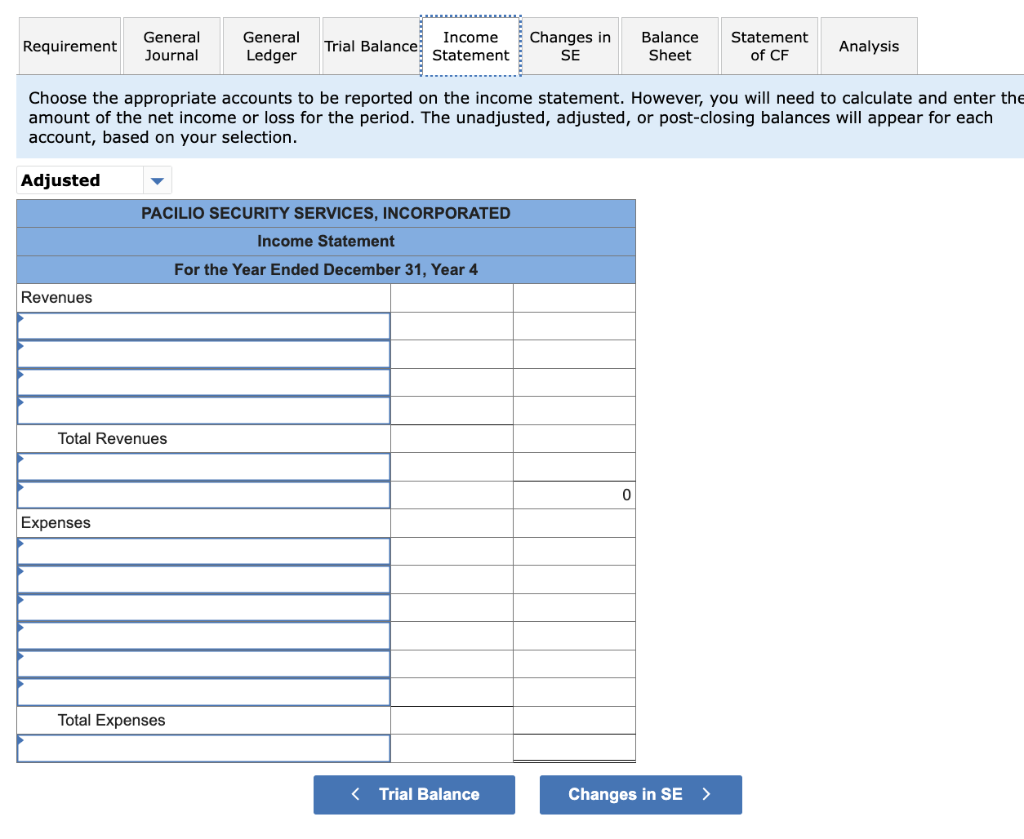

monitoring services. It plans to phase out its current service of providing security personnel at various events. The following summary transactions occurred during Year 4: 1. Paid the salaries payable from Year 3. 2. Acquired an additional $42,000 cash from the issue of common stock. 3. Rented a larger building on May 1; paid $6,000 for 12 months' rent in advance. 4. Paid $800 cash for supplies to be used over the next several months by the business. 5. Purchased alarm systems for resale at a cost of $12,000. The alarm systems were purchased on account with the terms 2/10,n/30 6. Returned alarm systems that had a cost of $240. 7. Installed alarm systems during the year for a total sales amount of $20,000. Sales of $15,000 were on account, while $5,000 were cash sales. 8. The cost of the systems sold in Event 7 amounted to $9,440. 9. Paid the installers and other employees a total of $9,500 in salaries. 10. Sold $36,000 of monitoring services for the year. The services are billed to the customers each month. 11. Paid cash on accounts payable. The payment was made before the discount period expired. At the time of purchase, the inventory has a cost of $8,000. 12. Paid cash to settle additional accounts payable in the amount of $2,780. The payment was made after the discount period expired. 13. Collected $43,000 of accounts receivable during the year. 14. Performed $12,000 of security services for area events; $9,000 was on account and $3,000 was for cash. 15. Paid advertising cost of $1,620 for the year. 16. Paid $1,100 for utilities expense for the year. 17. Paid a dividend of $12,000 to the shareholders. Adjustment Information 18. Supplies of $150 were on hand at the end of the year. 19. Recognized the expired rent for the year. 20. Recognized the balance of the unearned revenue; cash was received in Year 3 . 21. Accrued salaries at December 31 , Year 4 , were $1,500. Choose the appropriate accounts to be reported on the income statement. However, you will need to calculate and enter th amount of the net income or loss for the period. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. Prepare the statement of changes in stockholders' equity for the year ended December 31 , Year 4 . You will need to determine and enter the accounts and balances to prepare the Statement of Changes in Stockholders' Equity. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. The balance sheet is the accounting equation: Assets = Liabilities + Equity. Each asset and liability account is reported separately on the balance sheet. Choose the appropriate accounts to be reported on the balance sheet. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection