may an Expert help me with this please! I will rate for sure!!

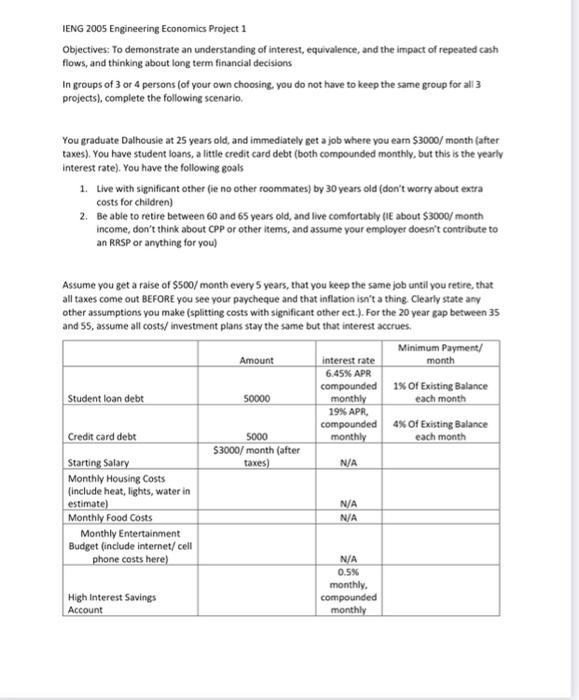

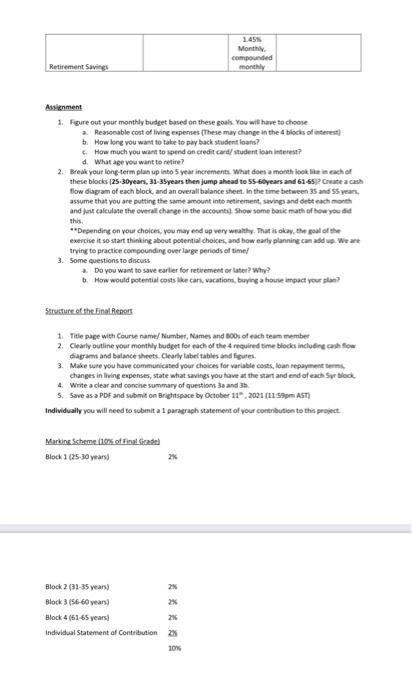

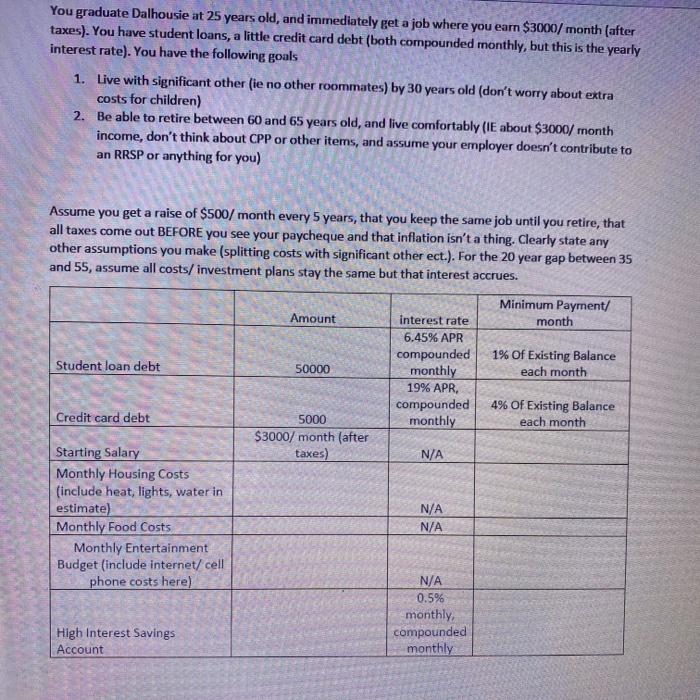

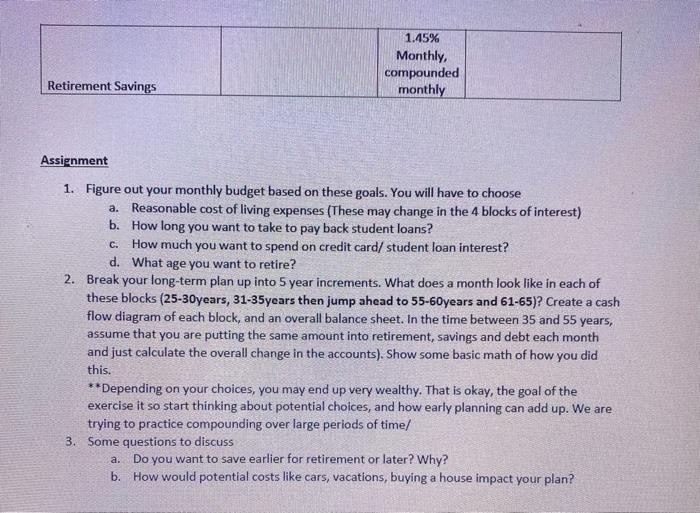

TENG 2005 Engineering Economics Project 1 Objectives: To demonstrate an understanding of interest, equivalence, and the impact of repeated cash flows, and thinking about long term financial decisions In groups of 3 or 4 persons (of your own choosing, you do not have to keep the same group for all 3 projects), complete the following scenario. You graduate Dalhousie at 25 years old, and immediately get a job where you earn $3000/month (after taxes). You have student loans, a little credit card debt (both compounded monthly, but this is the yearly interest rate). You have the following goals 1. Live with significant other (ie no other roommates) by 30 years old (don't worry about extra costs for children) 2. Be able to retire between 60 and 65 years old, and live comfortably (le about $3000/month income, don't think about CPP or other items, and assume your employer doesn't contribute to an RRSP or anything for you) Assume you get a raise of $500/month every 5 years, that you keep the same job until you retire, that all taxes come out BEFORE you see your paycheque and that inflation isn't a thing. Clearly state any other assumptions you make (splitting costs with significant other ect.). For the 20 year gap between 35 and 55, assume all costs/investment plans stay the same but that interest accrues. Minimum Payment/ Amount interest rate month 6.45% APR compounded 1% of Existing Balance Student loan debt 50000 monthly each month 19% APR compounded 4% of Existing Balance Credit card debt 5000 monthly each month $3000/ month (after Starting Salary taxes) N/A Monthly Housing Costs (include heat, lights, water in estimate) N/A Monthly Food Costs N/A Monthly Entertainment Budget (include internet/ cell phone costs here) N/A 0.5% monthly High Interest Savings compounded Account monthly 1.45 Monthly compounded monthly Retirement Savings Assignment 1. Figure out your monthly budget based on these goals. You will have to choose 2. Reasonable cost of living expenses (These may change in the blocks of interest b. How long you want to take to pay back student loans? How much you want to spend on credit card studention interest? d. What age you want to retire? 2. Break your long-term plan up into 5 year increments. What does a month look like in each of these blocks (25-30years, 31-35years then jump ahead to 55 years and 61-652Cate a cash flow diagram of each block, and an overall balance sheet. In the time between 35 and years assume that you are putting the same amount into retirement, savings and debe each month and or calculate the overall change in the account Show some basic math of how you **Depending on your choices, you may end up very wealthy. That is okay the goal of the exercise it so start thinking about potential choices, and how early planning can add up. We are trying to practice compounding over large periods of time 3. Some questions to discuss Do you want to save earlier for retirement or later? Why? 6. How would potential costs like cars, vacation, buying a house impact your plan? Structure of the Final Report 1. Title page with Course name/ Number, Names and soos of each team member 2. Clearly outline your monthly budget for each of the required time biodies including cash fow diagrams and balance sheets. Clearly label tables and figures. 3. Make sure you have communicated your choices for variable costs, loan repayment changes in living expenses, state what savings you have at the start and end of each Syed 4 Write a clear and contine summary of questions 30 and 35 S. Save as a PDF and submit on Brightspace by October 11, 2021 (AST) Individually you will need to to submit a paragraph statement of your contribution to this project Marking Schemes oldal Block 1 (25-30 years) Block 2 (31-35 years Block 3 (56-60 years) 2% Block 4 (61-65 years) 23 Individual Statement of Contribution 2% 30% You graduate Dalhousie at 25 years old, and immediately get a job where you earn $3000/month (after taxes). You have student loans, a little credit card debt (both compounded monthly, but this is the yearly interest rate). You have the following goals 1. Live with significant other (ie no other roommates) by 30 years old (don't worry about extra costs for children) 2. Be able to retire between 60 and 65 years old, and live comfortably (IE about $3000/month income, don't think about CPP or other items, and assume your employer doesn't contribute to an RRSP or anything for you) Assume you get a raise of $500/month every 5 years, that you keep the same job until you retire, that all taxes come out BEFORE you see your paycheque and that inflation isn't a thing. Clearly state any other assumptions you make (splitting costs with significant other ect.). For the 20 year gap between 35 and 55, assume all costs/investment plans stay the same but that interest accrues. Minimum Payment/ Amount interest rate month 6.45% APR compounded 1% Of Existing Balance Student loan debt 50000 monthly each month 19% APR compounded 4% Of Existing Balance Credit card debt 5000 monthly each month $3000/ month (after Starting Salary taxes) N/A Monthly Housing Costs (include heat, lights, water in estimate) N/A Monthly Food Costs N/A Monthly Entertainment Budget (include internet/ cell phone costs here) N/A 0.5% monthly, High Interest Savings compounded Account monthly 1.45% Monthly, compounded monthly Retirement Savings Assignment C. 1. Figure out your monthly budget based on these goals. You will have to choose a. Reasonable cost of living expenses (These may change in the 4 blocks of interest) b. How long you want to take to pay back student loans? How much you want to spend on credit card/ student loan interest? d. What age you want to retire? 2. Break your long-term plan up into 5 year increments. What does a month look like in each of these blocks (25-30years, 31-35years then jump ahead to 55-60years and 61-65)? Create a cash flow diagram of each block, and an overall balance sheet. In the time between 35 and 55 years, assume that you are putting the same amount into retirement, savings and debt each month and just calculate the overall change in the accounts). Show some basic math of how you did this. **Depending on your choices, you may end up very wealthy. That is okay, the goal of the exercise it so start thinking about potential choices, and how early planning can add up. We are trying to practice compounding over large periods of time/ 3. Some questions to discuss a. Do you want to save earlier for retirement or later? Why? b. How would potential costs like cars, vacations, buying a house impact your plan? TENG 2005 Engineering Economics Project 1 Objectives: To demonstrate an understanding of interest, equivalence, and the impact of repeated cash flows, and thinking about long term financial decisions In groups of 3 or 4 persons (of your own choosing, you do not have to keep the same group for all 3 projects), complete the following scenario. You graduate Dalhousie at 25 years old, and immediately get a job where you earn $3000/month (after taxes). You have student loans, a little credit card debt (both compounded monthly, but this is the yearly interest rate). You have the following goals 1. Live with significant other (ie no other roommates) by 30 years old (don't worry about extra costs for children) 2. Be able to retire between 60 and 65 years old, and live comfortably (le about $3000/month income, don't think about CPP or other items, and assume your employer doesn't contribute to an RRSP or anything for you) Assume you get a raise of $500/month every 5 years, that you keep the same job until you retire, that all taxes come out BEFORE you see your paycheque and that inflation isn't a thing. Clearly state any other assumptions you make (splitting costs with significant other ect.). For the 20 year gap between 35 and 55, assume all costs/investment plans stay the same but that interest accrues. Minimum Payment/ Amount interest rate month 6.45% APR compounded 1% of Existing Balance Student loan debt 50000 monthly each month 19% APR compounded 4% of Existing Balance Credit card debt 5000 monthly each month $3000/ month (after Starting Salary taxes) N/A Monthly Housing Costs (include heat, lights, water in estimate) N/A Monthly Food Costs N/A Monthly Entertainment Budget (include internet/ cell phone costs here) N/A 0.5% monthly High Interest Savings compounded Account monthly 1.45 Monthly compounded monthly Retirement Savings Assignment 1. Figure out your monthly budget based on these goals. You will have to choose 2. Reasonable cost of living expenses (These may change in the blocks of interest b. How long you want to take to pay back student loans? How much you want to spend on credit card studention interest? d. What age you want to retire? 2. Break your long-term plan up into 5 year increments. What does a month look like in each of these blocks (25-30years, 31-35years then jump ahead to 55 years and 61-652Cate a cash flow diagram of each block, and an overall balance sheet. In the time between 35 and years assume that you are putting the same amount into retirement, savings and debe each month and or calculate the overall change in the account Show some basic math of how you **Depending on your choices, you may end up very wealthy. That is okay the goal of the exercise it so start thinking about potential choices, and how early planning can add up. We are trying to practice compounding over large periods of time 3. Some questions to discuss Do you want to save earlier for retirement or later? Why? 6. How would potential costs like cars, vacation, buying a house impact your plan? Structure of the Final Report 1. Title page with Course name/ Number, Names and soos of each team member 2. Clearly outline your monthly budget for each of the required time biodies including cash fow diagrams and balance sheets. Clearly label tables and figures. 3. Make sure you have communicated your choices for variable costs, loan repayment changes in living expenses, state what savings you have at the start and end of each Syed 4 Write a clear and contine summary of questions 30 and 35 S. Save as a PDF and submit on Brightspace by October 11, 2021 (AST) Individually you will need to to submit a paragraph statement of your contribution to this project Marking Schemes oldal Block 1 (25-30 years) Block 2 (31-35 years Block 3 (56-60 years) 2% Block 4 (61-65 years) 23 Individual Statement of Contribution 2% 30% You graduate Dalhousie at 25 years old, and immediately get a job where you earn $3000/month (after taxes). You have student loans, a little credit card debt (both compounded monthly, but this is the yearly interest rate). You have the following goals 1. Live with significant other (ie no other roommates) by 30 years old (don't worry about extra costs for children) 2. Be able to retire between 60 and 65 years old, and live comfortably (IE about $3000/month income, don't think about CPP or other items, and assume your employer doesn't contribute to an RRSP or anything for you) Assume you get a raise of $500/month every 5 years, that you keep the same job until you retire, that all taxes come out BEFORE you see your paycheque and that inflation isn't a thing. Clearly state any other assumptions you make (splitting costs with significant other ect.). For the 20 year gap between 35 and 55, assume all costs/investment plans stay the same but that interest accrues. Minimum Payment/ Amount interest rate month 6.45% APR compounded 1% Of Existing Balance Student loan debt 50000 monthly each month 19% APR compounded 4% Of Existing Balance Credit card debt 5000 monthly each month $3000/ month (after Starting Salary taxes) N/A Monthly Housing Costs (include heat, lights, water in estimate) N/A Monthly Food Costs N/A Monthly Entertainment Budget (include internet/ cell phone costs here) N/A 0.5% monthly, High Interest Savings compounded Account monthly 1.45% Monthly, compounded monthly Retirement Savings Assignment C. 1. Figure out your monthly budget based on these goals. You will have to choose a. Reasonable cost of living expenses (These may change in the 4 blocks of interest) b. How long you want to take to pay back student loans? How much you want to spend on credit card/ student loan interest? d. What age you want to retire? 2. Break your long-term plan up into 5 year increments. What does a month look like in each of these blocks (25-30years, 31-35years then jump ahead to 55-60years and 61-65)? Create a cash flow diagram of each block, and an overall balance sheet. In the time between 35 and 55 years, assume that you are putting the same amount into retirement, savings and debt each month and just calculate the overall change in the accounts). Show some basic math of how you did this. **Depending on your choices, you may end up very wealthy. That is okay, the goal of the exercise it so start thinking about potential choices, and how early planning can add up. We are trying to practice compounding over large periods of time/ 3. Some questions to discuss a. Do you want to save earlier for retirement or later? Why? b. How would potential costs like cars, vacations, buying a house impact your plan