Mrs. Cora Yank (age 42) is divorced and has full custody of her 10-year-old son, William.

- Mrs. Yank works as a medical technician in a Chicago hospital. Her salary was $38,400, from which her employer withheld $1,045 federal income tax and $2,938 employee FICA tax.

- Several years ago, Mrs. Yank was seriously injured in a traffic accident caused by another drivers negligence. This year, she received a $25,000 settlement from the drivers insurance company: $20,000 as compensation for her physical injuries and $5,000 for lost wages during her convalescent period. Because she was unable to work for the first seven weeks of the year, she collected $1,400 unemployment compensation from the state of Illinois.

- Mrs. Yank earned $629 interest on a savings account. She contributed $800 to a traditional IRA. She is not an active participant in any other qualified retirement plan.

- Mrs. Yank paid $10,800 rent on the apartment in which she and William live. She received $1,600 alimony and $2,350 child support from her former husband under a divorce agreement executed in 2013.

- Mrs. Yank is covered under her employers medical reimbursement plan. However, this years medical bills exceeded her reimbursement limit by $1,630.

- Mrs. Yank paid $1,062 income tax to Illinois.

- Mrs. Yank spent $470 on hospital shoes and uniforms. Her employer didnt reimburse her for this expense.

- Mrs. Yank paid $1,300 for after-school child care for William.

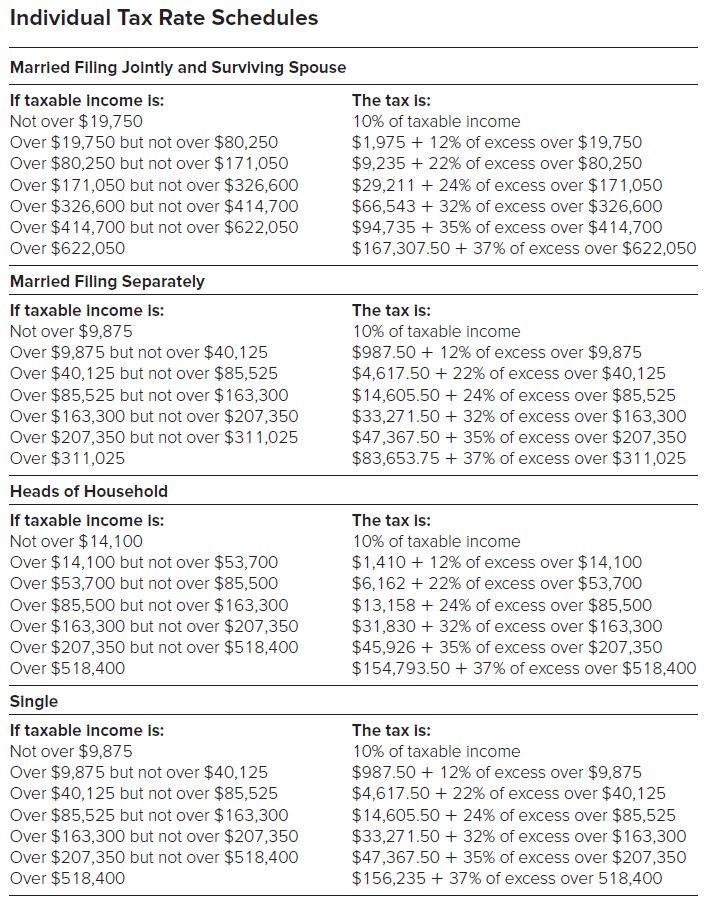

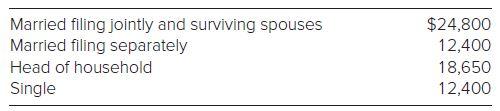

Required: From the above information, compute Mrs. Yanks 2020 federal income tax (including any AMT) and the amount due with her Form 1040 or the refund she should receive. Assume the tax year is 2020. Use Individual tax rate schedules and Standard deduction table. (Round all your intermediate calculations and final answers to the nearest whole dollar amount.)

Standard Deduction Table

Individual Tax Rate Schedules Married Filing Jointly and Surviving Spouse The tax is: If taxable income is: Not over $19,750 Over $19,750 but not over $80,250 Over $80,250 but not over $171,050 Over $171,050 but not over $326,600 Over $326,600 but not over $414,700 Over $414,700 but not over $622,050 Over $622,050 10% of taxable income $1,975 + 12% of excess over $19,750 $9,235 + 22% of excess over $80,250 $29,211 + 24% of excess over $171,050 $66,543 + 32% of excess over $326,600 $94,735 + 35% of excess over $414,700 $167,307.50 + 37% of excess over $622,050 Married Filing Separately If taxable income is: Not over $9,875 Over $9,875 but not over $40,125 Over $40,125 but not over $85,525 Over $85,525 but not over $163,300 Over $ 163,300 but not over $207,350 Over $207,350 but not over $311,025 Over $311,025 The tax is: 10% of taxable income $987.50 + 12% of excess over $9,875 $4,617.50 + 22% of excess over $40,125 $14,605.50 + 24% of excess over $85,525 $33,271.50 + 32% of excess over $163,300 $47,367.50 + 35% excess over $207,350 $83,653.75 + 37% of excess over $311,025 Heads of Household The tax is: If taxable income is: Not over $14,100 Over $14,100 but not over $53,700 Over $53,700 but not over $85,500 Over $85,500 but not over $163,300 Over $163,300 but not over $207,350 Over $207,350 but not over $518,400 Over $518,400 10% of taxable income $1,410 + 12% of excess over $14,100 $6,162 + 22% of excess over $53,700 $13,158 +24% of excess over $85,500 $31,830 + 32% of excess over $163,300 $45,926 + 35% of excess over $207,350 $154,793.50 + 37% of excess over $518,400 Single If taxable income is: Not over $9,875 Over $9,875 but not over $40,125 Over $40,125 but not over $85,525 Over $85,525 but not over $163,300 Over $163,300 but not over $207,350 Over $207,350 but not over $518,400 Over $518,400 The tax is: 10% of taxable income $987.50 + 12% of excess over $9,875 $4,617.50 + 22% of excess over $40,125 $14,605.50 + 24% of excess over $85,525 $33,271.50 + 32% of excess over $163,300 $47,367.50 + 35% of excess over $207,350 $156,235 + 37% of excess over 518,400 Married filing jointly and surviving spouses Married filing separately Head of household Single $24,800 12,400 18,650 12,400 Individual Tax Rate Schedules Married Filing Jointly and Surviving Spouse The tax is: If taxable income is: Not over $19,750 Over $19,750 but not over $80,250 Over $80,250 but not over $171,050 Over $171,050 but not over $326,600 Over $326,600 but not over $414,700 Over $414,700 but not over $622,050 Over $622,050 10% of taxable income $1,975 + 12% of excess over $19,750 $9,235 + 22% of excess over $80,250 $29,211 + 24% of excess over $171,050 $66,543 + 32% of excess over $326,600 $94,735 + 35% of excess over $414,700 $167,307.50 + 37% of excess over $622,050 Married Filing Separately If taxable income is: Not over $9,875 Over $9,875 but not over $40,125 Over $40,125 but not over $85,525 Over $85,525 but not over $163,300 Over $ 163,300 but not over $207,350 Over $207,350 but not over $311,025 Over $311,025 The tax is: 10% of taxable income $987.50 + 12% of excess over $9,875 $4,617.50 + 22% of excess over $40,125 $14,605.50 + 24% of excess over $85,525 $33,271.50 + 32% of excess over $163,300 $47,367.50 + 35% excess over $207,350 $83,653.75 + 37% of excess over $311,025 Heads of Household The tax is: If taxable income is: Not over $14,100 Over $14,100 but not over $53,700 Over $53,700 but not over $85,500 Over $85,500 but not over $163,300 Over $163,300 but not over $207,350 Over $207,350 but not over $518,400 Over $518,400 10% of taxable income $1,410 + 12% of excess over $14,100 $6,162 + 22% of excess over $53,700 $13,158 +24% of excess over $85,500 $31,830 + 32% of excess over $163,300 $45,926 + 35% of excess over $207,350 $154,793.50 + 37% of excess over $518,400 Single If taxable income is: Not over $9,875 Over $9,875 but not over $40,125 Over $40,125 but not over $85,525 Over $85,525 but not over $163,300 Over $163,300 but not over $207,350 Over $207,350 but not over $518,400 Over $518,400 The tax is: 10% of taxable income $987.50 + 12% of excess over $9,875 $4,617.50 + 22% of excess over $40,125 $14,605.50 + 24% of excess over $85,525 $33,271.50 + 32% of excess over $163,300 $47,367.50 + 35% of excess over $207,350 $156,235 + 37% of excess over 518,400 Married filing jointly and surviving spouses Married filing separately Head of household Single $24,800 12,400 18,650 12,400