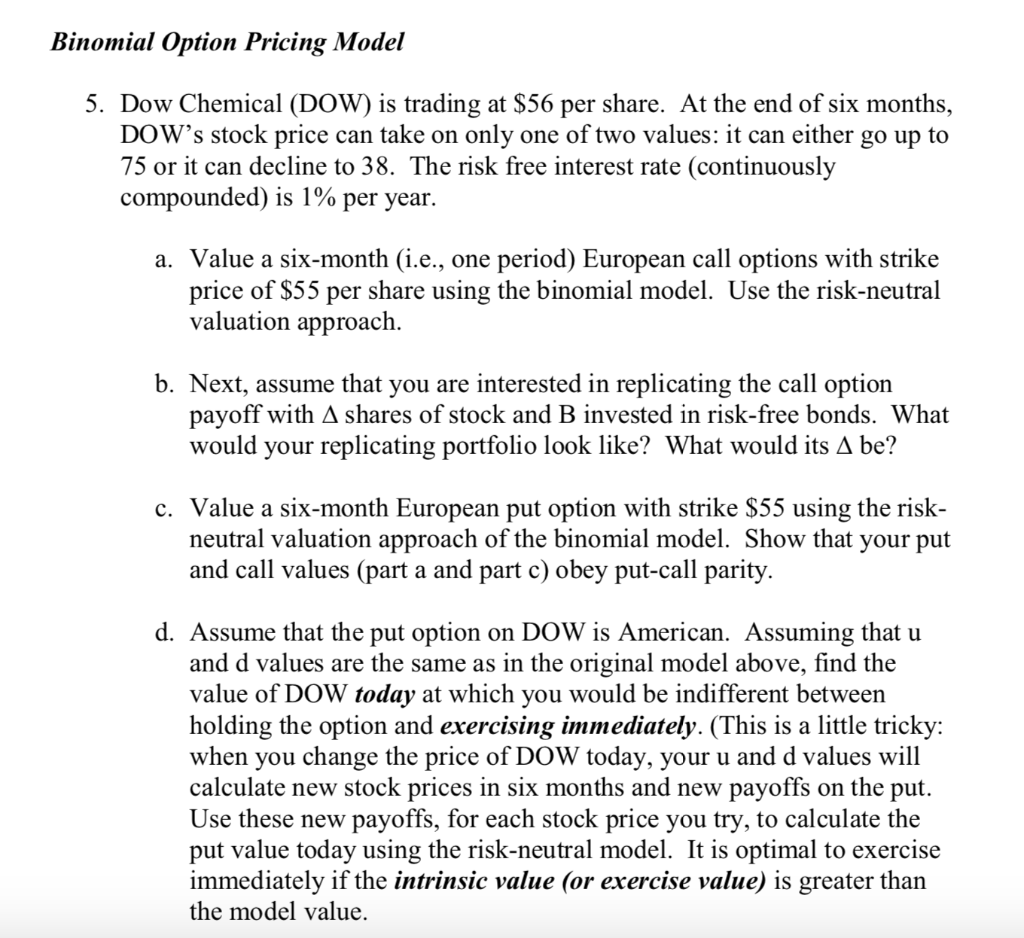

mial Option Pricing Model Dow Chemical (DOW) is trading at $56 per share. At the end of six months, DOW's stock price can take on only one of two values: it can either go up to 75 or it can decline to 38 . The risk free interest rate (continuously compounded) is 1% per year. a. Value a six-month (i.e., one period) European call options with strike price of $55 per share using the binomial model. Use the risk-neutral valuation approach. b. Next, assume that you are interested in replicating the call option payoff with shares of stock and B invested in risk-free bonds. What would your replicating portfolio look like? What would its be? c. Value a six-month European put option with strike $55 using the riskneutral valuation approach of the binomial model. Show that your put and call values (part a and part c) obey put-call parity. d. Assume that the put option on DOW is American. Assuming that u and d values are the same as in the original model above, find the value of DOW today at which you would be indifferent between holding the option and exercising immediately. (This is a little tricky: when you change the price of DOW today, your u and d values will calculate new stock prices in six months and new payoffs on the put. Use these new payoffs, for each stock price you try, to calculate the put value today using the risk-neutral model. It is optimal to exercise immediately if the intrinsic value (or exercise value) is greater than the model value. mial Option Pricing Model Dow Chemical (DOW) is trading at $56 per share. At the end of six months, DOW's stock price can take on only one of two values: it can either go up to 75 or it can decline to 38 . The risk free interest rate (continuously compounded) is 1% per year. a. Value a six-month (i.e., one period) European call options with strike price of $55 per share using the binomial model. Use the risk-neutral valuation approach. b. Next, assume that you are interested in replicating the call option payoff with shares of stock and B invested in risk-free bonds. What would your replicating portfolio look like? What would its be? c. Value a six-month European put option with strike $55 using the riskneutral valuation approach of the binomial model. Show that your put and call values (part a and part c) obey put-call parity. d. Assume that the put option on DOW is American. Assuming that u and d values are the same as in the original model above, find the value of DOW today at which you would be indifferent between holding the option and exercising immediately. (This is a little tricky: when you change the price of DOW today, your u and d values will calculate new stock prices in six months and new payoffs on the put. Use these new payoffs, for each stock price you try, to calculate the put value today using the risk-neutral model. It is optimal to exercise immediately if the intrinsic value (or exercise value) is greater than the model value