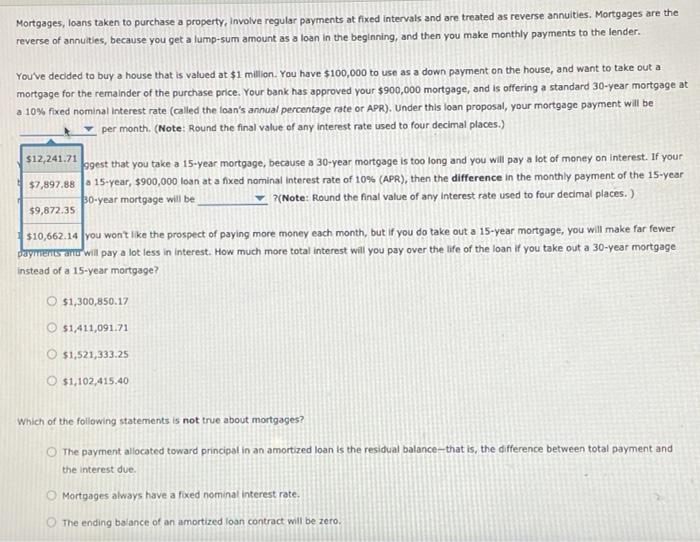

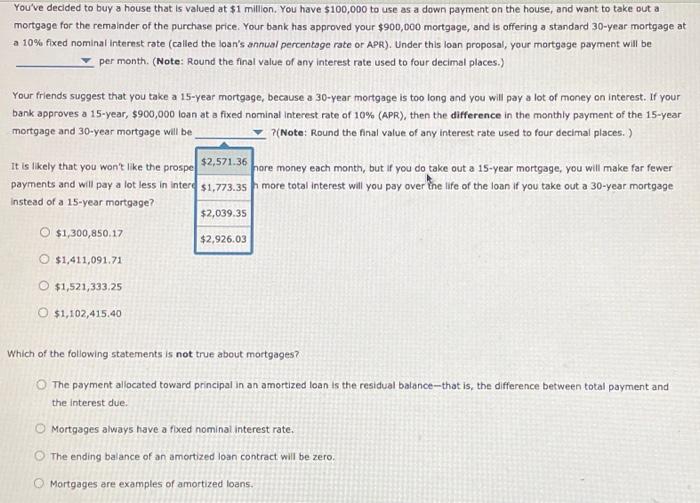

Mortgages, loans taken to purchase a property, Involve regular payments at fixed intervals and are treated as reverse annuities. Mortgages are the reverse of annuities, because you get a lump-sum amount as a loan in the beginning, and then you make monthly payments to the lender. You've decided to buy a house that is valued at $1 million. You have $100,000 to use as a down payment on the house, and want to take out a mortgage for the remainder of the purchase price. Your bank has approved your $900,000 mortgage, and is offering a standard 30-year mortgage at - 10% fixed nominal Interest rate (called the loan's annual percentage rate of APR). Under this loan proposal, your mortgage payment will be per month. (Note: Round the final value of any interest rate used to four decimal places.) $12,241.71 ggest that you take a 15-year mortgage, because a 30-year mortgage is too long and you will pay a lot of money on Interest. If your $7,897.88 15-year, $900,000 loan at a fixed nominal Interest rate of 10% (APR), then the difference in the monthly payment of the 15-year po-year mortgage will be (Note: Round the final value of any interest rate used to four decimal places. ) $9,872.35 $10,662.14 you won't like the prospect of paying more money each month, but if you do take out a 15-year mortgage, you will make far fewer dayters and will pay a lot less in interest. How much more total interest will you pay over the life of the loan if you take out a 30-year mortgage instead of a 15-year mortgage? $1,300,850.17 $1,411,091.71 $1,521,333.25 O $1,102,415.40 Which of the following statements is not true about mortgages? The payment allocated toward principal in an amortized loan is the residual balance-that is, the difference between total payment and the interest due. Mortgages always have a fixed nominal interest rate. The ending balance of an amortized loan contract will be zero. a You've decided to buy a house that is valued at $1 million. You have $100,000 to use as a down payment on the house, and want to take out a mortgage for the remainder of the purchase price. Your bank has approved your $900,000 mortgage, and is offering a standard 30-year mortgage at a 10% fixed nominal Interest rate (called the loan's annual percentage rate or APR). Under this loan proposal, your mortgage payment will be per month. (Note: Round the final value of any interest rate used to four decimal places.) Your friends suggest that you take a 15-year mortgage, because a 30-year mortgage is too long and you will pay a lot of money on interest. If your bank approves a 15-year, $900,000 loan at a fixed nominal Interest rate of 10% (APR), then the difference in the monthly payment of the 15-year mortgage and 30-year mortgage will be (Note: Round the final value of any interest rate used to four decimal places.) It is likely that you won't like the prospe $2,571.36 pore money each month, but if you do take out a 15-year mortgage, you will make far fewer payments and will pay a lot less in intere $1,773.35 more total interest will you pay over the life of the loan if you take out a 30-year mortgage Instead of a 15-year mortgage? $2,039.35 O $1,300,850.17 $2,926.03 $1,411,091.71 $1,521,333,25 $1,102,415.40 Which of the following statements is not true about mortgages The payment alocated toward principal in an amortized loan is the residual balance--that is, the difference between total payment and the interest due. Mortgages always have a fixed nominal interest rate. The ending balance of an amortized loan contract will be zero, Mortgages are examples of amortized loans