Answered step by step

Verified Expert Solution

Question

1 Approved Answer

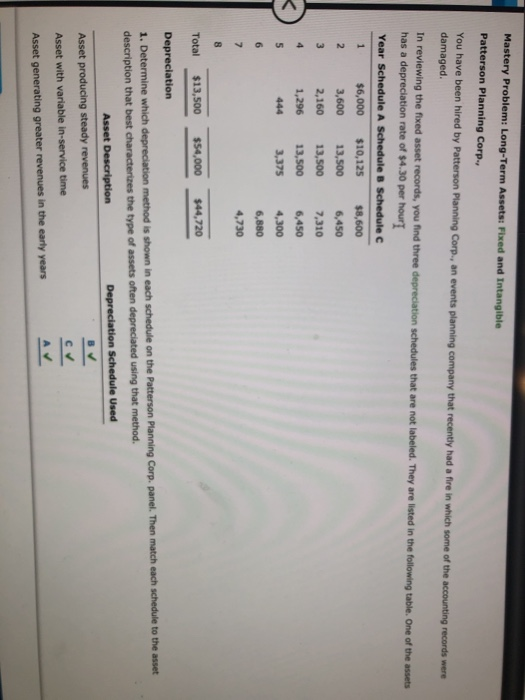

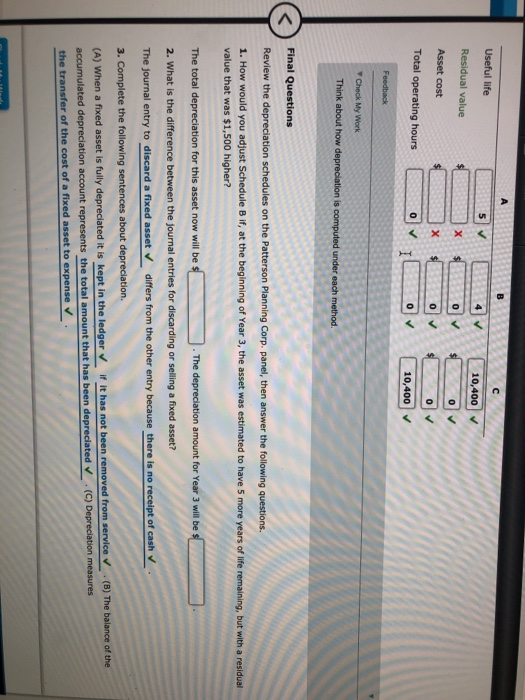

Mastery Problem: Long-Term Assets: Fixed and Intangible Patterson Planning Corp., You have been hired by Patterson Planning Corp., an events planning company that recently had

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Art Of Integrating Strategic Planning Process Metrics Risk Mitigation And Auditing

Authors: J.B. Smith

1st Edition

0873899253, 978-0873899253