Answered step by step

Verified Expert Solution

Question

1 Approved Answer

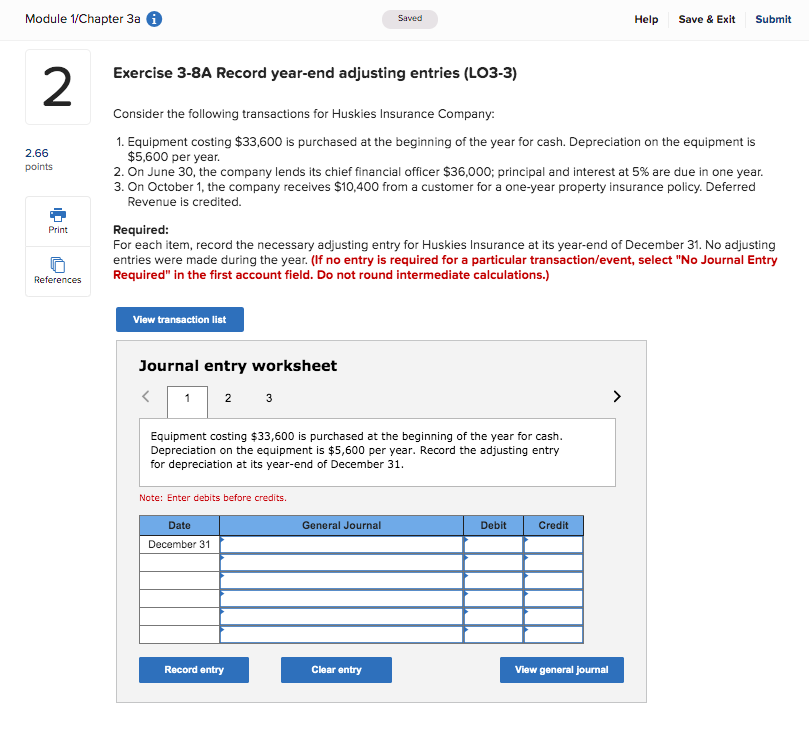

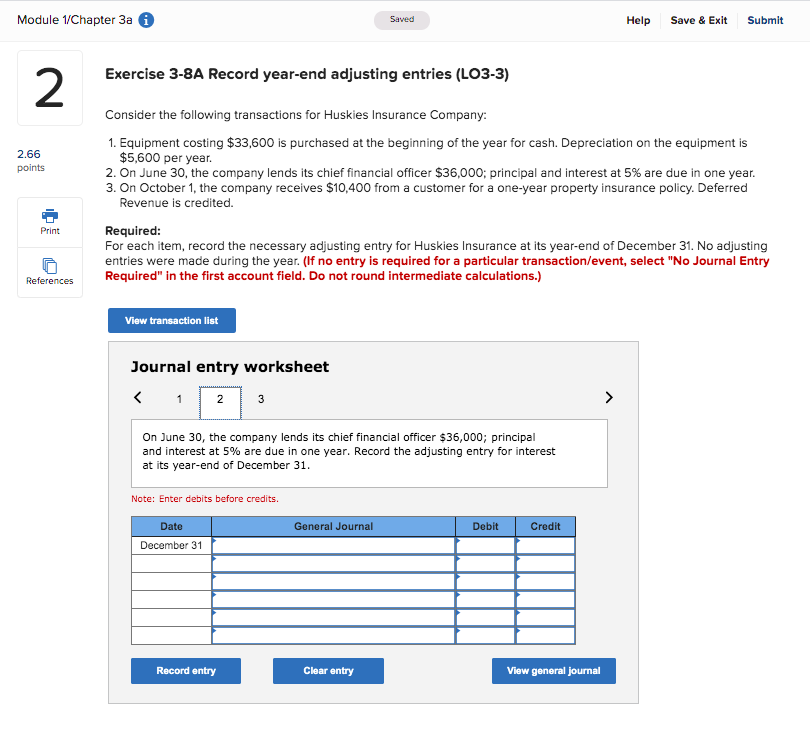

Module 1/Chapter 3a 2 2.66 points Print References Saved Exercise 3-8A Record year-end adjusting entries (LO3-3) Consider the following transactions for Huskies Insurance Company:

Module 1/Chapter 3a 2 2.66 points Print References Saved Exercise 3-8A Record year-end adjusting entries (LO3-3) Consider the following transactions for Huskies Insurance Company: Help Save & Exit Submit 1. Equipment costing $33,600 is purchased at the beginning of the year for cash. Depreciation on the equipment is $5,600 per year. 2. On June 30, the company lends its chief financial officer $36,000; principal and interest at 5% are due in one year. 3. On October 1, the company receives $10,400 from a customer for a one-year property insurance policy. Deferred Revenue is credited. Required: For each item, record the necessary adjusting entry for Huskies Insurance at its year-end of December 31. No adjusting entries were made during the year. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) View transaction list Journal entry worksheet < 1 2 3 Equipment costing $33,600 is purchased at the beginning of the year for cash. Depreciation on the equipment is $5,600 per year. Record the adjusting entry for depreciation at its year-end of December 31. Note: Enter debits before credits. Date December 31 General Journal Debit Credit Record entry Clear entry View general journal

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting An Introduction to Concepts Methods and Uses

Authors: Michael W. Maher, Clyde P. Stickney, Roman L. Weil

11th edition

1111571260, 978-1111571269