make 3 substantive responses for this artical

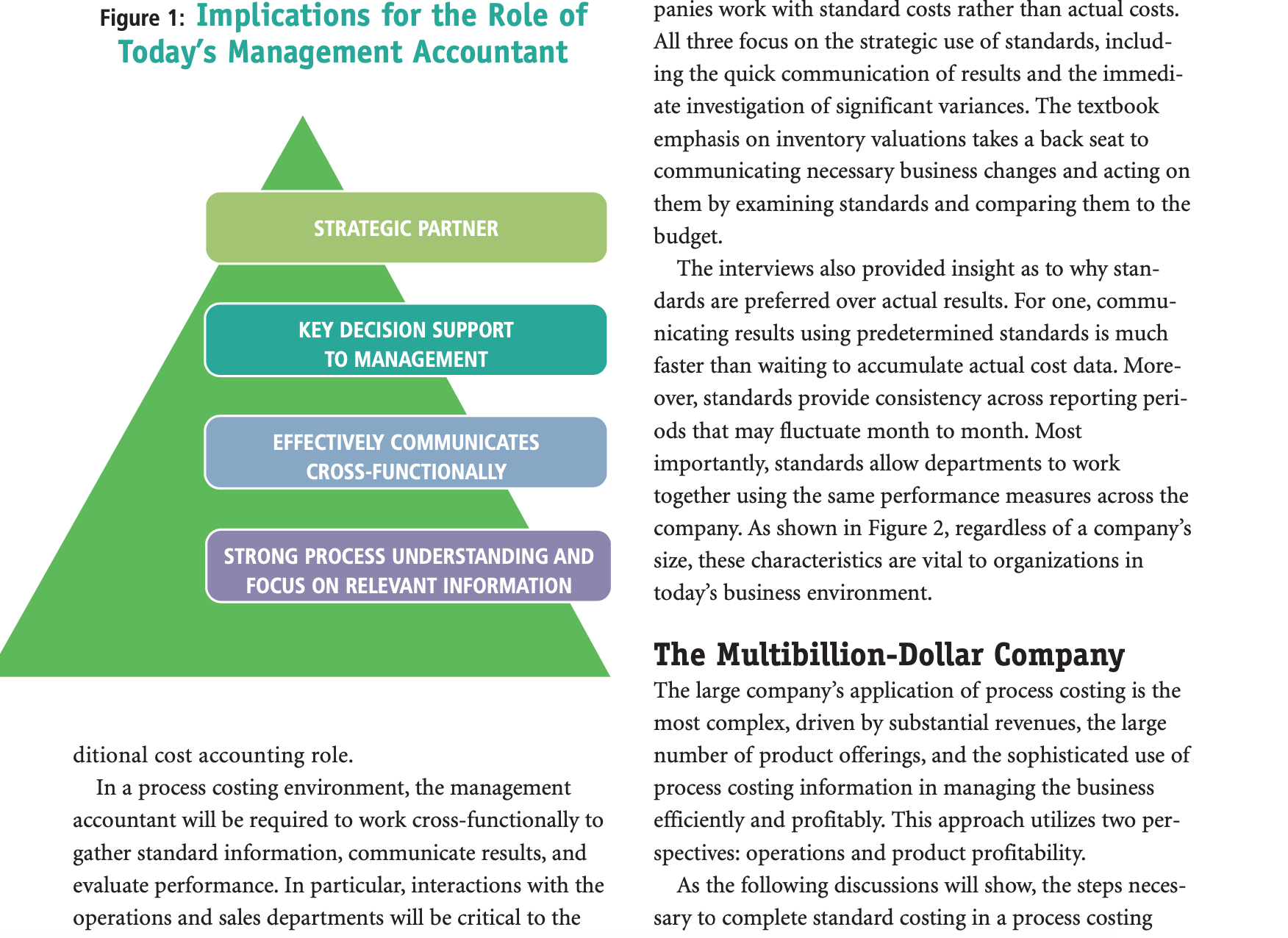

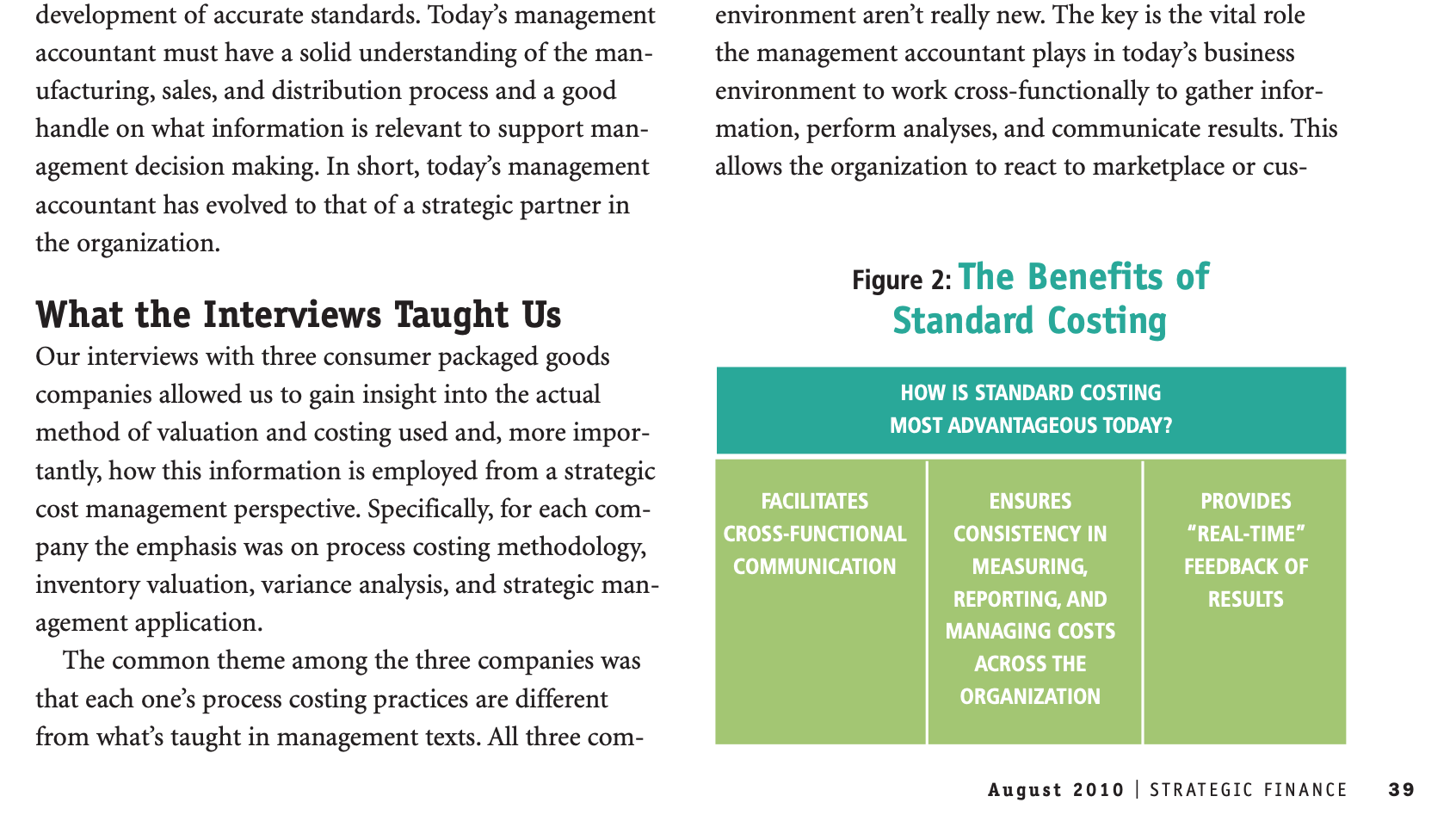

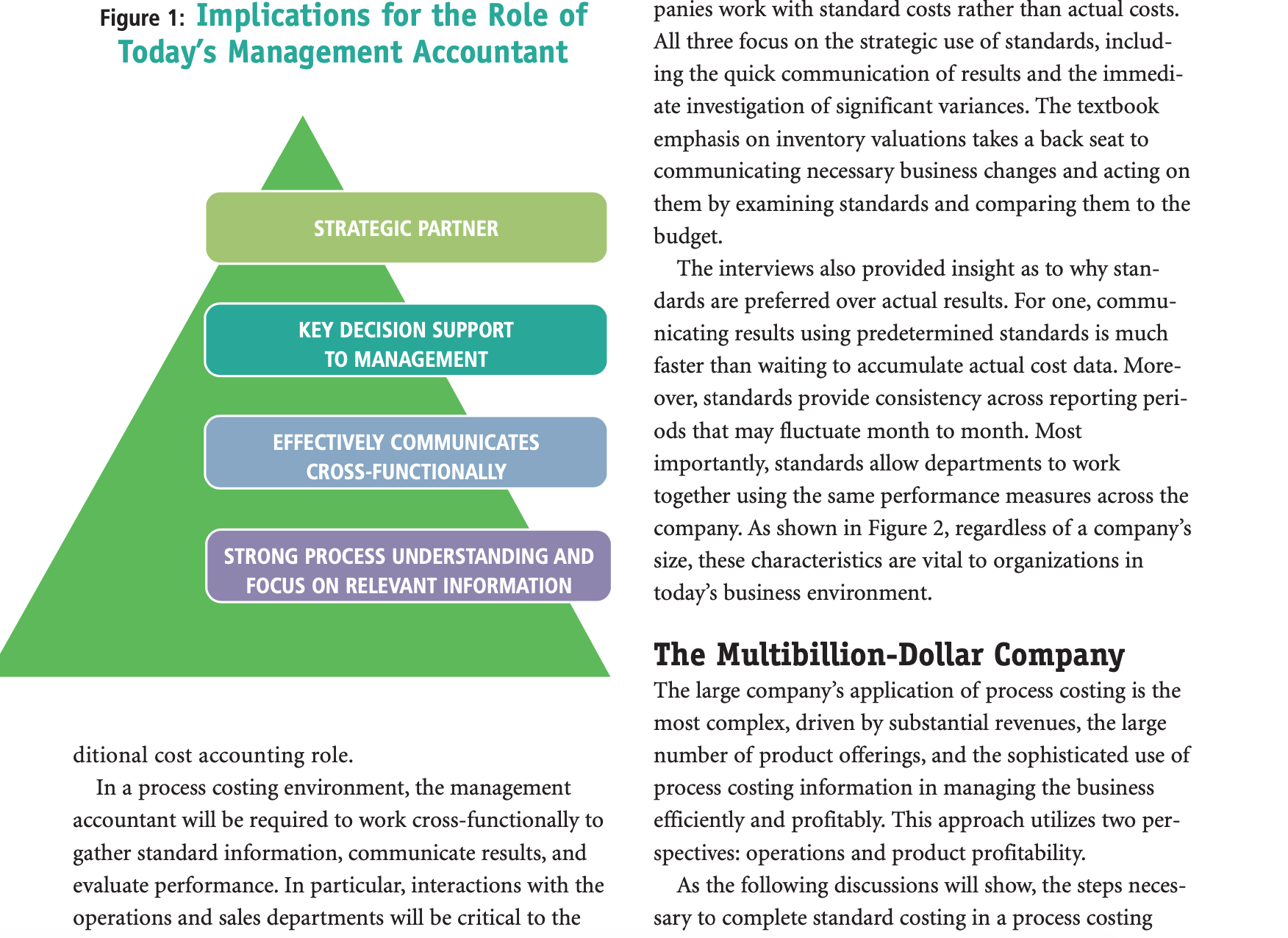

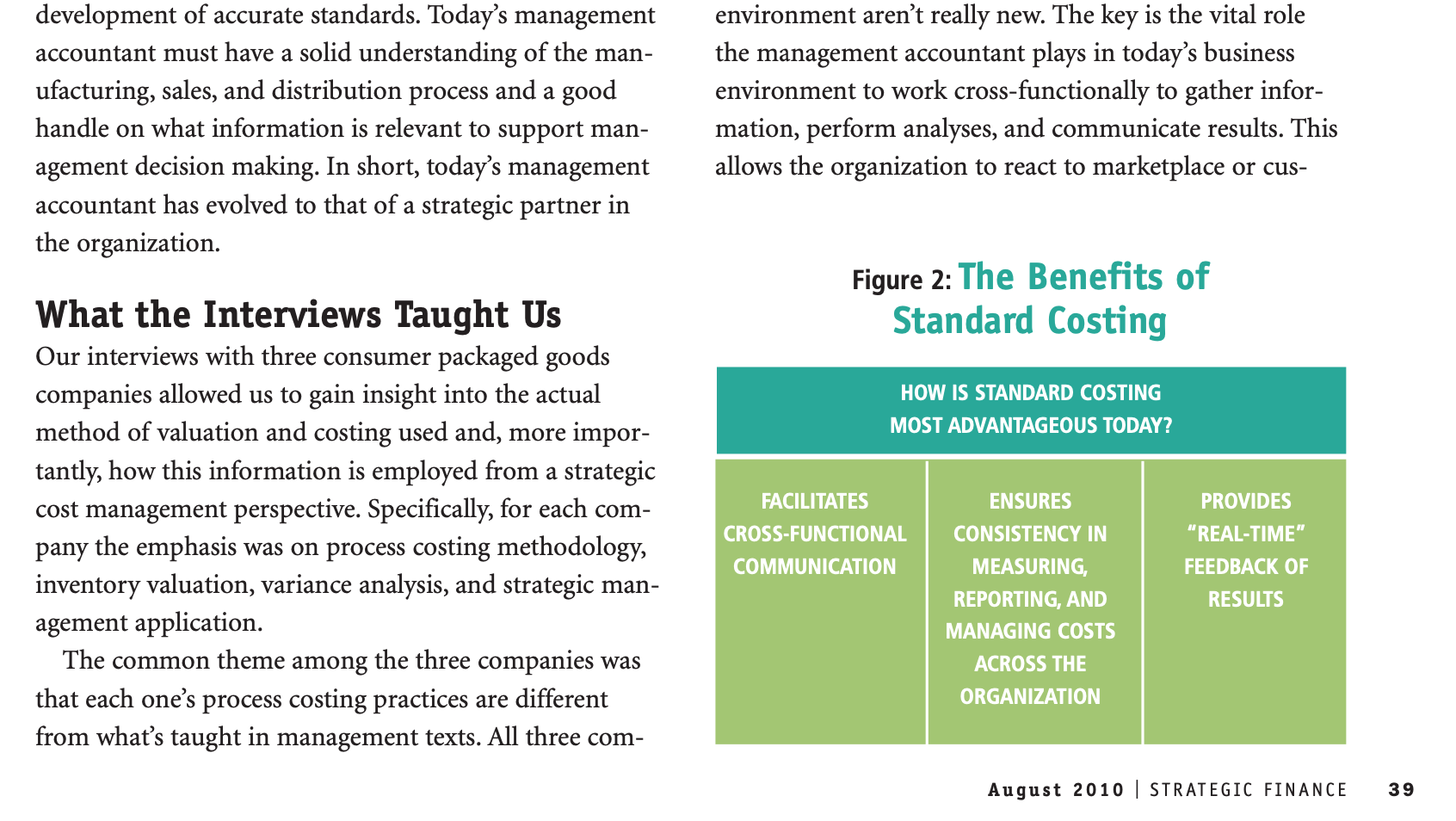

t's the classic \"either/or\" proposition in manufactur- ing settings, where assembly practices generally fol- low one of two tracks: job or process. The difference between the two is the ability to trace input costs to n- ished goods. A manufacturing process that requires spe- cic amounts of raw materials and labor to complete a unit is the job method. With job costing, the amount of raw materials and labor placed into production can be traced or specically identied to the nished good. A process method, on the other hand, involves the manufacture of large or mass quantities of identical units and is more complex because specic amounts of raw materials and labor can't be traced to nished goods. In a process manufacturing environment, raw materials, labor, and overhead placed into production need to be allocated to inventory. Given the difference in the ability to trace input costs of these two methods, the valuations The most signicant use for standards is as a strategic cost management tool, an how the use of standards can facilitate strategic cost man- agement, we conducted interviews with managers at three consumer packaged goods manufacturers. The homoge- neous nature of the packaged goods industry provides an ideal application of process costing. To provide a bal- anced perspective, we selected three companies varied in size and complexity: a large multibillion-dollar company, a $500 million company, and a small company. All of them use process costing and standardsin a manner ranging from straightforward to complexto help them manage their business protably. Theory of Process Costing Process costing is dened as an accounting methodology that tracks the production of large quantities of identical units. At the end of the period, units in production (work-in-process) and completed units (nished goods) must be valued for the balance sheet and income state- ment as required for external reporting. A popular text- book approach includes a ve-step method for allocating costs to inventory: Step 1: Summarize the ow of units: in process at the beginning of the period and placed into production. Step 2: Compute output: units completed and units in process at the end of the period. Step 3: Summarize total manufacturing costs The most significant use book approach includes a five-step method for allocating costs to inventory: for standards is as a strategic Step 1: Summarize the flow of units: in process at the beginning of the period and placed into production. cost management tool, an Step 2: Compute output: units completed and units in process at the end of the period. approach that's either ignored Step 3: Summarize total manufacturing costs incurred during the period. or limited to a description in Step 4: Compute manufacturing costs per unit. Step 5: Assign manufacturing costs to units completed most textbooks. and ending work-in-process. The textbook focus is clearly on the "calculation." Exer- cises and problems focus on the mathematical comple- tion of allocating manufacturing costs to ending of work-in-process and finished goods inventories differ work-in-process and finished goods using the five-step significantly. method. The discussion of process costing generally stops The topic of process costing as often presented in text- here. Little or no significant discussion is found in text- books is simplified and doesn't reflect industry practice. books on how management uses process costing to man- The primary difference is the textbook assumption that age the manufacturing operations. The emphasis is on actual costs incurred each month are reflected in valuing providing values for work-in-process and finished inven- inventory and cost of goods sold. In practice, predeter- tory for external reporting. mined standard costs-not actual ones-are used. Valua- The textbooks generally place the management tion and costing are important aspects when discussing accountant in a traditional cost accounting role, focus- standards. But potentially the most significant use for ing on the calculation of results for financial state- standards is as a strategic cost management tool, an ments. Little discussion is devoted to interpersonal and approach that's either ignored or limited to a description analytical/strategic management skills (see Figure 1). in most textbooks. Thus, many management accountants The role of the management accountant in a manufac are untrained or unaware of the many potential uses of turing firm that utilizes process costing is best lever-Figure 1: Implications for the Role of Today's Management Accountant KEY DECISION SUPPORT TO MANAGEMENT EFFECTIVELY COMMUNICATES CROSS-FUNCTIONALLY STRONG PROCESS UNDERSTANDING AND FOCUS ON RELEVANT INFORMATION ditional cost accounting role. In a process costing environment, the management accountant will be required to work crossfunctionally to gather standard information, communicate results, and evaluate performance. In particular, interactions with the operations and sales departments will be critical to the panies work with standard costs rather than actual costs. All three focus on the strategic use of standards, includ- ing the quick communication of results and the immedi ate investigation of signicant variances. The textbook emphasis on inventory valuations takes a back seat to communicating necessary business changes and acting on them by examining standards and comparing them to the budget. The interviews also provided insight as to why stan- dards are preferred over actual results. For one, commu- nicating results using predetermined standards is much faster than waiting to accumulate actual cost data. More- over, standards provide consistency across reporting peri- ods that may uctuate month to month. Most importantly, standards allow departments to work together using the same performance measures across the company. As shown in Figure 2, regardless of a company's size, these characteristics are vital to organizations in today's business environment. The Multibillion-Dollar Company The large company's application of process costing is the most complex, driven by substantial revenues, the large number of product offerings, and the sophisticated use of process costing information in managing the business efciently and protably. This approach utilizes two per spectives: operations and product protability. As the following discussions will show, the steps neces sary to complete standard costing in a process costing development of accurate standards. Today's management accountant must have a solid understanding of the man- ufacturing, sales, and distribution process and a good handle on what information is relevant to support man- agement decision making. In short, today's management accountant has evolved to that of a strategic partner in the organization. What the Interviews Taught Us Our interviews with three consumer packaged goods companies allowed us to gain insight into the actual method of valuation and costing used and, more impor- tantly, how this information is employed from a strategic cost management perspective. Specically, for each com- pany the emphasis was on process costing methodology, inventory valuation, variance analysis, and strategic man- agement application. The common theme among the three companies was that each one's process costing practices are different from what's taught in management texts. All three com- environment aren't really new. The key is the vital role the management accountant plays in today's business environment to work cross-functionally to gather infor- mation, perform analyses, and communicate results. This allows the organization to react to marketplace or cus- Figure 2: The Benets of Standard Costing HOW IS STANDARD COSTING MOST ADVANTAGEOUS TODAY? FACILITATES ENSURES PROVIDES CROSS-FUNCTIONAL CONSISTENCY IN "REAL-TIME" COMMUNICATION MEASURINGl FEEDBACK OF REPORTING, AND RESULTS MANAGING COSTS ACROSS THE ORGANIZATION August 2010 l STRATEGIC FINANCE 39