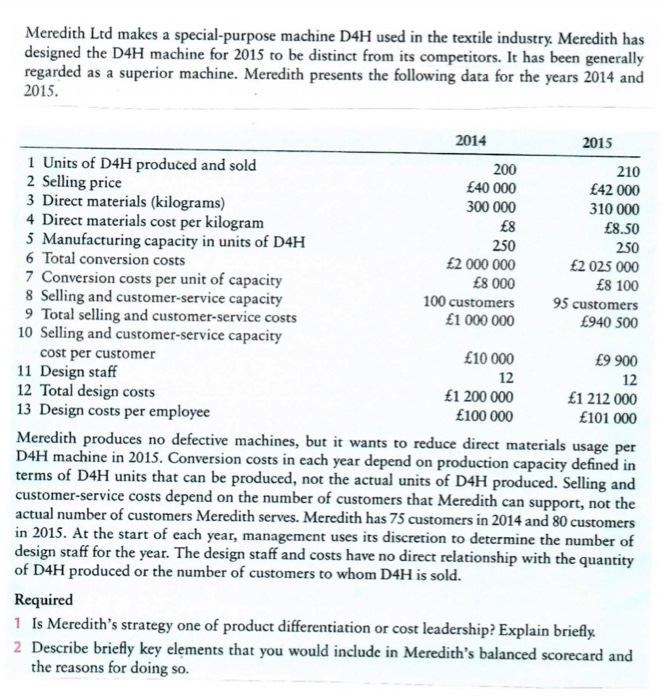

Meredith Ltd makes a special-purpose machine D4H used in the textile industry. Meredith has designed the D4H machine for 2015 to be distinct from its competitors. It has been generally regarded as a superior machine. Meredith presents the following data for the years 2014 and 2015. 12 2014 2015 1 Units of D4H produced and sold 200 210 2 Selling price 40 000 42 000 3 Direct materials (kilograms) 300 000 310 000 4 Direct materials cost per kilogram 8 8.50 5 Manufacturing capacity in units of D4H 250 250 6 Total conversion costs 2 000 000 2 025 000 7 Conversion costs per unit of capacity 8 000 8 100 8 Selling and customer-service capacity 100 customers 95 customers 9 Total selling and customer-service costs 1 000 000 940 500 10 Selling and customer-service capacity cost per customer 10 000 9 900 11 Design staff 12 12 Total design costs 1 200 000 1 212 000 13 Design costs per employee 100 000 101 000 Meredith produces no defective machines, but it wants to reduce direct materials usage per D4H machine in 2015. Conversion costs in each year depend on production capacity defined in terms of D4H units that can be produced, not the actual units of D4H produced. Selling and customer-service costs depend on the number of customers that Meredith can support, not the actual number of customers Meredith serves. Meredith has 75 customers in 2014 and 80 customers in 2015. At the start of each year, management uses its discretion to determine the number of design staff for the year. The design staff and costs have no direct relationship with the quantity of D4H produced or the number of customers to whom D4H is sold. Required 1 Is Meredith's strategy one of product differentiation or cost leadership? Explain briefly. 2 Describe briefly key elements that you would include in Meredith's balanced Scorecard and the reasons for doing so. Meredith Ltd makes a special-purpose machine D4H used in the textile industry. Meredith has designed the D4H machine for 2015 to be distinct from its competitors. It has been generally regarded as a superior machine. Meredith presents the following data for the years 2014 and 2015. 12 2014 2015 1 Units of D4H produced and sold 200 210 2 Selling price 40 000 42 000 3 Direct materials (kilograms) 300 000 310 000 4 Direct materials cost per kilogram 8 8.50 5 Manufacturing capacity in units of D4H 250 250 6 Total conversion costs 2 000 000 2 025 000 7 Conversion costs per unit of capacity 8 000 8 100 8 Selling and customer-service capacity 100 customers 95 customers 9 Total selling and customer-service costs 1 000 000 940 500 10 Selling and customer-service capacity cost per customer 10 000 9 900 11 Design staff 12 12 Total design costs 1 200 000 1 212 000 13 Design costs per employee 100 000 101 000 Meredith produces no defective machines, but it wants to reduce direct materials usage per D4H machine in 2015. Conversion costs in each year depend on production capacity defined in terms of D4H units that can be produced, not the actual units of D4H produced. Selling and customer-service costs depend on the number of customers that Meredith can support, not the actual number of customers Meredith serves. Meredith has 75 customers in 2014 and 80 customers in 2015. At the start of each year, management uses its discretion to determine the number of design staff for the year. The design staff and costs have no direct relationship with the quantity of D4H produced or the number of customers to whom D4H is sold. Required 1 Is Meredith's strategy one of product differentiation or cost leadership? Explain briefly. 2 Describe briefly key elements that you would include in Meredith's balanced Scorecard and the reasons for doing so