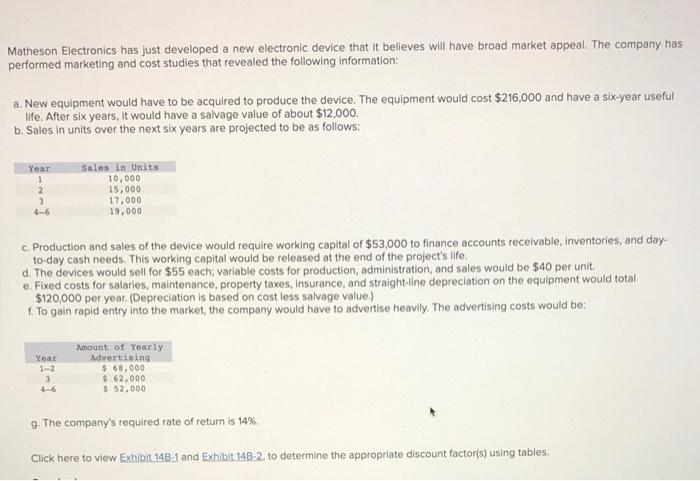

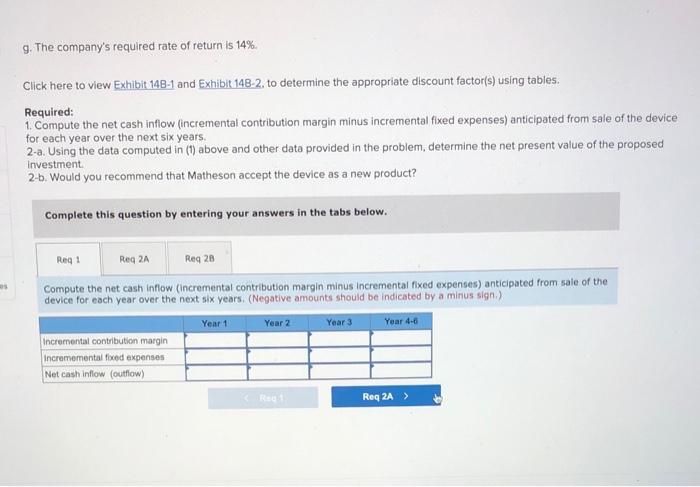

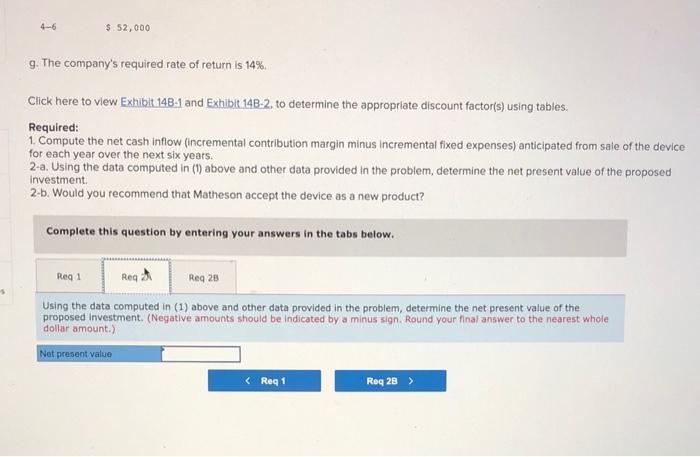

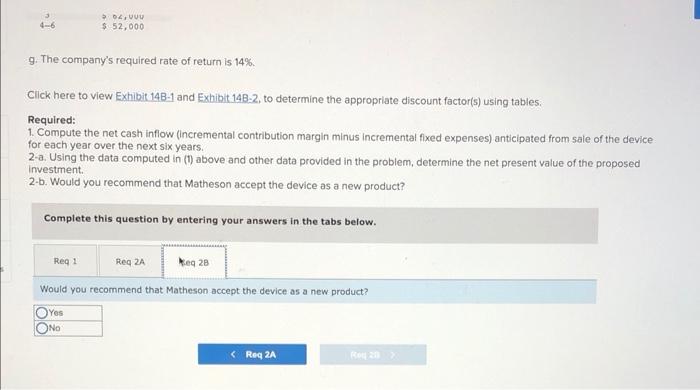

Matheson Electronics has just developed a new electronic device that it belleves will have broad market appeal. The company has performed marketing and cost studies that revealed the following information: a. New equipment would have to be acquired to produce the device. The equipment would cost $216,000 and have a six-year useful life. After six years, it would have a salvage value of about $12,000. b. Sales in units over the next six years are projected to be as follows: Year 1 2 3 4-6 Sales in Units 10,000 15,000 17,000 19.000 c. Production and sales of the device would require working capital of $53,000 to finance accounts receivable, inventories, and day- to-day cash needs. This working capital would be released at the end of the project's life. d. The devices would sell for $55 each, variable costs for production, administration, and sales would be $40 per unit e Fixed costs for salaries, maintenance, property taxes, insurance, and straight-line depreciation on the equipment would total $120,000 per year. (Depreciation is based on cost less salvage value.) 1. To gain rapid entry into the market, the company would have to advertise heavily. The advertising costs would be: Year 12 3 446 Amount of Yearly Advertising 5.68.000 $ 62,000 $ 52,000 g. The company's required rate of return is 14% Click here to view Exhibit 14B-1 and Exhibit 14B-2, to determine the appropriate discount factor(s) using tables. g. The company's required rate of return is 14% Click here to view Exhibit 148-1 and Exhibit 148-2. to determine the appropriate discount factor(s) using tables. Required: 1. Compute the net cash inflow (incremental contribution margin minus incremental fixed expenses) anticipated from sale of the device for each year over the next six years. 2-a. Using the data computed in (1) above and other data provided in the problem, determine the net present value of the proposed Investment 2-b. Would you recommend that Matheson accept the device as a new product? Complete this question by entering your answers in the tabs below. Reg 1 Reg 2A Reg 28 Compute the net cash inflow (incremental contribution margin minus incremental fixed expenses) anticipated from sale of the device for each year over the next six years. (Negative amounts should be indicated by a minus sign) Year 1 Year 2 Year 3 Your 4-6 Incremental contribution margin Incrememental food expenses Net cash inflow (outfiow) Reg 2A > 4-6 $ 52,000 g. The company's required rate of return is 14%. Click here to view Exhibit 148-1 and Exhibit 14B-2, to determine the appropriate discount factor(s) using tables. Required: 1. Compute the net cash inflow (incremental contribution margin minus incremental fixed expenses) anticipated from sale of the device for each year over the next six years. 2-a. Using the data computed in (1) above and other data provided in the problem, determine the net present value of the proposed Investment 2-b. Would you recommend that Matheson accept the device as a new product? Complete this question by entering your answers in the tabs below. Reg 1 Req Reg 20 Using the data computed in (1) above and other data provided in the problem, determine the net present value of the proposed Investment. (Negative amounts should be indicated by a minus sign. Round your final answer to the nearest whole dollar amount.) Net present value 4-6 >04,VUU $ 52,000 g. The company's required rate of return is 14% Click here to view Exhibit 148-1 and Exhibit 148:2, to determine the appropriate discount factor(s) using tables. Required: 1. Compute the net cash inflow (incremental contribution margin minus Incremental fixed expenses) anticipated from sale of the device for each year over the next six years. 2-a. Using the data computed in (1) above and other data provided in the problem, determine the net present value of the proposed Investment 2-b. Would you recommend that Matheson accept the device as a new product? Complete this question by entering your answers in the tabs below. Reg 1 Reg 2A Beg 28 Would you recommend that Matheson accept the device as a new product? Yes ONO