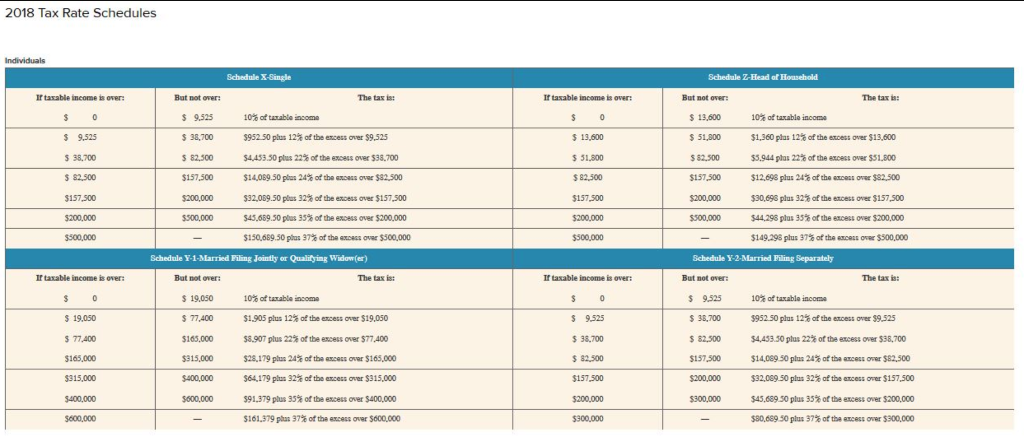

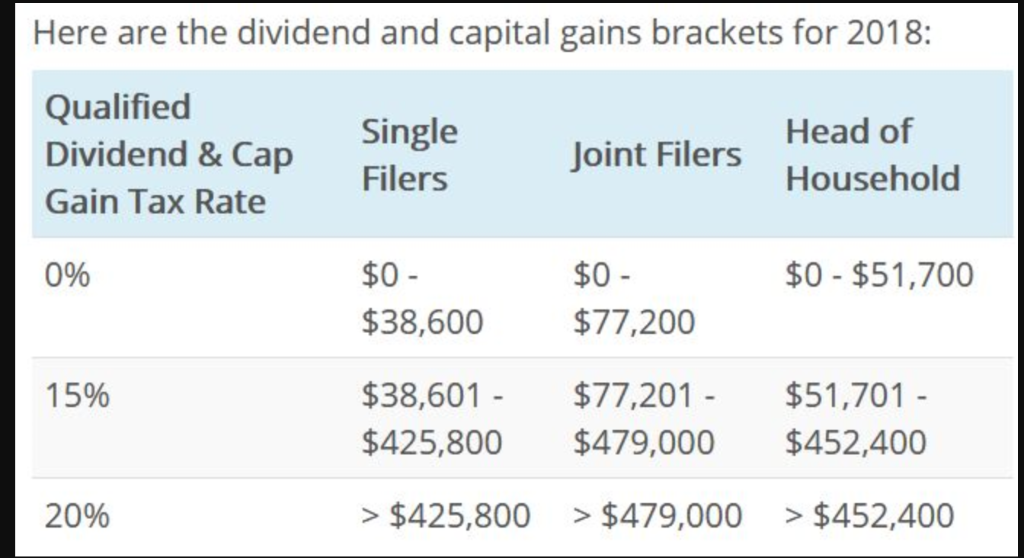

Question

Matt and Meg Comer are married and file a joint tax return. They do not have any children. Matt works as a history professor at

Matt and Meg Comer are married and file a joint tax return. They do not have any children. Matt works as a history professor at a local university and earns a salary of $63,750. Meg works part-time at the same university. She earns $31,050 a year. The couple does not itemize deductions. Other than salary, the Comers only other source of income is from the disposition of various capital assets (mostly stocks).

a. What is the Comers tax liability for 2018 if they report the following capital gains and losses for the year?

| Short-term capital gains | $ | 9,010 | |

| Short-term capital losses | (2,010) | ||

| Long-term capital gains | 15,010 | ||

| Long-term capital losses | (6,010) |

b. What is the Comers tax liability for 2018 if they report the following capital gains and losses for the year?

| Short-term capital gains | $ | 1,500 | |

| Short-term capital losses | 0 | ||

| Long-term capital gains | 13,020 | ||

| Long-term capital losses | (10,010 |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments Unlimited A Novel About DevOps Security Audit Compliance And Thriving In The Digital Age

Authors: Helen Beal, Bill Bensing, Jason Cox, Michael Edenzon, John Willis

1st Edition

1950508536, 978-1950508532