Answered step by step

Verified Expert Solution

Question

1 Approved Answer

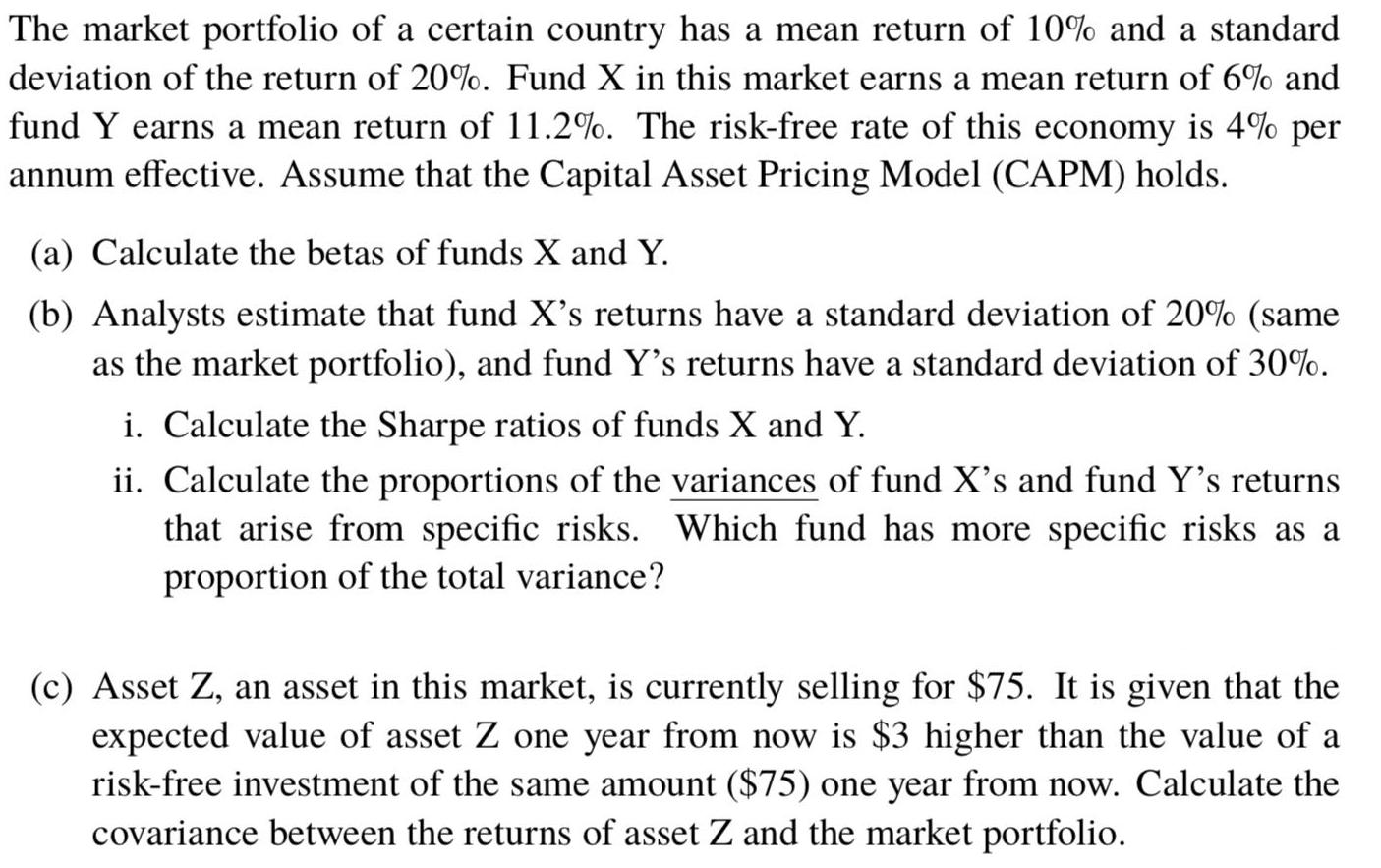

The market portfolio of a certain country has a mean return of 10% and a standard deviation of the return of 20%. Fund X

The market portfolio of a certain country has a mean return of 10% and a standard deviation of the return of 20%. Fund X in this market earns a mean return of 6% and fund Y earns a mean return of 11.2%. The risk-free rate of this economy is 4% per annum effective. Assume that the Capital Asset Pricing Model (CAPM) holds. (a) Calculate the betas of funds X and Y. (b) Analysts estimate that fund X's returns have a standard deviation of 20% (same as the market portfolio), and fund Y's returns have a standard deviation of 30%. i. Calculate the Sharpe ratios of funds X and Y. ii. Calculate the proportions of the variances of fund X's and fund Y's returns that arise from specific risks. Which fund has more specific risks as a proportion of the total variance? (c) Asset Z, an asset in this market, is currently selling for $75. It is given that the expected value of asset Z one year from now is $3 higher than the value of a risk-free investment of the same amount ($75) one year from now. Calculate the covariance between the returns of asset Z and the market portfolio.

Step by Step Solution

★★★★★

3.40 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

Solution Market portfolio Fund X Fund Y Fund X Mean SD Fund Y ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Horngrens Accounting

Authors: Tracie L. Miller nobles, Brenda L. Mattison, Ella Mae Matsumura

12th edition

9780134487151, 013448715X, 978-0134674681