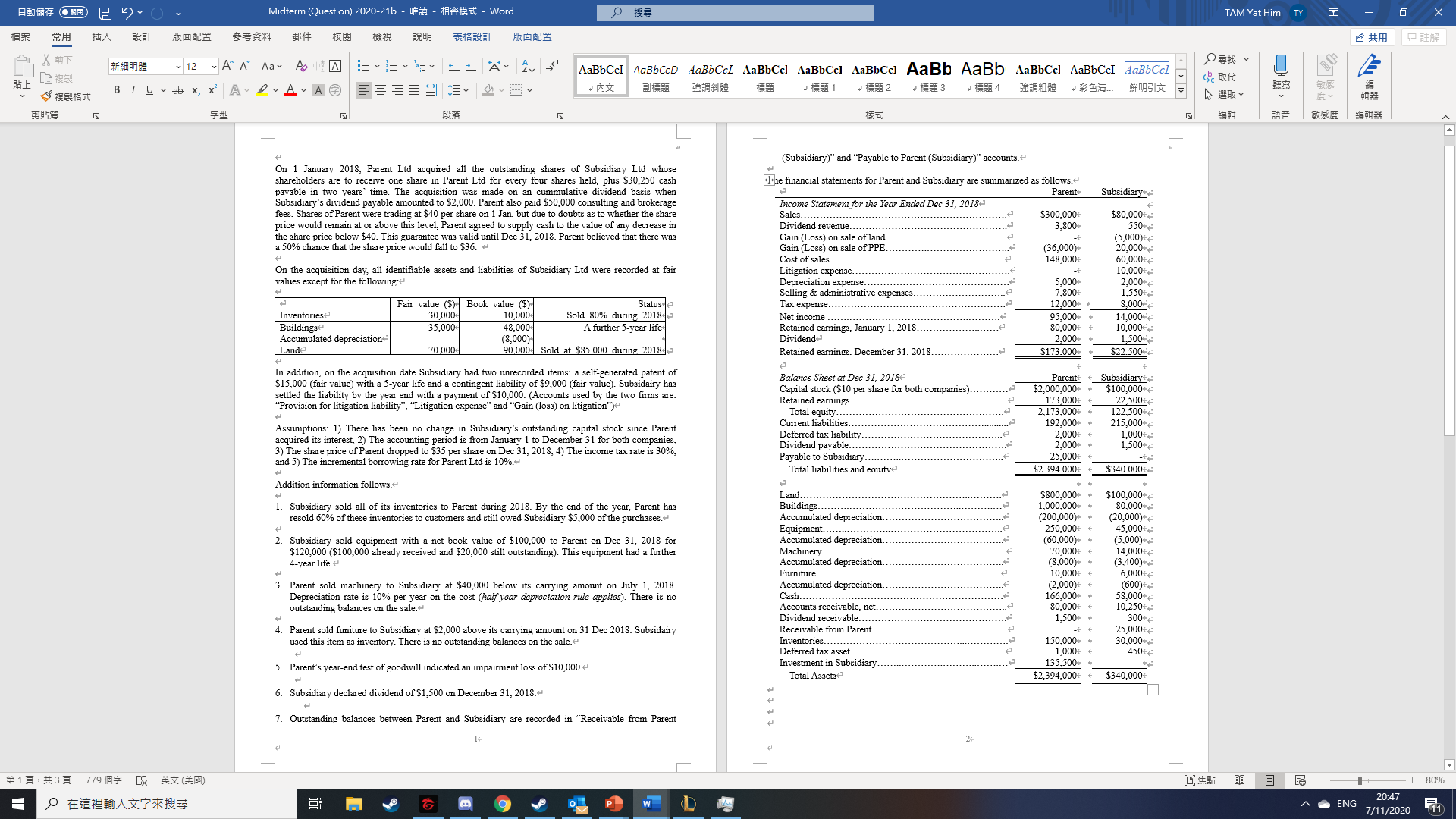

Midterm (Question) 2020-21b - MM - MEatest - Word TAM Yat Him TY X X AT 12 " A" A" Aa At A AaBbCcI AaBbCCD AaBbCc/ AaBbCc] AaBbCc] AaBbCc] AaBb AaBb AaBbCc] AaBbCcI AaBbCcI BIUab X x' ALAA 18 1 18 3 #RASIX (Subsidiary)" and "Payable to Parent (Subsidiary)" accounts. On 1 January 2018, Parent Ltd acquired all the outstanding shares of Subsidiary Ltd whose shareholders are to receive one share in Parent Lid for every four shares held, plus $30,250 cash The financial statements for Parent and Subsidiary are summarized as follows. payable in two years' time. The acquisition was made on an cummulative dividend basis when Parent- Subsidiarye Subsidiary's dividend payable amounted to $2,000. Parent also paid $30,000 consulting and brokerage fees. Shares of Parent were trading at $40 per share on 1 Jan, but due to doubts as to whether the share Income Statement for the Year Ended Dec 31, 2018- Sales......... -. .... $300,000 $80,000- price would remain at or above this level, Parent agreed to supply cash to the value of any decrease in ... 3,800 550 the share price below $40. This guarantee was valid until Dec 31, 2018. Parent believed that there was Dividend revenue............... Gain (Loss) on sale of land.. ... a 50% chance that the share price would fall to $36. ~ Gain (Loss) on sale of PPE... (36,000)- (5,000)- 20,000- On the acquisition day, all identifiable assets and liabilities of Subsidiary Ltd were recorded at fair Cost of sales.... 148,000- 60,0003 5,0004 10,000- values except for the following:+ Litigation expense.... Depreciation expense.. ....+ 2,000 Selling & administrative ex 7,800 1,550 Fair value ($) Book value ($) Status Tax expense... 12,000- 8,000 Inventories 30,000 10,000 Sold 80% during 20184 -...... 95,000- 14,000- Buildings $5,000 18,000 A further 5-year life Net income ............" Retained earnings, January 1, 2018... 80,000- 0,000- Accumulated depreciation 8,000) Dividend 2,000 1,500 Land 70.000 90.000 Sold at $83.000 during 2018 Retained earnings. December 31. 2018... . . ...... $173.000 $22.500 In addition, on the acquisition date Subsidiary had two unrecorded items: a self-generated patent of $15,000 (fair value) with a 5-year life and a contingent liability of $9,000 (fair value). Subsidairy has Balance Sheet at Dec 31, 2018- Parents * Subsidiary settled the liability by the year end with a payment of $10,000. (Accounts used by the two firms are: Capital stock ($10 per share for both companies)... $2,000,000- $100,000- "Provision for litigation liability", "Litigation expense" and "Gain (loss) on litigation") Retained earnings.......... -....... 173,000 22,500 Total equity........ .... 2,173,000- 122,500- Assumptions: 1) There has been no change in Subsidiary's outstanding capital stock since Parent Current liabilities.... 192,000- 215,000 acquired its interest, 2) The accounting period is from January 1 to December 31 for both companies, Deferred tax liability........ 2,000- 1,00043 3) The share price of Parent dropped to $35 per share on Dec 31, 2018, 4) The income tax rate is 30%, Dividend payable.... ..... 2,000- 1,500 and 5) The incremental borrowing rate for Parent Ltd is 10%.+ Payable to Subsidiary........... 25,000 Total liabilities and equitye $2.394.000 $340.000 Addition information follows. Land.......................".". $800,000- $100,000 1. Subsidiary sold all of its inventories to Parent during 2018. By the end of the year, Parent has Buildings... 1,000,000 80,000* resold 60% of these inventories to customers and still owed Subsidiary $5,000 of the purchases.~ Accumulated depreciation. 200,000) 20,000) 250,000 45,000- 2 Equipment..... Subsidiary sold equipment with a net book value of $100,000 to Parent on Dec 31, 2018 for Accumulated depreciation.. 60,000) $120,000 ($100,000 already received and $20,000 still outstanding). This equipment had a further 70.0004 (5,000) Machinery...... 14,000 4-year life.~ Accumulated depreciation. . 8,000) 3,400)- 3. Furniture... 10,000 6,000- Parent sold machinery to Subsidiary at $40,000 below its carrying amount on July 1, 2018. Accumulated depreciation.... (2,000)- (600) Depreciation rate is 10% per year on the cost (half-year depreciation rule applies). There is no Cash... 166,000- 58,000 outstanding balances on the sale.~ Accounts receivable, net... 80.000- 10,250-+3 Dividend receivable.. 1,500 300- 4. Parent sold funiture to Subsidiary at $2,000 above its carrying amount on 31 Dec 2018. Subsidairy Receivable from Parent.. 150,000- 25,000 used this item as inventory. There is no outstanding balances on the sale.~ Inventories................. 30,000*+ Deferred tax asset..................... 1,000- 5. Parent's year-end test of goodwill indicated an impairment loss of $10,000.~ Investment in Subsidiary. .... 135,500- Total Assets $2,394,000- $340,000+ 6. Subsidiary declared dividend of $1,500 on December 31, 2018.~ t t 7. Outstanding balances between Parent and Subsidiary are recorded in "Receivable from Parent #1R . #3A 779 85 XX XX(2) 81 8 - - + 80% 9 P W D ENG 20:47 7/11/2020