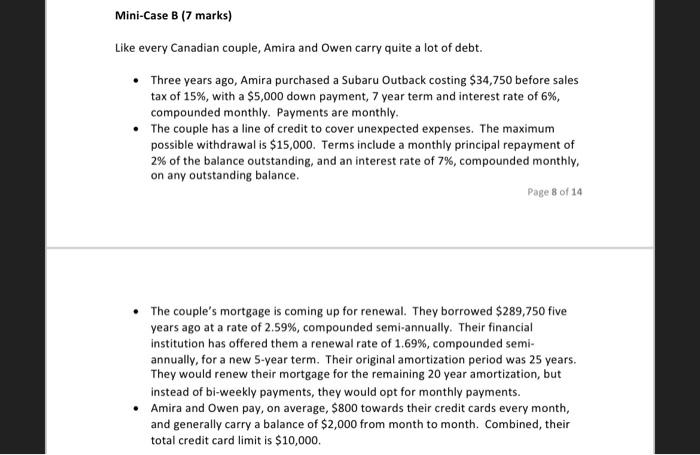

Mini-Case B (7 marks) Like every Canadian couple, Amira and Owen carry quite a lot of debt. Three years ago, Amira purchased a Subaru Outback costing $34,750 before sales tax of 15%, with a $5,000 down payment, 7 year term and interest rate of 6%, compounded monthly. Payments are monthly. The couple has a line of credit to cover unexpected expenses. The maximum possible withdrawal is $15,000. Terms include a monthly principal repayment of 2% of the balance outstanding, and an interest rate of 7%, compounded monthly on any outstanding balance. Page 8 of 14 The couple's mortgage is coming up for renewal. They borrowed $289,750 five years ago at a rate of 2.59%, compounded semi-annually. Their financial institution has offered them a renewal rate of 1.69%, compounded semi- annually, for a new 5-year term. Their original amortization period was 25 years. They would renew their mortgage for the remaining 20 year amortization, but instead of bi-weekly payments, they would opt for monthly payments. Amira and Owen pay, on average, $800 towards their credit cards every month, and generally carry a balance of $2,000 from month to month. Combined, their total credit card limit is $10,000 Part 6 (1 mark) Given all you know about the couple's finances (refer to both Case 1 and Case 2), what one suggestion would you make to provide guidance or improve their financial situation? Recommendations could include Mini-Case B (7 marks) Like every Canadian couple, Amira and Owen carry quite a lot of debt. Three years ago, Amira purchased a Subaru Outback costing $34,750 before sales tax of 15%, with a $5,000 down payment, 7 year term and interest rate of 6%, compounded monthly. Payments are monthly. The couple has a line of credit to cover unexpected expenses. The maximum possible withdrawal is $15,000. Terms include a monthly principal repayment of 2% of the balance outstanding, and an interest rate of 7%, compounded monthly on any outstanding balance. Page 8 of 14 The couple's mortgage is coming up for renewal. They borrowed $289,750 five years ago at a rate of 2.59%, compounded semi-annually. Their financial institution has offered them a renewal rate of 1.69%, compounded semi- annually, for a new 5-year term. Their original amortization period was 25 years. They would renew their mortgage for the remaining 20 year amortization, but instead of bi-weekly payments, they would opt for monthly payments. Amira and Owen pay, on average, $800 towards their credit cards every month, and generally carry a balance of $2,000 from month to month. Combined, their total credit card limit is $10,000 Part 6 (1 mark) Given all you know about the couple's finances (refer to both Case 1 and Case 2), what one suggestion would you make to provide guidance or improve their financial situation? Recommendations could include