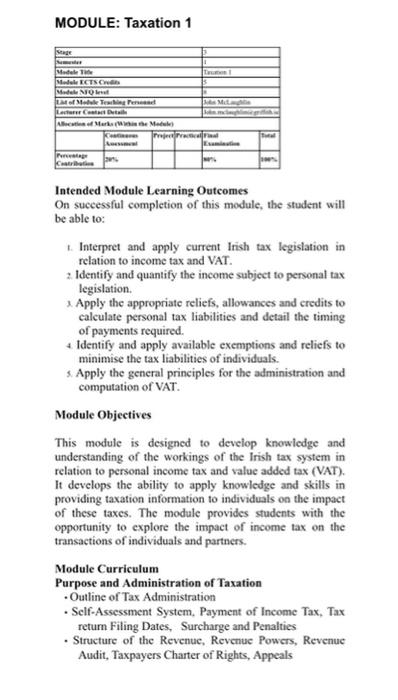

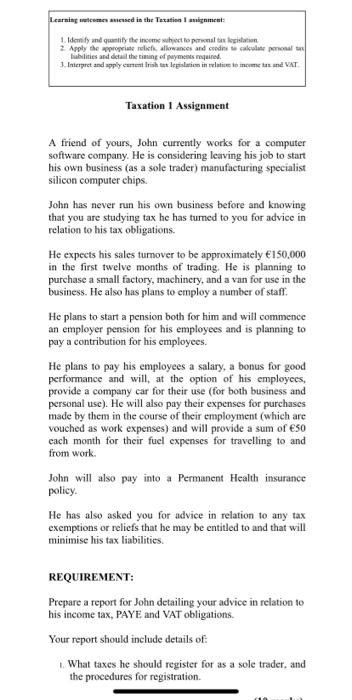

MODULE: Taxation 1 | Metal The Modele ECTS Model NTO of Me Tester Lesen Contact Ace Marke Model M Intended Module Learning Outcomes On successful completion of this module, the student will be able to: Interpret and apply current Irish tax legislation in relation to income tax and VAT. 2. Identify and quantify the income subject to personal tax legislation Apply the appropriate reliefs, allowances and credits to calculate personal tax liabilities and detail the timing of payments required. Identify and apply available exemptions and reliefs to minimise the tax liabilities of individuals. Apply the general principles for the administration and computation of VAT. Module Objectives This module is designed to develop knowledge and understanding of the workings of the Irish tax system in relation to personal income tax and value added tax (VAT). It develops the ability to apply knowledge and skills in providing taxation information to individuals on the impact of these taxes. The module provides students with the opportunity to explore the impact of income tax on the transactions of individuals and partners. Module Curriculum Purpose and Administration of Taxation Outline of Tax Administration Self-Assessment System. Payment of Income Tax, Tax return Filing Dates, Surcharge and Penalties Structure of the Revenue, Revenue Powers, Revenue Audit, Taxpayers Charter of Rights, Appeals . . Outline of Income Tax Charge to Income tax, residence and domicile Classification of Income, basis of assessment Tax credits, reliefs, charges on income Exemptions and relief schemes Retirement annuity contracts Tax treatment of single, married civil partners, widowed, separated and divorced persons Trade and Professional Income Badges of Trade Determination of income assessable Capital and revenue expenditure Computation of assessable profit Rules of commencement and cessation including possible revisions Short lived businesses . Change of accounting date Partnership, assessment of partners . Capital Allowances, wear and tear, balancing allowances and charges, replacement option Taxation of farmers, income averaging Subcontractors - relevant tax legislation, operation of Relevant Contracts Tax (RCT) Property and Investment Income Taxation of Investment Income, Case III, Case IV. and Schedule F Basis of assessment Dividend withholding tax Case V income - Basis of assessment, Allowable deductions, Premiums on Leases Case V capital allowances Rent a room relief Employment income Scope of Schedule E Employed vs Self-employed - Basis of assessment Qualifying expenses, Benefits in kind, Share option schemes Termination payments, exemptions and reliefs - PAYE system PRSI, USC Income Tax Losses Relief for Trade Losses, current year claims and losses carried forward Excess Capital Allowances Losses in commencement Terminal Losses Case V losses - Excess Case V capital allowances Value Added Tax . General principles including registration requirements (including group registration), records to be maintained Charge to VAT, Rates of VAT, Chargeable Amount Exempt and Zero Rated Supplies - Allowable and Disallowable Deductions Two-thirds and package rules - Cash and invoice basis EU intra community trade Imports and exports VAT on property - supply of immovable property for VAT purposes Local Property Tax Scope of Local Property Tax (LPT) - Liability, computations, payment options, exemptions Reading lists and other learning materials Taxation Manual, Griffith College Publications, Current Edition Recommended Reading List Website: www.revenue.ic Module Learning Environment This module is delivered by means of formal and participative style lectures as well as small group tutorials. The college intranet (Moodle) is used to provide supporting material including videos of lecture content Module Teaching and Learning Strategy This module is delivered through lectures and tutorials. Lectures are used to impart knowledge and understanding and also allow students to carry out problem solving exercises allowing the student to apply the techniques leamed. These are used to give students immediate feedback in this way learning can be monitored in the classroom. Formative assessment is also provided on a regular basis to help identify the student's progress and areas that may need improvement. Module Assessment Strategy 20% of the marks are allocated to coursework assignment. Students are required to provide taxation advice to a client and to reflect on taxation developments. Students are advised to undertake the assignment both in terms of research and the presentation format involved. The remaining 80% is reserved for an end of semester examination upon module completion. Learning women ained in the Texation langement 1.Idemy and quantify the income suject to penalti og 2. Apply the propriate relict, allowances and credinicakolate pa fibilities and detail the timing of payments required. 3. Interpret and apply contribution in relate to come and VAT Taxation 1 Assignment A friend of yours, John currently works for a computer software company. He is considering leaving his job to start his own business (as a sole trader) manufacturing specialist silicon computer chips John has never run his own business before and knowing that you are studying tax he has turned to you for advice in relation to his tax obligations. He expects his sales tumover to be approximately 150.000 in the first twelve months of trading. He is planning to purchase a small factory, machinery, and a van for use in the business. He also has plans to employ a number of staff. He plans to start a pension both for him and will commence an employer pension for his employees and is planning to pay a contribution for his employees. He plans to pay his employees a salary, a bonus for good performance and will at the option of his employees, provide a company car for their use (for both business and personal use). He will also pay their expenses for purchases made by them in the course of their employment (which are vouched as work expenses) and will provide a sum of 50 each month for their fuel expenses for travelling to and from work John will also pay into a Permanent Health insurance policy. He has also asked you for advice in relation to any tax exemptions or reliefs that he may be entitled to and that will minimise his tax liabilities. REQUIREMENT: Prepare a report for John detailing your advice in relation to his income tax, PAYE and VAT obligations Your report should include details of: What taxes he should register for as a sole trader, and the procedures for registration. Taxation 1 Assignment A friend of yours, John currently works for a computer software company. He is considering leaving his job to start his own business (as a sole trader) manufacturing specialist silicon computer chips John has never run his own business before and knowing that you are studying tax he has turned to you for advice in relation to his tax obligations He expects his sales turnover to be approximately 150,000 in the first twelve months of trading. He is planning to purchase a small factory, machinery, and a van for use in the business. He also has plans to employ a number of staff. He plans to start a pension both for him and will commence an employer pension for his employees and is planning to pay a contribution for his employees. He plans to pay his employees a salary, a bonus for good performance and will, at the option of his employees, provide a company car for their use (for both business and personal use). He will also pay their expenses for purchases made by them in the course of their employment (which are vouched as work expenses) and will provide a sum of 50 cach month for their fuel expenses for travelling to and from work. John will also pay into a Permanent Health insurance policy. He has also asked you for advice in relation to any tax exemptions or reliefs that he may be entitled to and that will minimise his tax liabilities. REQUIREMENT: Prepare a report for John detailing your advice in relation to his income tax, PAYE and VAT obligations Your report should include details of What taxes he should register for as a sole trader, and the procedures for registration (10 marks) 2 Basis of assessment for the income from his sole trade. (10 marks) 2. Allowable and disallowed expenses for his sole trade. (10 marks) 3. Allowable and disallowed expenses for his sole trade. (15 marks) 4. Tax relief for capital expenditure. (15 marks) 5. Tax obligations as an employer. (15 marks) 6. The treatment of his employees' remuneration and recommendations for minimising the tax liabilities of his employees. (15 marks) 7. Recommendations for minimising his overall tax liability MODULE: Taxation 1 | Metal The Modele ECTS Model NTO of Me Tester Lesen Contact Ace Marke Model M Intended Module Learning Outcomes On successful completion of this module, the student will be able to: Interpret and apply current Irish tax legislation in relation to income tax and VAT. 2. Identify and quantify the income subject to personal tax legislation Apply the appropriate reliefs, allowances and credits to calculate personal tax liabilities and detail the timing of payments required. Identify and apply available exemptions and reliefs to minimise the tax liabilities of individuals. Apply the general principles for the administration and computation of VAT. Module Objectives This module is designed to develop knowledge and understanding of the workings of the Irish tax system in relation to personal income tax and value added tax (VAT). It develops the ability to apply knowledge and skills in providing taxation information to individuals on the impact of these taxes. The module provides students with the opportunity to explore the impact of income tax on the transactions of individuals and partners. Module Curriculum Purpose and Administration of Taxation Outline of Tax Administration Self-Assessment System. Payment of Income Tax, Tax return Filing Dates, Surcharge and Penalties Structure of the Revenue, Revenue Powers, Revenue Audit, Taxpayers Charter of Rights, Appeals . . Outline of Income Tax Charge to Income tax, residence and domicile Classification of Income, basis of assessment Tax credits, reliefs, charges on income Exemptions and relief schemes Retirement annuity contracts Tax treatment of single, married civil partners, widowed, separated and divorced persons Trade and Professional Income Badges of Trade Determination of income assessable Capital and revenue expenditure Computation of assessable profit Rules of commencement and cessation including possible revisions Short lived businesses . Change of accounting date Partnership, assessment of partners . Capital Allowances, wear and tear, balancing allowances and charges, replacement option Taxation of farmers, income averaging Subcontractors - relevant tax legislation, operation of Relevant Contracts Tax (RCT) Property and Investment Income Taxation of Investment Income, Case III, Case IV. and Schedule F Basis of assessment Dividend withholding tax Case V income - Basis of assessment, Allowable deductions, Premiums on Leases Case V capital allowances Rent a room relief Employment income Scope of Schedule E Employed vs Self-employed - Basis of assessment Qualifying expenses, Benefits in kind, Share option schemes Termination payments, exemptions and reliefs - PAYE system PRSI, USC Income Tax Losses Relief for Trade Losses, current year claims and losses carried forward Excess Capital Allowances Losses in commencement Terminal Losses Case V losses - Excess Case V capital allowances Value Added Tax . General principles including registration requirements (including group registration), records to be maintained Charge to VAT, Rates of VAT, Chargeable Amount Exempt and Zero Rated Supplies - Allowable and Disallowable Deductions Two-thirds and package rules - Cash and invoice basis EU intra community trade Imports and exports VAT on property - supply of immovable property for VAT purposes Local Property Tax Scope of Local Property Tax (LPT) - Liability, computations, payment options, exemptions Reading lists and other learning materials Taxation Manual, Griffith College Publications, Current Edition Recommended Reading List Website: www.revenue.ic Module Learning Environment This module is delivered by means of formal and participative style lectures as well as small group tutorials. The college intranet (Moodle) is used to provide supporting material including videos of lecture content Module Teaching and Learning Strategy This module is delivered through lectures and tutorials. Lectures are used to impart knowledge and understanding and also allow students to carry out problem solving exercises allowing the student to apply the techniques leamed. These are used to give students immediate feedback in this way learning can be monitored in the classroom. Formative assessment is also provided on a regular basis to help identify the student's progress and areas that may need improvement. Module Assessment Strategy 20% of the marks are allocated to coursework assignment. Students are required to provide taxation advice to a client and to reflect on taxation developments. Students are advised to undertake the assignment both in terms of research and the presentation format involved. The remaining 80% is reserved for an end of semester examination upon module completion. Learning women ained in the Texation langement 1.Idemy and quantify the income suject to penalti og 2. Apply the propriate relict, allowances and credinicakolate pa fibilities and detail the timing of payments required. 3. Interpret and apply contribution in relate to come and VAT Taxation 1 Assignment A friend of yours, John currently works for a computer software company. He is considering leaving his job to start his own business (as a sole trader) manufacturing specialist silicon computer chips John has never run his own business before and knowing that you are studying tax he has turned to you for advice in relation to his tax obligations. He expects his sales tumover to be approximately 150.000 in the first twelve months of trading. He is planning to purchase a small factory, machinery, and a van for use in the business. He also has plans to employ a number of staff. He plans to start a pension both for him and will commence an employer pension for his employees and is planning to pay a contribution for his employees. He plans to pay his employees a salary, a bonus for good performance and will at the option of his employees, provide a company car for their use (for both business and personal use). He will also pay their expenses for purchases made by them in the course of their employment (which are vouched as work expenses) and will provide a sum of 50 each month for their fuel expenses for travelling to and from work John will also pay into a Permanent Health insurance policy. He has also asked you for advice in relation to any tax exemptions or reliefs that he may be entitled to and that will minimise his tax liabilities. REQUIREMENT: Prepare a report for John detailing your advice in relation to his income tax, PAYE and VAT obligations Your report should include details of: What taxes he should register for as a sole trader, and the procedures for registration. Taxation 1 Assignment A friend of yours, John currently works for a computer software company. He is considering leaving his job to start his own business (as a sole trader) manufacturing specialist silicon computer chips John has never run his own business before and knowing that you are studying tax he has turned to you for advice in relation to his tax obligations He expects his sales turnover to be approximately 150,000 in the first twelve months of trading. He is planning to purchase a small factory, machinery, and a van for use in the business. He also has plans to employ a number of staff. He plans to start a pension both for him and will commence an employer pension for his employees and is planning to pay a contribution for his employees. He plans to pay his employees a salary, a bonus for good performance and will, at the option of his employees, provide a company car for their use (for both business and personal use). He will also pay their expenses for purchases made by them in the course of their employment (which are vouched as work expenses) and will provide a sum of 50 cach month for their fuel expenses for travelling to and from work. John will also pay into a Permanent Health insurance policy. He has also asked you for advice in relation to any tax exemptions or reliefs that he may be entitled to and that will minimise his tax liabilities. REQUIREMENT: Prepare a report for John detailing your advice in relation to his income tax, PAYE and VAT obligations Your report should include details of What taxes he should register for as a sole trader, and the procedures for registration (10 marks) 2 Basis of assessment for the income from his sole trade. (10 marks) 2. Allowable and disallowed expenses for his sole trade. (10 marks) 3. Allowable and disallowed expenses for his sole trade. (15 marks) 4. Tax relief for capital expenditure. (15 marks) 5. Tax obligations as an employer. (15 marks) 6. The treatment of his employees' remuneration and recommendations for minimising the tax liabilities of his employees. (15 marks) 7. Recommendations for minimising his overall tax liability