Answered step by step

Verified Expert Solution

Question

1 Approved Answer

My teacher gets WA = .6 and WB = .4 I don't know how he got WA. Thanks Question 7: Portfolio Weights Suppose stock A

My teacher gets WA = .6 and WB = .4

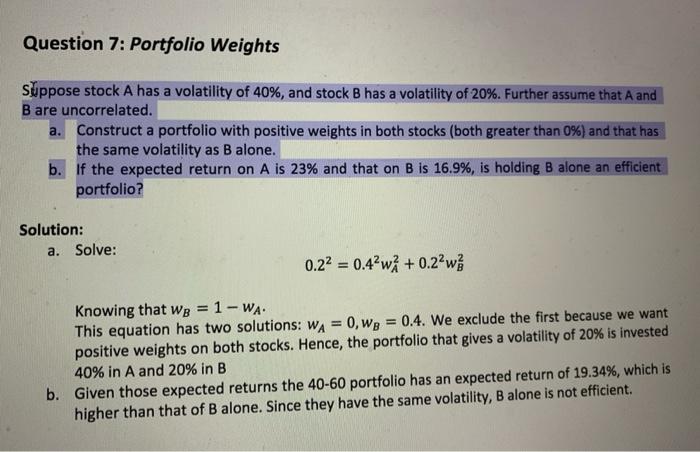

Question 7: Portfolio Weights Suppose stock A has a volatility of 40%, and stock B has a volatility of 20%. Further assume that A and Bare uncorrelated. a. Construct a portfolio with positive weights in both stocks (both greater than 0%) and that has the same volatility as B alone. b. If the expected return on A is 23% and that on B is 16.9%, is holding B alone an efficient portfolio? Solution: a. Solve: 0.22 = 0.42w +0.22w Knowing that we = 1 - WA. This equation has two solutions: WA = 0,wg = 0.4. We exclude the first because we want positive weights on both stocks. Hence, the portfolio that gives a volatility of 20% is invested 40% in A and 20% in B b. Given those expected returns the 40-60 portfolio has an expected return of 19.34%, which is higher than that of B alone. Since they have the same volatility, B alone is not efficient. Question 7: Portfolio Weights Suppose stock A has a volatility of 40%, and stock B has a volatility of 20%. Further assume that A and Bare uncorrelated. a. Construct a portfolio with positive weights in both stocks (both greater than 0%) and that has the same volatility as B alone. b. If the expected return on A is 23% and that on B is 16.9%, is holding B alone an efficient portfolio? Solution: a. Solve: 0.22 = 0.42w +0.22w Knowing that we = 1 - WA. This equation has two solutions: WA = 0,wg = 0.4. We exclude the first because we want positive weights on both stocks. Hence, the portfolio that gives a volatility of 20% is invested 40% in A and 20% in B b. Given those expected returns the 40-60 portfolio has an expected return of 19.34%, which is higher than that of B alone. Since they have the same volatility, B alone is not efficient I don't know how he got WA. Thanks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banker To The World

Authors: William Rhodes

1st Edition

0071704256, 978-0071704250