Answered step by step

Verified Expert Solution

Question

1 Approved Answer

My = % to 2 decimal places y = % to 2 decimal places (10 points) Additionally, a risk-free asset with return r =

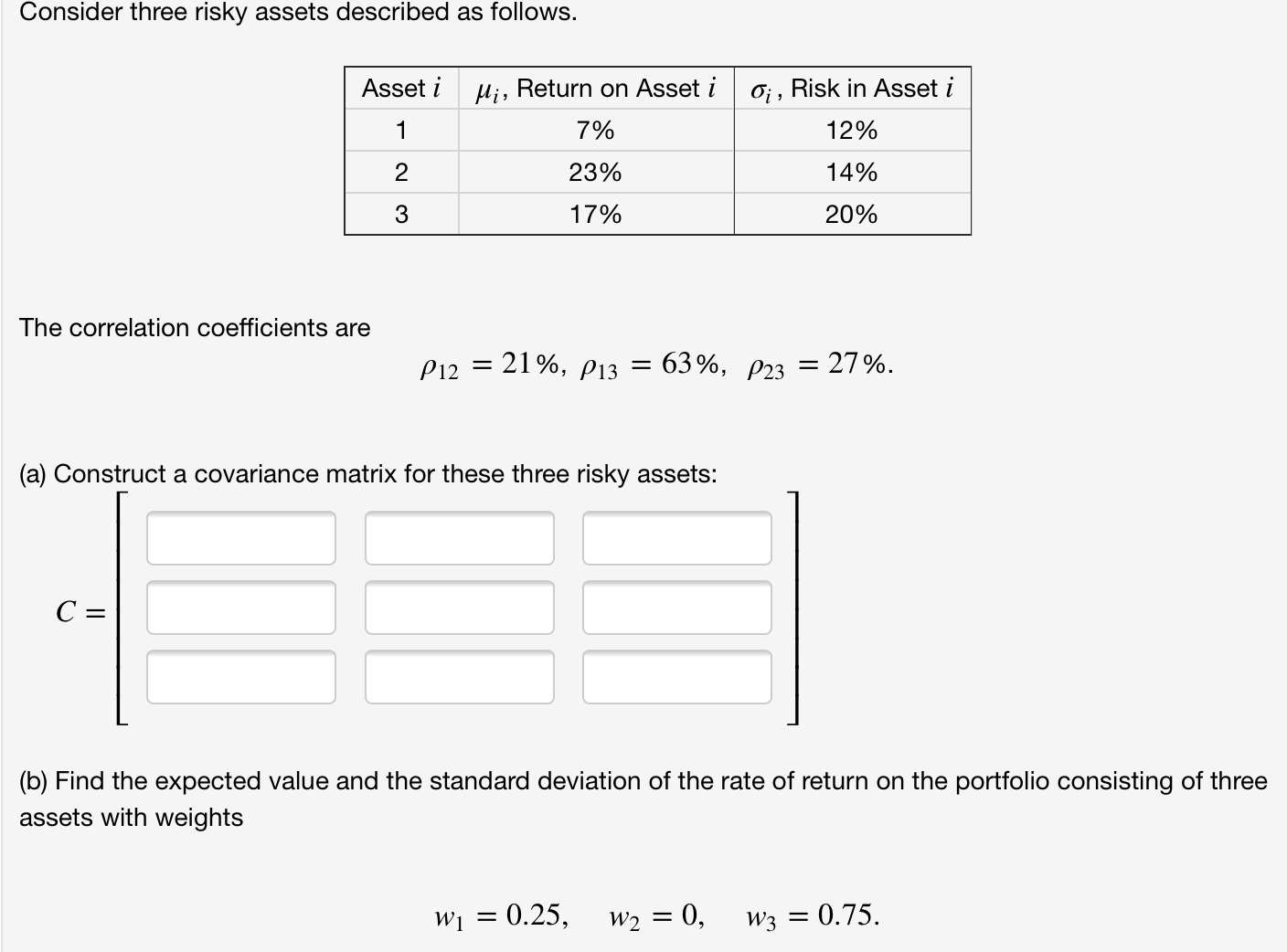

My = % to 2 decimal places y = % to 2 decimal places (10 points) Additionally, a risk-free asset with return r = 5% is available. On a blank piece of paper, sketch a risk-return diagram, where you should mark the following: the three risky assets #1, #2, #3 and the risk-free asset; (i) the portfolio line for the risky assets #1 and #2; (ii) the minimum variance line for all risky assets; (iii) the smallest variance portfolio in the risky assets; (iv) the market portfolio; (v) the efficient frontier for portfolios in the risky assets; (vi) the efficient frontier for four-asset portfolios. Use the numbers (i)-(vi) and (#1)-(#3) as labels. Consider three risky assets described as follows. Asset i Mi, Return on Asset i Oi, Risk in Asset i 1 7% 12% 2 23% 14% 3 17% 20% The correlation coefficients are P12 = 21%, P13 = 63%, P23 = 27%. (a) Construct a covariance matrix for these three risky assets: C = (b) Find the expected value and the standard deviation of the rate of return on the portfolio consisting of three assets with weights W = 0.25, W = 0, W3 = = 0.75.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111