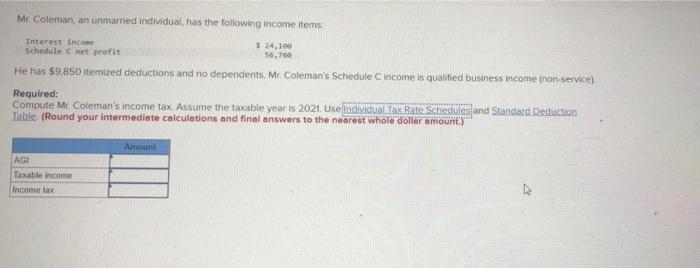

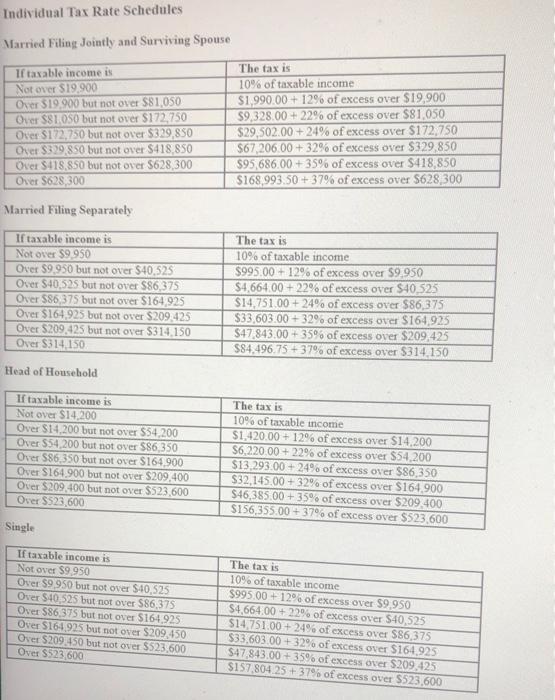

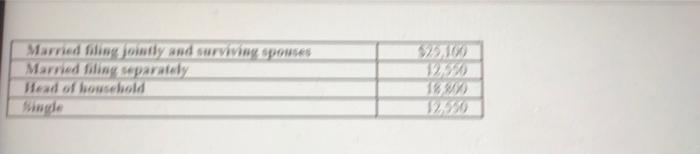

Mr Coleman, an unmarried individual, has the following income items 5.24,100 56.760 Interest Income Schedule Cnet profit He has $9.850 itemized deductions and no dependents. Mr. Coleman's Schedule C income is qualified business income (non-service) Required: Compute Mr Coleman's income tax Assume the taxable year is 2021. Use Individual Tax Rate Schedules and Standard Deduction Table (Round your intermediate calculations and final answers to the nearest whole dollar amount.) Amount AGI Taxable income Income tax Individual Tax Rate Schedules Married Filing Jointly and Surviving Spouse If taxable income is Not over $19.900 Over $19.900 but not over $81,050 Over $81.050 but not over $172,750 Over $172,750 but not over $329,850 Oker $339,850 but not over $418,850 Ovet S418,850 but not over $628,300 Over 5628,300 The fax is 10% of taxable income $1,990.00 + 12% of excess over $19,900 $9,328.00 + 22% of excess over $81.050 $29,502.00 +24% of excess over $172.750 $67,206,00 + 32% of excess over $329,850 $95,686,00 + 35% of excess over $418,850 $168.993.50 +37% of excess over $628,300 Married Filing Separately If taxable income is Not over $9.950 Over $9.950 but not over $40.525 Over $40.52S but not over $86,375 Over $86,375 but not over $164.925 Over $164.925 but not over $209,425 Over $209,425 but not over $314.150 Over $314.150 The tax is 10% of taxable income $995.00 +12% of excess over $9.950 $4,664.00 +22% of excess over $40.525 $14,751.00 +24% of excess over $86,375 $33,603.00 +32% of excess over $164.925 $47,843.00 + 35% of excess over $209,425 $84.496.75 +37% of excess over $314.150 Head of Household If taxable income is Not over $14,200 Over $14,200 but not over $54,200 Over $54,200 but not over $86,350 Over $86 350 but not over $164.900 Over $164.900 but not over $209,400 Over $209,400 but not over S523,600 Over S523,600 The taxis 10% of taxable income $1.420.00 + 12% of excess over $14,200 $6.220.00 + 22% of excess over $54,200 $13,293.00 +24% of excess over $86,350 $32,145.00 +32% of excess over $164.900 $46,385.00+ 35% of excess over $209,400 $156,355.00 +37% of excess over $523,600 Single If taxable income is Not over $9.950 Over $9 950 but not over $10.525 Over $40.525 but not over $86,375 Over $86,375 but not over $164,925 Over $164.925 but not over $209,450 Over S209.450 but not over $S23.600 Over S523,600 The tas is 10% of taxable income $995.00 +12 6 of excess over $9.950 $4,664,00 + 22% of excess over $40,525 $14,751.00 +24% of excess over $86,375 $33,603.00 +32% of excess over $164.925 $47,843.00 +35% of excess over $209,425 $157,80425 + 37% of excess over S523,600 Married filing jointly and surviving spouses Married filing separately Head of household Single W320