Answered step by step

Verified Expert Solution

Question

1 Approved Answer

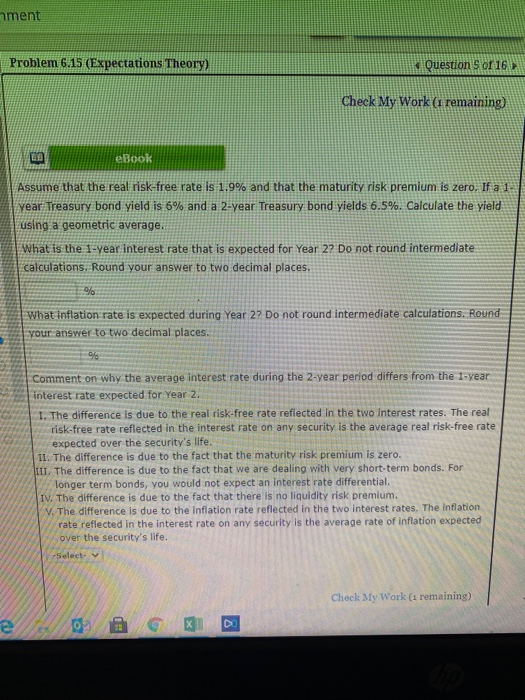

ment Problem 6.15 (Expectations Theory) nrnent Problem 6.15 (Expectations Theory) Qestion Sot 16 My rmai@ing) AC$utne that thxeal risk-free rate is 1.9% and that the

nrnent Problem 6.15 (Expectations Theory) Qestion Sot 16 My rmai@ing) AC$utne that thxeal risk-free rate is 1.9% and that the maturity iiSkpremium is zero. If 'J yepi;Treasrybond yield is anda 2year Treasury pond yields 4.5%. Calculate the yield using a geometric average. rate that iS expected for Year 2? Do intermediate Round your decimal places. Wh\t inflatiori is xpectd during Year 2? Do not round intermediate calculationS. ROUhd yourans"er to two decimal places. Comment 00 why the average interest rate during the 2+'ear period differe from the I-vear interest rate expected for Year 2. t. The difference is due to the real risk-free raie reflected in the two interest rates. The real fisk-free rate reflected in the interest rate on any security is the average real risk-free rate expected o.'er the security's life. 11. The difference is due the fact that the maturity risk premium is zero. The difference is due to the fact that we are dealing with very shortterm bonds. For longer term bonds, you would not expect an interest rate differential. IV, The difference is due to the fact that there is no liquidity risk premium. V. The difference is due to the inflation rate reflected in the interest rates _ The inflation rate reflected in the interest rate on any security is the average rate Of inflation over the securitws life. cheuk k remaining)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Financial Management

Authors: Stanley B. Block, Geoffrey A. Hirt, Bartley R. Danielsen

13th Edition

0073382388, 978-0073382388