Question: make project note on all CVP Analysis and Decision Making Decision Maximum Contribution is obtained from Product Wye. So, WYE would be manufactured by ...

make project note on all

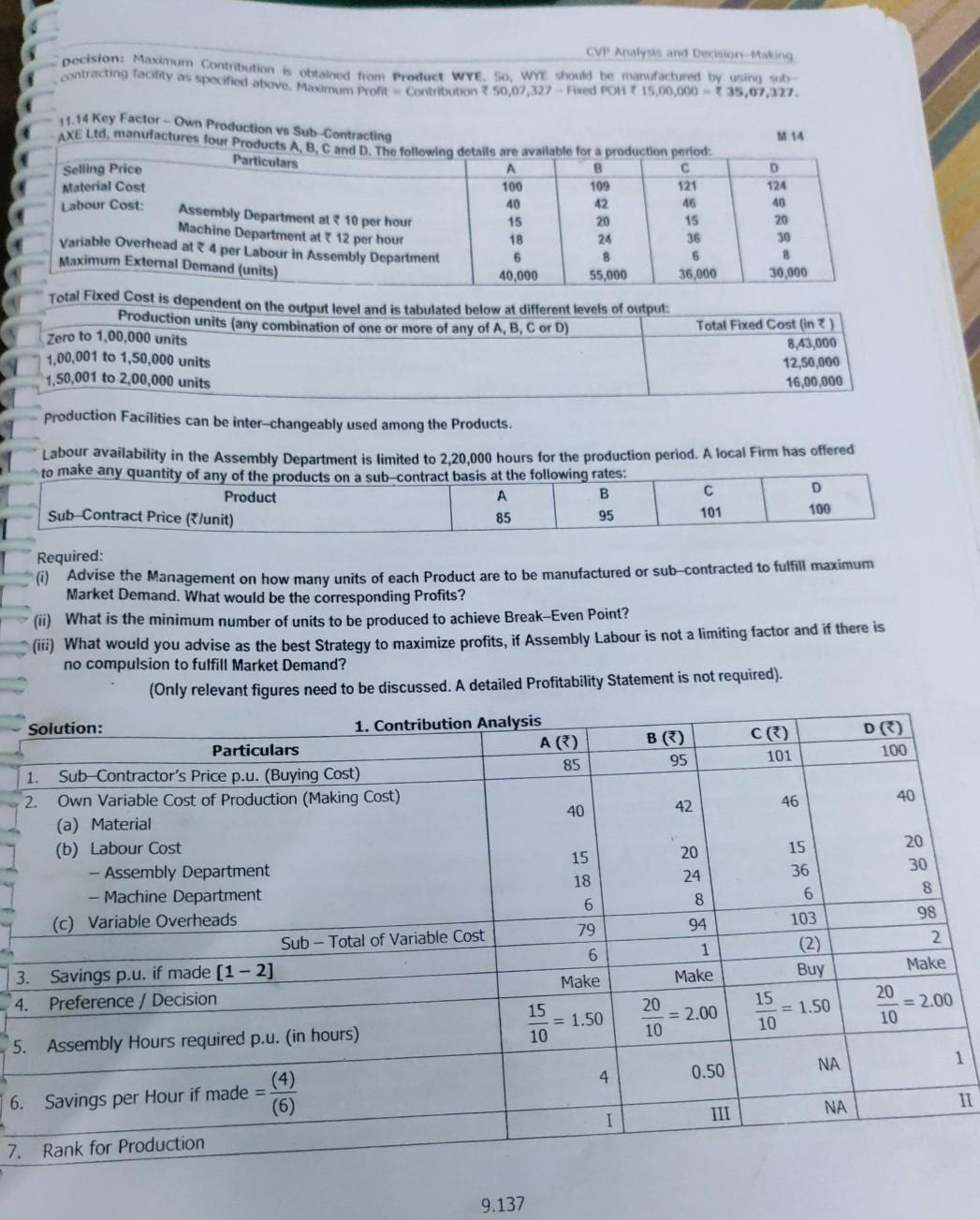

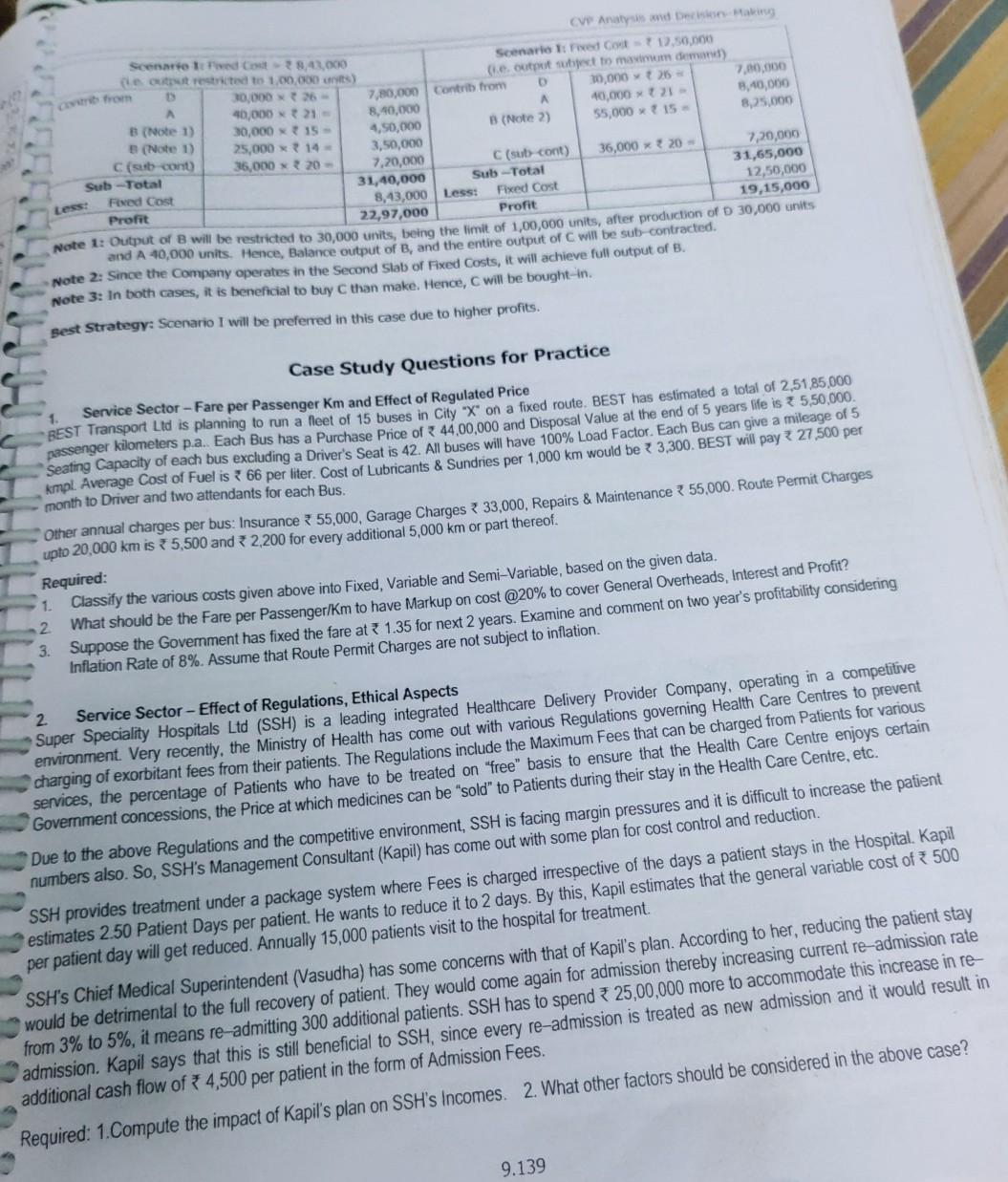

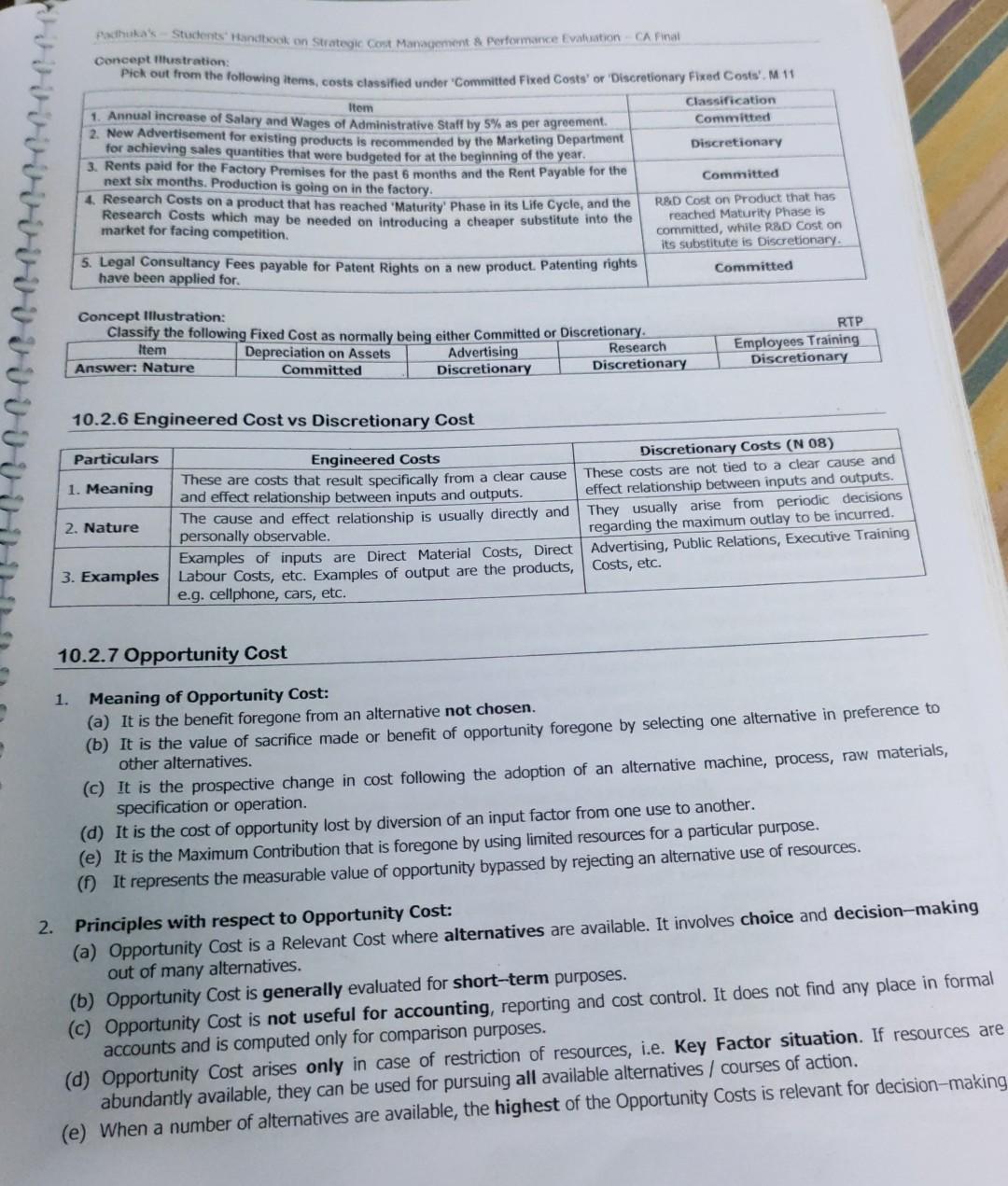

CVP Analysis and Decision Making Decision Maximum Contribution is obtained from Product Wye. So, WYE would be manufactured by ... contracting facility as spected above. Maximum Pom contribution 2 50,07,327 - Fived POH ? 15,00,000 - 35,07,321. 11.14 Key Factor-Own Production vs Sub-Contracting AXE Ltd, manufactures four Products A, B, C and D. The following details are available for a production period: Particulars Assembly Department at 10 per hour Machine Department at 12 per hour Variable Overhead at 4 per Labour in Assembly Department Maximum Extemal Domand (units) D A B 85 95 M14 Selling Price A B D Material Cost 100 109 121 Labour Cost: 124 40 42 46 40 15 20 15 20 18 24 36 30 6 8 6 8 40,000 55,000 36.000 30,000 Total Fixed Cost is dependent on the output level and is tabulated below at different levels of output: Production units (any combination of one or more of any of A, B, C or D) Zero to 1,00,000 units Total Fixed Cost (in) 1,00,001 to 1,50,000 units 8,43,000 1,50,001 to 2,00,000 units 12,50.000 16,00,000 Production Facilities can be inter-changeably used among the Products. Labour availability in the Assembly Department is limited to 2,20,000 hours for the production period. A local Firm has offered to make any quantity of any of the products on a sub-contract basis at the following rates: Product Sub-Contract Price (lunit) 101 100 Required: Advise the Management on how many units of each Product are to be manufactured or sub-contracted to fulfill maximum Market Demand. What would be the corresponding Profits? (ii) What is the minimum number of units to be produced to achieve Break-Even Point? (iii) What would you advise as the best Strategy to maximize profits, if Assembly Labour is not a limiting factor and if there is no compulsion to fulfill Market Demand? (Only relevant figures need to be discussed. A detailed profitability Statement is not required). Solution: 1. Contribution Analysis Particulars A) B) C) D) 1. 100 Sub-Contractor's Price p.u. (Buying Cost) 85 95 101 2 Own Variable Cost of Production (Making Cost) 42 40 46 40 (a) Material (b) Labour Cost 20 15 15 20 - Assembly Department 30 36 18 24 - Machine Department 8 6 8 6 (c) Variable Overheads 79 94 98 103 Sub - Total of Variable Cost (2) 2 6 3. Savings p.u. if made (1 -2] Make Make Buy Make 4. Preference / Decision 15 20 20 15 = 2.00 = 1.50 = 2.00 10 10 10 5. Assembly Hours required p.u. (in hours) 10 1 = 1.50 NA 4 0.50 NA 11 (4) 6. Savings per Hour if made = (6) 7 Rank for Production I III 9.137 from CV Analysis and Decision Making Scenario tried Cod 8.42.000 Scenario 1: Fived Cod 12.50,000 e out restricted to 1,00,000) (output subject to main demand) 30.00036 7,80,000 Contrib from D 30,000 25 7.00,000 40,000 21 8,10,000 10,000 8,40,000 B (Note 1) 30,000 x 15 B (Note 2) 4,50.000 55,000x15 8,25,000 B (Note 1) 25,000 x 14 C (sub cont 3,50,000 36,000 x 20 C(sub cont) 7,20,000 36,000 x 20 - 7.20,000 Sub -Total Sub-Total 31,40,000 31,65,000 Fixed Cost 8,43,000 Less: Fixed Cost 12,50,000 Profit 22,97,000 Profit 19,15,000 Note : Output of B will be restricted to 30,000 units, being the limit of 1,00,000 units, after production of D 30,000 units and A 40,000 units. Hence, Balance output of B, and the entire output of C will be sub contracted. Note 2: Since the Company operates in the Second Slab of Fixed Costs, it will achieve full output of 8. Note 3: In both cases, it is beneficial to buy C than make. Hence, will be bought in. sest Strategy: Scenario I will be preferred in this case due to higher profits. Less: 1. Case Study Questions for Practice Service Sector - Fare per Passenger Km and Effect of Regulated Price BEST Transport Ltd is planning to run a fleet of 15 buses in City -X on a fixed route. BEST has estimated a total of 2,51,85.000 passenger kilometers p.a.. Each Bus has a Purchase Price of 44.00,000 and Disposal Value at the end of 5 years life is = 5,50,000. Seating Capacity of each bus excluding a Driver's Seat is 42. All buses will have 100% Load Factor. Each Bus can give a mileage of 5 kmpl . Average cost of Fuel is 66 per liter. Cost of Lubricants & Sundries per 1,000 km would be ? 3,300. BEST will pay + 27 500 per month to Driver and two attendants for each Bus. Other annual charges per bus: Insurance 3 55,000, Garage Charges 33,000, Repairs & Maintenance 55,000. Route Permit Charges upto 20,000 km is 5,500 and 2,200 for every additional 5,000 km or part thereof. Required: 1. Classify the various costs given above into Fixed, Variable and Semi-Variable, based on the given data. What should be the Fare per Passenger/Km to have Markup on cost @20% to cover General Overheads, Interest and Profit? 3. Suppose the Government has fixed the fare at * 1.35 for next 2 years. Examine and comment on two year's profitability considering Inflation Rate of 8%. Assume that Route Permit Charges are not subject to inflation. 2 2 Service Sector-Effect of Regulations, Ethical Aspects Super Speciality Hospitals Ltd (SSH) is a leading integrated Healthcare Delivery Provider Company, operating in a competitive environment. Very recently, the Ministry of Health has come out with various Regulations governing Health Care Centres to prevent charging of exorbitant fees from their patients. The Regulations include the Maximum Fees that can be charged from Patients for various services, the percentage of Patients who have to be treated on "free" basis to ensure that the Health Care Centre enjoys certain Government concessions, the Price at which medicines can be "sold" to Patients during their stay in the Health Care Centre, etc. Due to the above Regulations and the competitive environment, SSH is facing margin pressures and it is difficult to increase the patient numbers also. So, SSH's Management Consultant (Kapil) has come out with some plan for cost control and reduction. SSH provides treatment under a package system where Fees is charged irrespective of the days a patient stays in the Hospital. Kapil estimates 2.50 Patient Days per patient. He wants to reduce it to 2 days. By this, Kapil estimates that the general variable cost of 500 per patient day will get reduced. Annually 15,000 patients visit to the hospital for treatment SSH's Chief Medical Superintendent (Vasudha) has some concerns with that of Kapil's plan. According to her, reducing the patient stay would be detrimental to the full recovery of patient. They would come again for admission thereby increasing current re-admission rate from 3% to 5%, it means re-admitting 300 additional patients. SSH has to spend 25,00,000 more to accommodate this increase in re admission. Kapil says that this is still beneficial to SSH, since every re-admission is treated as new admission and it would result in additional cash flow of 4,500 per patient in the form of Admission Fees. Required: 1.Compute the impact of Kapil's plan on SSH's Incomes. 2. What other factors should be considered in the above case? 9.139 Pothuka's Students and took on Strategic Cont Management & Performance Evaluation CAP Concept Illustration: Pick out from the following terms, costs classified under Committed Fixed Costs' or Discretionary Fixed Conta". M11 Item Classification Committed Discretionary Committed 1. Annual increase of Salary and Wages of Administrative Staff by 5% as per agreement. 2. New Advertisement for existing products is recommended by the Marketing Department for achieving sales quantities that were budgeted for at the beginning of the year. 3. Rents paid for the Factory Premises for the past 6 months and the Rent Payable for the next six months. Production is going on in the factory. 4. Research Costs on a product that has reached Maturity' Phase in its Life Cycle, and the Research Costs which may be needed on introducing a cheaper substitute into the market for facing competition. 5. Legal Consultancy Fees payable for Patent Rights on a new product. Patenting rights have been applied for. RBD Cost on Product that has reached Maturity Phase is committed, while R&D Cost on its substitute is Discretionary Committed Concept Illustration: Classify the following Fixed Cost as normally being either Committed or Discretionary Item Depreciation on Assets Advertising Research Answer: Nature Committed Discretionary Discretionary RTP Employees Training Discretionary 10.2.6 Engineered Cost vs Discretionary Cost Particulars Engineered Costs Discretionary Costs (N 08) 1. Meaning These are costs that result specifically from a clear cause These costs are not tied to a clear cause and and effect relationship between inputs and outputs. effect relationship between inputs and outputs. 2. Nature The cause and effect relationship is usually directly and They usually arise from periodic decisions personally observable. regarding the maximum outlay to be incurred. Examples of inputs are Direct Material Costs, Direct Advertising, Public Relations, Executive Training 3. Examples Labour Costs, etc. Examples of output are the products, Costs, etc. e.g. cellphone, cars, etc. 10.2.7 Opportunity Cost 1. Meaning of Opportunity Cost: (a) It is the benefit foregone from an alternative not chosen. (b) It is the value of sacrifice made or benefit of opportunity foregone by selecting one alternative in preference to other alternatives. (C) It is the prospective change in cost following the adoption of an alternative machine, process, raw materials, specification or operation. (d) It is the cost of opportunity lost by diversion of an input factor from one use to another. (e) It is the Maximum Contribution that is foregone by using limited resources for a particular purpose. (0It represents the measurable value of opportunity bypassed by rejecting an alternative use of resources. 2. Principles with respect to Opportunity Cost: (a) Opportunity Cost is a Relevant Cost where alternatives are available. It involves choice and decision-making out of many alternatives. (b) Opportunity Cost is generally evaluated for short-term purposes. (c) Opportunity Cost is not useful for accounting, reporting and cost control. It does not find any place in formal accounts and is computed only for comparison purposes. (d) Opportunity Cost arises only in case of restriction of resources, i.e. Key Factor situation. If resources are abundantly available, they can be used for pursuing all available alternatives / courses of action. (e) When a number of alternatives are available, the highest of the Opportunity Costs is relevant for decision-making CVP Analysis and Decision Making Decision Maximum Contribution is obtained from Product Wye. So, WYE would be manufactured by ... contracting facility as spected above. Maximum Pom contribution 2 50,07,327 - Fived POH ? 15,00,000 - 35,07,321. 11.14 Key Factor-Own Production vs Sub-Contracting AXE Ltd, manufactures four Products A, B, C and D. The following details are available for a production period: Particulars Assembly Department at 10 per hour Machine Department at 12 per hour Variable Overhead at 4 per Labour in Assembly Department Maximum Extemal Domand (units) D A B 85 95 M14 Selling Price A B D Material Cost 100 109 121 Labour Cost: 124 40 42 46 40 15 20 15 20 18 24 36 30 6 8 6 8 40,000 55,000 36.000 30,000 Total Fixed Cost is dependent on the output level and is tabulated below at different levels of output: Production units (any combination of one or more of any of A, B, C or D) Zero to 1,00,000 units Total Fixed Cost (in) 1,00,001 to 1,50,000 units 8,43,000 1,50,001 to 2,00,000 units 12,50.000 16,00,000 Production Facilities can be inter-changeably used among the Products. Labour availability in the Assembly Department is limited to 2,20,000 hours for the production period. A local Firm has offered to make any quantity of any of the products on a sub-contract basis at the following rates: Product Sub-Contract Price (lunit) 101 100 Required: Advise the Management on how many units of each Product are to be manufactured or sub-contracted to fulfill maximum Market Demand. What would be the corresponding Profits? (ii) What is the minimum number of units to be produced to achieve Break-Even Point? (iii) What would you advise as the best Strategy to maximize profits, if Assembly Labour is not a limiting factor and if there is no compulsion to fulfill Market Demand? (Only relevant figures need to be discussed. A detailed profitability Statement is not required). Solution: 1. Contribution Analysis Particulars A) B) C) D) 1. 100 Sub-Contractor's Price p.u. (Buying Cost) 85 95 101 2 Own Variable Cost of Production (Making Cost) 42 40 46 40 (a) Material (b) Labour Cost 20 15 15 20 - Assembly Department 30 36 18 24 - Machine Department 8 6 8 6 (c) Variable Overheads 79 94 98 103 Sub - Total of Variable Cost (2) 2 6 3. Savings p.u. if made (1 -2] Make Make Buy Make 4. Preference / Decision 15 20 20 15 = 2.00 = 1.50 = 2.00 10 10 10 5. Assembly Hours required p.u. (in hours) 10 1 = 1.50 NA 4 0.50 NA 11 (4) 6. Savings per Hour if made = (6) 7 Rank for Production I III 9.137 from CV Analysis and Decision Making Scenario tried Cod 8.42.000 Scenario 1: Fived Cod 12.50,000 e out restricted to 1,00,000) (output subject to main demand) 30.00036 7,80,000 Contrib from D 30,000 25 7.00,000 40,000 21 8,10,000 10,000 8,40,000 B (Note 1) 30,000 x 15 B (Note 2) 4,50.000 55,000x15 8,25,000 B (Note 1) 25,000 x 14 C (sub cont 3,50,000 36,000 x 20 C(sub cont) 7,20,000 36,000 x 20 - 7.20,000 Sub -Total Sub-Total 31,40,000 31,65,000 Fixed Cost 8,43,000 Less: Fixed Cost 12,50,000 Profit 22,97,000 Profit 19,15,000 Note : Output of B will be restricted to 30,000 units, being the limit of 1,00,000 units, after production of D 30,000 units and A 40,000 units. Hence, Balance output of B, and the entire output of C will be sub contracted. Note 2: Since the Company operates in the Second Slab of Fixed Costs, it will achieve full output of 8. Note 3: In both cases, it is beneficial to buy C than make. Hence, will be bought in. sest Strategy: Scenario I will be preferred in this case due to higher profits. Less: 1. Case Study Questions for Practice Service Sector - Fare per Passenger Km and Effect of Regulated Price BEST Transport Ltd is planning to run a fleet of 15 buses in City -X on a fixed route. BEST has estimated a total of 2,51,85.000 passenger kilometers p.a.. Each Bus has a Purchase Price of 44.00,000 and Disposal Value at the end of 5 years life is = 5,50,000. Seating Capacity of each bus excluding a Driver's Seat is 42. All buses will have 100% Load Factor. Each Bus can give a mileage of 5 kmpl . Average cost of Fuel is 66 per liter. Cost of Lubricants & Sundries per 1,000 km would be ? 3,300. BEST will pay + 27 500 per month to Driver and two attendants for each Bus. Other annual charges per bus: Insurance 3 55,000, Garage Charges 33,000, Repairs & Maintenance 55,000. Route Permit Charges upto 20,000 km is 5,500 and 2,200 for every additional 5,000 km or part thereof. Required: 1. Classify the various costs given above into Fixed, Variable and Semi-Variable, based on the given data. What should be the Fare per Passenger/Km to have Markup on cost @20% to cover General Overheads, Interest and Profit? 3. Suppose the Government has fixed the fare at * 1.35 for next 2 years. Examine and comment on two year's profitability considering Inflation Rate of 8%. Assume that Route Permit Charges are not subject to inflation. 2 2 Service Sector-Effect of Regulations, Ethical Aspects Super Speciality Hospitals Ltd (SSH) is a leading integrated Healthcare Delivery Provider Company, operating in a competitive environment. Very recently, the Ministry of Health has come out with various Regulations governing Health Care Centres to prevent charging of exorbitant fees from their patients. The Regulations include the Maximum Fees that can be charged from Patients for various services, the percentage of Patients who have to be treated on "free" basis to ensure that the Health Care Centre enjoys certain Government concessions, the Price at which medicines can be "sold" to Patients during their stay in the Health Care Centre, etc. Due to the above Regulations and the competitive environment, SSH is facing margin pressures and it is difficult to increase the patient numbers also. So, SSH's Management Consultant (Kapil) has come out with some plan for cost control and reduction. SSH provides treatment under a package system where Fees is charged irrespective of the days a patient stays in the Hospital. Kapil estimates 2.50 Patient Days per patient. He wants to reduce it to 2 days. By this, Kapil estimates that the general variable cost of 500 per patient day will get reduced. Annually 15,000 patients visit to the hospital for treatment SSH's Chief Medical Superintendent (Vasudha) has some concerns with that of Kapil's plan. According to her, reducing the patient stay would be detrimental to the full recovery of patient. They would come again for admission thereby increasing current re-admission rate from 3% to 5%, it means re-admitting 300 additional patients. SSH has to spend 25,00,000 more to accommodate this increase in re admission. Kapil says that this is still beneficial to SSH, since every re-admission is treated as new admission and it would result in additional cash flow of 4,500 per patient in the form of Admission Fees. Required: 1.Compute the impact of Kapil's plan on SSH's Incomes. 2. What other factors should be considered in the above case? 9.139 Pothuka's Students and took on Strategic Cont Management & Performance Evaluation CAP Concept Illustration: Pick out from the following terms, costs classified under Committed Fixed Costs' or Discretionary Fixed Conta". M11 Item Classification Committed Discretionary Committed 1. Annual increase of Salary and Wages of Administrative Staff by 5% as per agreement. 2. New Advertisement for existing products is recommended by the Marketing Department for achieving sales quantities that were budgeted for at the beginning of the year. 3. Rents paid for the Factory Premises for the past 6 months and the Rent Payable for the next six months. Production is going on in the factory. 4. Research Costs on a product that has reached Maturity' Phase in its Life Cycle, and the Research Costs which may be needed on introducing a cheaper substitute into the market for facing competition. 5. Legal Consultancy Fees payable for Patent Rights on a new product. Patenting rights have been applied for. RBD Cost on Product that has reached Maturity Phase is committed, while R&D Cost on its substitute is Discretionary Committed Concept Illustration: Classify the following Fixed Cost as normally being either Committed or Discretionary Item Depreciation on Assets Advertising Research Answer: Nature Committed Discretionary Discretionary RTP Employees Training Discretionary 10.2.6 Engineered Cost vs Discretionary Cost Particulars Engineered Costs Discretionary Costs (N 08) 1. Meaning These are costs that result specifically from a clear cause These costs are not tied to a clear cause and and effect relationship between inputs and outputs. effect relationship between inputs and outputs. 2. Nature The cause and effect relationship is usually directly and They usually arise from periodic decisions personally observable. regarding the maximum outlay to be incurred. Examples of inputs are Direct Material Costs, Direct Advertising, Public Relations, Executive Training 3. Examples Labour Costs, etc. Examples of output are the products, Costs, etc. e.g. cellphone, cars, etc. 10.2.7 Opportunity Cost 1. Meaning of Opportunity Cost: (a) It is the benefit foregone from an alternative not chosen. (b) It is the value of sacrifice made or benefit of opportunity foregone by selecting one alternative in preference to other alternatives. (C) It is the prospective change in cost following the adoption of an alternative machine, process, raw materials, specification or operation. (d) It is the cost of opportunity lost by diversion of an input factor from one use to another. (e) It is the Maximum Contribution that is foregone by using limited resources for a particular purpose. (0It represents the measurable value of opportunity bypassed by rejecting an alternative use of resources. 2. Principles with respect to Opportunity Cost: (a) Opportunity Cost is a Relevant Cost where alternatives are available. It involves choice and decision-making out of many alternatives. (b) Opportunity Cost is generally evaluated for short-term purposes. (c) Opportunity Cost is not useful for accounting, reporting and cost control. It does not find any place in formal accounts and is computed only for comparison purposes. (d) Opportunity Cost arises only in case of restriction of resources, i.e. Key Factor situation. If resources are abundantly available, they can be used for pursuing all available alternatives / courses of action. (e) When a number of alternatives are available, the highest of the Opportunity Costs is relevant for decision-making

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts