $ 23750 (U) (1.500.00 1400 950.00 $ Meals served Severage meat $285) Controllable variable costs Variable cost of goods sold ($1.50) Valable selling expenses (50.40) Contribution margin Controllable fixed costs Foxed manufacturing expenses ad selling expenses center operating income financial performance measures Number of orders processed Average sales order 0.00 (170.000 10.00 $ 200.00 30.000 FT 120.00) $ 62.50 000.00 (250.00 26250 0.00 (200.00 050001 500.00 $ $ 237.50 (U $ SO 53.06 NA NA NA NA 58.34 ) $11.40