*Must have IDEA Data Files from Connect*

Overall Skills Assignment 3: Keystone Accounts Receivable, Part 1 (IDEA Required)

Click the link for question details. Overall Skills Assignment 3: Keystone Accounts Receivable, Part 1

Required Data Files:

11B-4 Keystone Approved Credit Customers

11B-4_Keystone AR by Invoice

IDEA 10 C1202 IDEA Data Analysis Workbook

(Enter your answers exactly as they appear in IDEA.)

Required:

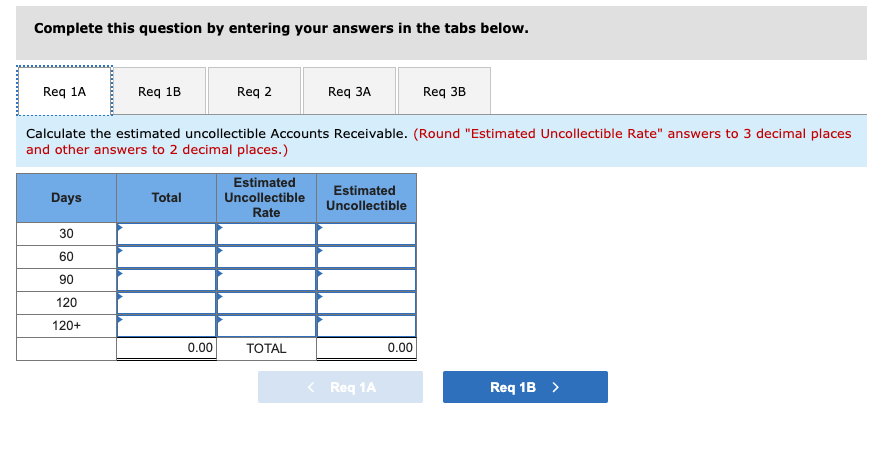

1-a. Calculate the estimated uncollectible Accounts Receivable.

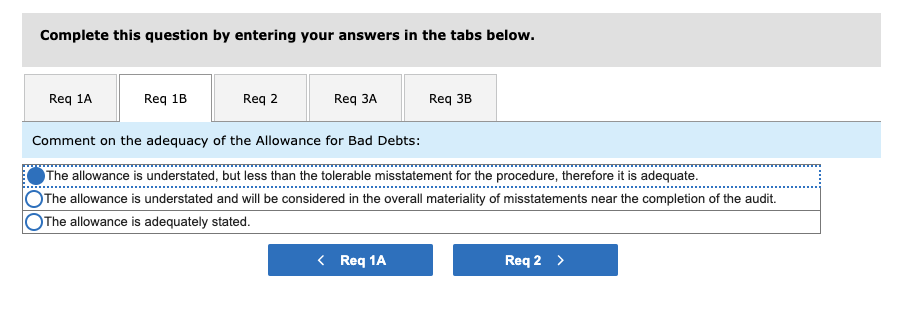

1-b. Comment on the adequacy of the Allowance for Bad Debts:

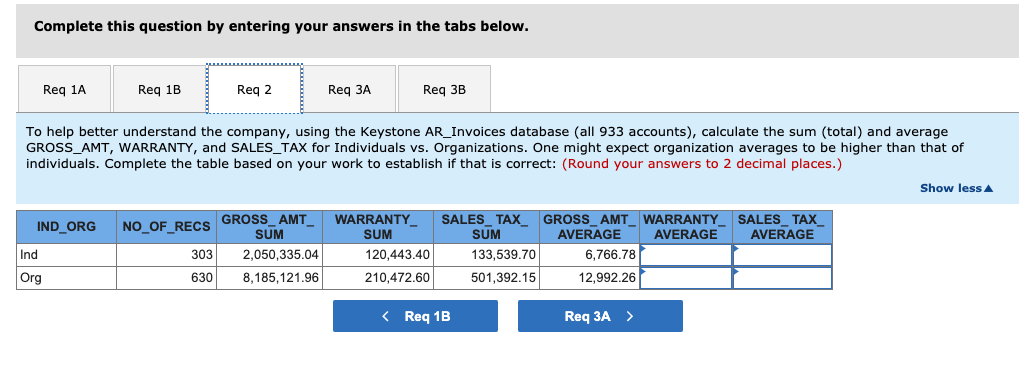

2. To help better understand the company, using the Keystone AR_Invoices database (all 933 accounts), calculate the sum (total) and average GROSS_AMT, WARRANTY, and SALES_TAX for Individuals vs. Organizations. One might expect organization averages to be higher than that of individuals. Complete the table based on your work to establish if that is correct:

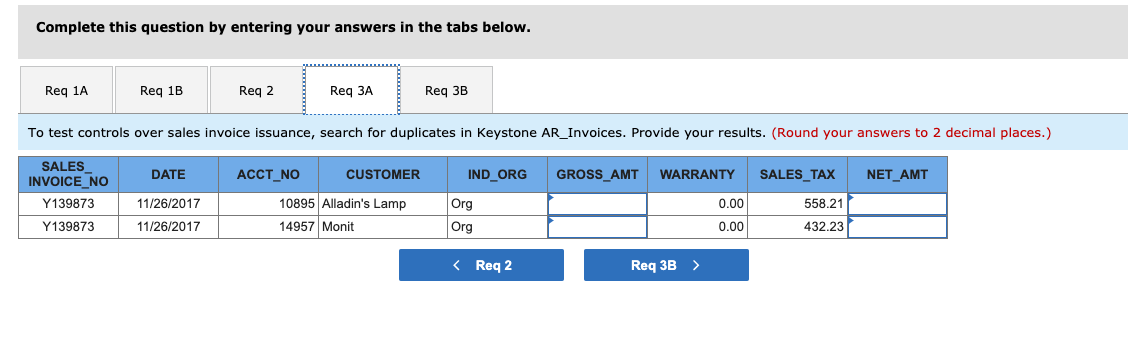

3-a. To test controls over sales invoice issuance, search for duplicates in Keystone AR_Invoices. Provide your results.

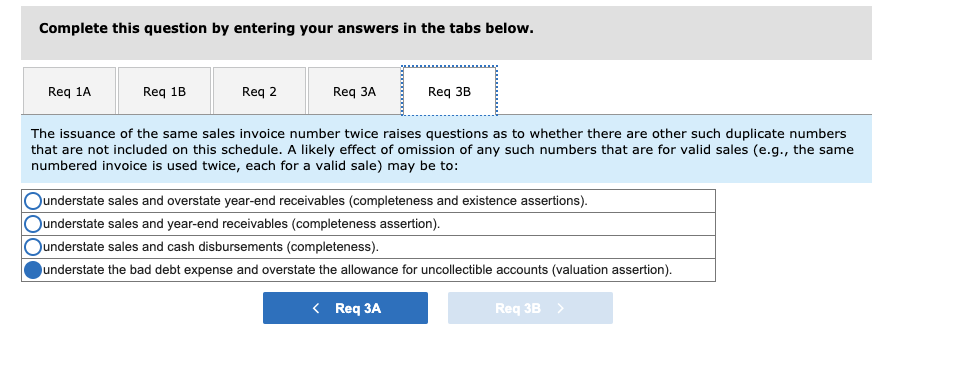

3-b. The issuance of the same sales invoice number twice raises questions as to whether there are other such duplicate numbers that are not included on this schedule. A likely effect of omission of any such numbers that are for valid sales (e.g., the same numbered invoice is used twice, each for a valid sale) may be to:

Complete this question by entering your answers in the tabs below. Req 1A Req 1B Reg 2 Req 3A Req 3B Calculate the estimated uncollectible Accounts Receivable. (Round "Estimated Uncollectible Rate" answers to 3 decimal places and other answers to 2 decimal places.) Days Total Estimated Uncollectible Rate Estimated Uncollectible 30 60 90 120 120+ 0.00 TOTAL 0.00 Complete this question by entering your answers in the tabs below. Req 1A Reg 1B Req 2 Req Req 3B Comment on the adequacy of the Allowance for Bad Debts: The allowance is understated, but less than the tolerable misstatement for the procedure, therefore it is adequate. The allowance is understated and will be considered in the overall materiality of misstatements near the completion of the audit. The allowance is adequately stated. Complete this question by entering your answers in the tabs below. Reg 1A Req 1B Req 2 Req 3A Req 3B To help better understand the company, using the Keystone AR_Invoices database (all 933 accounts), calculate the sum (total) and average GROSS_AMT, WARRANTY, and SALES_TAX for Individuals vs. Organizations. One might expect organization averages to be higher than that of individuals. Complete the table based on your work to establish if that is correct: (Round your answers to 2 decimal places.) Show less A IND_ORG NO_OF_RECS SALES_TAX_ AVERAGE Ind 303 GROSS AMT SUM 2,050,335.04 8,185,121.96 WARRANTY SUM 120,443.40 210,472.60 SALES TAX. GROSS_AMT_ WARRANTY SUM AVERAGE AVERAGE 133,539.70 6,766.78 501,392.15 12,992.26 Org 630 Complete this question by entering your answers in the tabs below. Req 1A Req 1B Req 2 Req Req 3B To test controls over sales invoice issuance, search for duplicates in Keystone AR_Invoices. Provide your results. (Round your answers to 2 decimal places.) DATE ACCT_NO CUSTOMER IND_ORG GROSS_AMT WARRANTY SALES_TAX NET_AMT SALES INVOICE NO Y139873 Y139873 11/26/2017 0.00 558.21 10895 Alladin's Lamp 14957 Monit Org Org 11/26/2017 0.00 432.23 Complete this question by entering your answers in the tabs below. Req 1A Reg 1B Reg 2 Req Req 3B The issuance of the same sales invoice number twice raises questions as to whether there are other such duplicate numbers that are not included on this schedule. A likely effect of omission of any such numbers that are for valid sales (e.g., the same numbered invoice is used twice, each for a valid sale) may be to: Ounderstate sales and overstate year-end receivables (completeness and existence assertions). O understate sales and year-end receivables (completeness assertion). understate sales and cash disbursements (completeness). understate the bad debt expense and overstate the allowance for uncollectible accounts (valuation assertion). Complete this question by entering your answers in the tabs below. Req 1A Reg 1B Req 2 Req Req 3B Comment on the adequacy of the Allowance for Bad Debts: The allowance is understated, but less than the tolerable misstatement for the procedure, therefore it is adequate. The allowance is understated and will be considered in the overall materiality of misstatements near the completion of the audit. The allowance is adequately stated. Complete this question by entering your answers in the tabs below. Reg 1A Req 1B Req 2 Req 3A Req 3B To help better understand the company, using the Keystone AR_Invoices database (all 933 accounts), calculate the sum (total) and average GROSS_AMT, WARRANTY, and SALES_TAX for Individuals vs. Organizations. One might expect organization averages to be higher than that of individuals. Complete the table based on your work to establish if that is correct: (Round your answers to 2 decimal places.) Show less A IND_ORG NO_OF_RECS SALES_TAX_ AVERAGE Ind 303 GROSS AMT SUM 2,050,335.04 8,185,121.96 WARRANTY SUM 120,443.40 210,472.60 SALES TAX. GROSS_AMT_ WARRANTY SUM AVERAGE AVERAGE 133,539.70 6,766.78 501,392.15 12,992.26 Org 630 Complete this question by entering your answers in the tabs below. Req 1A Req 1B Req 2 Req Req 3B To test controls over sales invoice issuance, search for duplicates in Keystone AR_Invoices. Provide your results. (Round your answers to 2 decimal places.) DATE ACCT_NO CUSTOMER IND_ORG GROSS_AMT WARRANTY SALES_TAX NET_AMT SALES INVOICE NO Y139873 Y139873 11/26/2017 0.00 558.21 10895 Alladin's Lamp 14957 Monit Org Org 11/26/2017 0.00 432.23 Complete this question by entering your answers in the tabs below. Req 1A Reg 1B Reg 2 Req Req 3B The issuance of the same sales invoice number twice raises questions as to whether there are other such duplicate numbers that are not included on this schedule. A likely effect of omission of any such numbers that are for valid sales (e.g., the same numbered invoice is used twice, each for a valid sale) may be to: Ounderstate sales and overstate year-end receivables (completeness and existence assertions). O understate sales and year-end receivables (completeness assertion). understate sales and cash disbursements (completeness). understate the bad debt expense and overstate the allowance for uncollectible accounts (valuation assertion).