Answered step by step

Verified Expert Solution

Question

1 Approved Answer

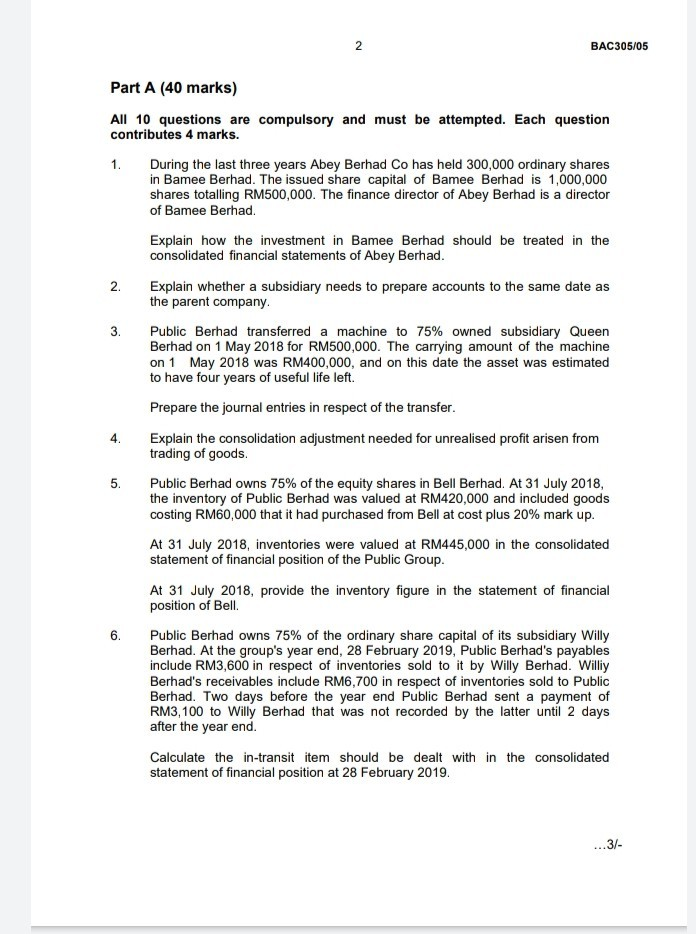

N BAC305/05 Part A (40 marks) All 10 questions are compulsory and must be attempted. Each question contributes 4 marks. 1. During the last three

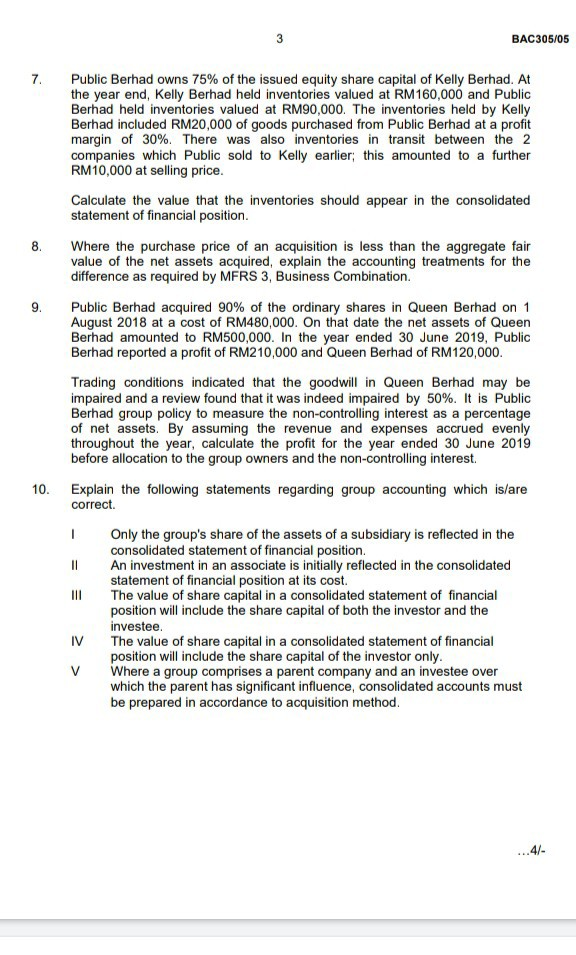

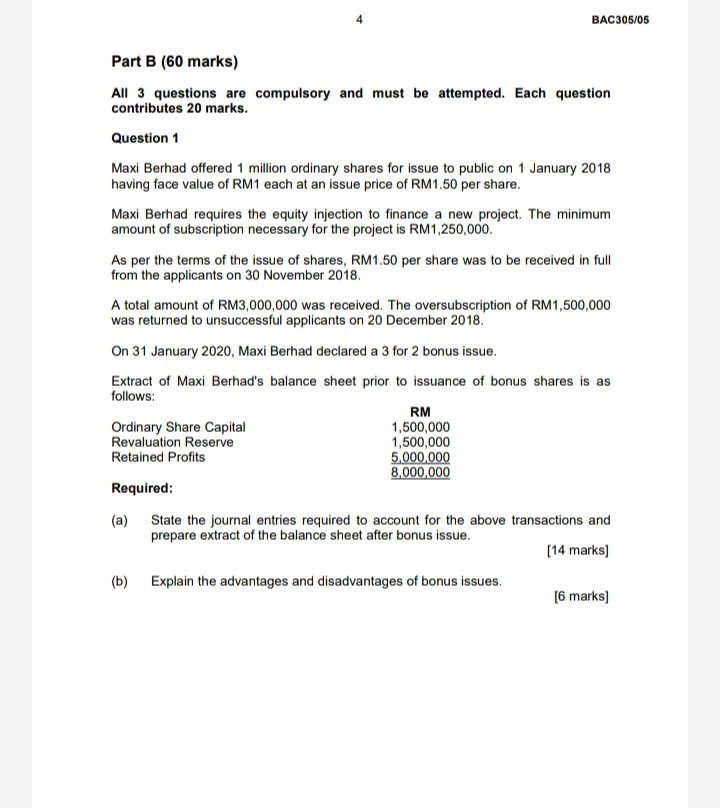

N BAC305/05 Part A (40 marks) All 10 questions are compulsory and must be attempted. Each question contributes 4 marks. 1. During the last three years Abey Berhad Co has held 300,000 ordinary shares in Bamee Berhad. The issued share capital of Bamee Berhad is 1,000,000 shares totalling RM500,000. The finance director of Abey Berhad is a director of Bamee Berhad Explain how the investment in Bamee Berhad should be treated in the consolidated financial statements of Abey Berhad. 2. Explain whether a subsidiary needs to prepare accounts to the same date as the parent company 3. Public Berhad transferred a machine to 75% owned subsidiary Queen Berhad on 1 May 2018 for RM500,000. The carrying amount of the machine on 1 May 2018 was RM400,000, and on this date the asset was estimated to have four years of useful life left. Prepare the journal entries in respect of the transfer. Explain the consolidation adjustment needed for unrealised profit arisen from trading of goods. 5. Public Berhad owns 75% of the equity shares in Bell Berhad. At 31 July 2018, the inventory of Public Berhad was valued at RM420,000 and included goods costing RM60,000 that it had purchased from Bell at cost plus 20% mark up. At 31 July 2018, inventories were valued at RM445,000 in the consolidated statement of financial position of the Public Group. At 31 July 2018, provide the inventory figure in the statement of financial position of Bell. 6. Public Berhad owns 75% of the ordinary share capital of its subsidiary Willy Berhad. At the group's year end, 28 February 2019, Public Berhad's payables include RM3,600 in respect of inventories sold to it by Willy Berhad. Williy Berhad's receivables include RM6,700 in respect of inventories sold to Public Berhad. Two days before the year end Public Berhad sent a payment of RM3, 100 to Willy Berhad that was not recorded by the latter until 2 days after the year end. Calculate the in-transit item should be dealt with in the consolidated statement of financial position at 28 February 2019. ...3/- 3 BAC305/05 7 8. 9. Public Berhad owns 75% of the issued equity share capital of Kelly Berhad. At the year end, Kelly Berhad held inventories valued at RM160,000 and Public Berhad held inventories valued at RM90,000. The inventories held by Kelly Berhad included RM20,000 of goods purchased from Public Berhad at a profit margin of 30%. There was also inventories in transit between the 2 companies which Public sold to Kelly earlier this amounted to a further RM10,000 at selling price. Calculate the value that the inventories should appear in the consolidated statement of financial position. Where the purchase price of an acquisition is less than the aggregate fair value of the net assets acquired, explain the accounting treatments for the difference as required by MFRS 3, Business Combination. Public Berhad acquired 90% of the ordinary shares in Queen Berhad on 1 August 2018 at a cost of RM480,000. On that date the net assets of Queen Berhad amounted to RM500,000. In the year ended 30 June 2019, Public Berhad reported a profit of RM210,000 and Queen Berhad of RM120,000. Trading conditions indicated that the goodwill in Queen Berhad may be impaired and a review found that it was indeed impaired by 50%. It is Public Berhad group policy to measure the non-controlling interest as a percentage of net assets. By assuming the revenue and expenses accrued evenly throughout the year, calculate the profit for the year ended 30 June 2019 before allocation to the group owners and the non-controlling interest Explain the following statements regarding group accounting which is/are correct Only the group's share of the assets of a subsidiary is reflected in the consolidated statement of financial position. An investment in an associate is initially reflected in the consolidated statement of financial position at its cost. III The value of share capital in a consolidated statement of financial position will include the share capital of both the investor and the investee IV The value of share capital in a consolidated statement of financial position will include the share capital of the investor only. V Where a group comprises a parent company and an investee over which the parent has significant influence, consolidated accounts must be prepared in accordance to acquisition method. 10. - = ...4/- BAC305/05 Part B (60 marks) All 3 questions are compulsory and must be attempted. Each question contributes 20 marks. Question 1 Maxi Berhad offered 1 million ordinary shares for issue to public on 1 January 2018 having face value of RM1 each at an issue price of RM1.50 per share. Maxi Berhad requires the equity injection to finance a new project. The minimum amount of subscription necessary for the project is RM1,250,000. As per the terms of the issue of shares, RM1.50 per share was to be received in full from the applicants on 30 November 2018 A total amount of RM3,000,000 was received. The oversubscription of RM1,500,000 was returned to unsuccessful applicants on 20 December 2018. On 31 January 2020, Maxi Berhad declared a 3 for 2 bonus issue. Extract of Maxi Berhad's balance sheet prior to issuance of bonus shares is as follows: RM Ordinary Share Capital 1,500,000 Revaluation Reserve 1,500,000 Retained Profits 5,000,000 8,000,000 Required: (a) State the journal entries required to account for the above transactions and prepare extract of the balance sheet after bonus issue. [14 marks) (b) Explain the advantages and disadvantages of bonus issues. [6 marks) BAC305/05 Question 2 North Berhad, a public limited company, acquired 80% ordinary shares in East Berhad on 1 January 2017 for RM8,640,000 when the accumulated retained earnings of East Berhad were RM2,000,000. North Berhad also acquired one third (1/3) of the issued ordinary share capital in West Berhad on 1 July 2019 for RM4,000,000 Balance sheets of the three companies as at 31 December 2019 are given below: North East West Non-current assets RM'000 RM'000 RM'000 Freehold property 10,000 1,000 Plant and equipment 6,100 7,400 8,550 Investments in companies 14,000 1,820 510 30,100 10,220 9,060 Current assets Inventories 1,660 680 600 Accounts receivable 1,040 580 Cash and cash equivalents 480 100 150 3,180 1,360 1,050 Current liabilities Accounts payable 1,240 2,120 750 Taxation 440 500 60 1,680 2,620 810 300 Net current assets 1,500 31,600 (1,260) 8,960 240 9,300 500 Financed by Ordinary shares capital 10,000 3,600 3,000 Retained profit b/f 12,000 3,260 4,500 Profit for the year 8,600 1,600 1,800 Non-current Liabilities 8% Loan note 1,000 10% Bonds 31,600 8,960 9,300 Additional information: (1) On February 2017, East declared and paid a net dividend of RM350,000 for the year 2016. North credited its income statement with its share of the dividend received (2) On 1 January 2019, North acquired 60% of the 10% bonds issued by East paying RM300,000 ...6/- BAC305/05 (3) On 1 January 2017, a piece of land of East had a fair value of RM240,000 in excess of its book value. The value this land had not changed since acquisition (4) During 2019, North sold goods to East for RM260,000. Two thirds of these goods were still in inventory of East at 31 December 2019. In November 2019 North sold inventory for RM130,000 to West and West has not sold any of these inventory. North transfers inventory to East and West at a mark up of 30% on cost (5) As at the end of the year, East had not provided for the second half-year interest on the 10% Bonds. (6) Included in accounts payable of East was an amount of RM70,000 due to North. However, North has factored without recourse, RM40,000 of these accounts receivable. (7) The group accounting policy for goodwill is to write it off on a straight-line basis over a period of five years with a proportionate charge where it arises part way through an accounting period. The amortisation of goodwill has not been recorded in the book yet. (8) Assume that income and expenses accrue evenly throughout the year. Required: (a) Prepare a consolidated statement of financial position for North Berhad and its subsidiary as at 31 December 2019, incorporating its associate in accordance with MFRS 128; (b) Lay out workings for (0) Goodwill (ii) Group retained earnings Minority interest; and (iv) Investment in associates. [20 marks) ...71- Question 3 (a) Tobaco Berhad, with the Ringgit Malaysia as its functional currency, purchases plant from a foreign entity for $18 million on 31 May 2019 when the exchange rate was $2 to RM1. The entity also sells goods to a foreign customer for $10.5million on 30 September 2019, when the exchange rate was $1.75 to RM1. At the entity's year end of 31 December 2019, both amounts are still outstanding and have not been paid. The closing exchange rate was $1.5 to RM1. Required: Explain the accounting treatment for both sale and purchases transactions for Tobacco Berhad [5 marks) (b) Truly Berhad has a 100%-owned foreign subsidiary, which has a carrying value at a cost of RM25 million. It sells the subsidiary on 31 December 2019 for $45million. As at 31 December 2019, the credit balance on the exchange reserve, which relates to this subsidiary, was RM6 million. The functional currency of the entity is the Ringgit Malaysia and the exchange rate on 31 December 2019 is RM1 to $1.5. The net asset value of the subsidiary at the date of disposal was RM28 million. Required: Explain the accounting treatment for the disposal transaction. [4 marks) (c) Public Bhd, a company incorporated in Malaysia, whose functional currency is the Ringgit Malaysia (RM) and whose year ends on 31 December, has two overseas subsidiaries. Public is preparing to finalise its financial statements for the year ended 31 December 2019 and has the following inter-company accounts with the two subsidiaries: (0) A loan of INR8 million to Republic, a company in India whose functional currency is the Indian Rupee (INR), which has been outstanding since the acquisition of Republic in 2015 and which it does not regard as repayable in the foreseeable future. (ii) A trade receivables account balance amounting to RM300,000 from Private, a foreign company whose functional currency is the Rupiah, held in the books of Private at 725 million Rupiah. (ii) A short-term loan of INR4 million to Private taken out on 30 June 2019 and repayable on 30 June 2020. .8/- The relevant exchange rates are as follows: At 31 December 2018 RM1 = INR2.2 At 30 June 2019 RM1 = INR2 INR1 = 1,500 Rupiah RM1 = 2,570 Rupiah At 31 December 2019 RM1 = INR1.7 INR1 = 1,750 Rupiah RM1 = 2,400 Rupiah Required: (1) Compute the exchange differences, if any, to be recognised in 2019 for the above items and explain their respective treatment in the separate financial statements of: (1) Public (2) Republic (3) Private [6 marks] (i) Public's presentation currency is the Ringgit Malaysia (RM). Explain, stating your reasons, how the above exchange difference in (a) above should be treated in the consolidated financial statements of Public. (5 marks) END OF QUESTION PAPER N BAC305/05 Part A (40 marks) All 10 questions are compulsory and must be attempted. Each question contributes 4 marks. 1. During the last three years Abey Berhad Co has held 300,000 ordinary shares in Bamee Berhad. The issued share capital of Bamee Berhad is 1,000,000 shares totalling RM500,000. The finance director of Abey Berhad is a director of Bamee Berhad Explain how the investment in Bamee Berhad should be treated in the consolidated financial statements of Abey Berhad. 2. Explain whether a subsidiary needs to prepare accounts to the same date as the parent company 3. Public Berhad transferred a machine to 75% owned subsidiary Queen Berhad on 1 May 2018 for RM500,000. The carrying amount of the machine on 1 May 2018 was RM400,000, and on this date the asset was estimated to have four years of useful life left. Prepare the journal entries in respect of the transfer. Explain the consolidation adjustment needed for unrealised profit arisen from trading of goods. 5. Public Berhad owns 75% of the equity shares in Bell Berhad. At 31 July 2018, the inventory of Public Berhad was valued at RM420,000 and included goods costing RM60,000 that it had purchased from Bell at cost plus 20% mark up. At 31 July 2018, inventories were valued at RM445,000 in the consolidated statement of financial position of the Public Group. At 31 July 2018, provide the inventory figure in the statement of financial position of Bell. 6. Public Berhad owns 75% of the ordinary share capital of its subsidiary Willy Berhad. At the group's year end, 28 February 2019, Public Berhad's payables include RM3,600 in respect of inventories sold to it by Willy Berhad. Williy Berhad's receivables include RM6,700 in respect of inventories sold to Public Berhad. Two days before the year end Public Berhad sent a payment of RM3, 100 to Willy Berhad that was not recorded by the latter until 2 days after the year end. Calculate the in-transit item should be dealt with in the consolidated statement of financial position at 28 February 2019. ...3/- 3 BAC305/05 7 8. 9. Public Berhad owns 75% of the issued equity share capital of Kelly Berhad. At the year end, Kelly Berhad held inventories valued at RM160,000 and Public Berhad held inventories valued at RM90,000. The inventories held by Kelly Berhad included RM20,000 of goods purchased from Public Berhad at a profit margin of 30%. There was also inventories in transit between the 2 companies which Public sold to Kelly earlier this amounted to a further RM10,000 at selling price. Calculate the value that the inventories should appear in the consolidated statement of financial position. Where the purchase price of an acquisition is less than the aggregate fair value of the net assets acquired, explain the accounting treatments for the difference as required by MFRS 3, Business Combination. Public Berhad acquired 90% of the ordinary shares in Queen Berhad on 1 August 2018 at a cost of RM480,000. On that date the net assets of Queen Berhad amounted to RM500,000. In the year ended 30 June 2019, Public Berhad reported a profit of RM210,000 and Queen Berhad of RM120,000. Trading conditions indicated that the goodwill in Queen Berhad may be impaired and a review found that it was indeed impaired by 50%. It is Public Berhad group policy to measure the non-controlling interest as a percentage of net assets. By assuming the revenue and expenses accrued evenly throughout the year, calculate the profit for the year ended 30 June 2019 before allocation to the group owners and the non-controlling interest Explain the following statements regarding group accounting which is/are correct Only the group's share of the assets of a subsidiary is reflected in the consolidated statement of financial position. An investment in an associate is initially reflected in the consolidated statement of financial position at its cost. III The value of share capital in a consolidated statement of financial position will include the share capital of both the investor and the investee IV The value of share capital in a consolidated statement of financial position will include the share capital of the investor only. V Where a group comprises a parent company and an investee over which the parent has significant influence, consolidated accounts must be prepared in accordance to acquisition method. 10. - = ...4/- BAC305/05 Part B (60 marks) All 3 questions are compulsory and must be attempted. Each question contributes 20 marks. Question 1 Maxi Berhad offered 1 million ordinary shares for issue to public on 1 January 2018 having face value of RM1 each at an issue price of RM1.50 per share. Maxi Berhad requires the equity injection to finance a new project. The minimum amount of subscription necessary for the project is RM1,250,000. As per the terms of the issue of shares, RM1.50 per share was to be received in full from the applicants on 30 November 2018 A total amount of RM3,000,000 was received. The oversubscription of RM1,500,000 was returned to unsuccessful applicants on 20 December 2018. On 31 January 2020, Maxi Berhad declared a 3 for 2 bonus issue. Extract of Maxi Berhad's balance sheet prior to issuance of bonus shares is as follows: RM Ordinary Share Capital 1,500,000 Revaluation Reserve 1,500,000 Retained Profits 5,000,000 8,000,000 Required: (a) State the journal entries required to account for the above transactions and prepare extract of the balance sheet after bonus issue. [14 marks) (b) Explain the advantages and disadvantages of bonus issues. [6 marks) BAC305/05 Question 2 North Berhad, a public limited company, acquired 80% ordinary shares in East Berhad on 1 January 2017 for RM8,640,000 when the accumulated retained earnings of East Berhad were RM2,000,000. North Berhad also acquired one third (1/3) of the issued ordinary share capital in West Berhad on 1 July 2019 for RM4,000,000 Balance sheets of the three companies as at 31 December 2019 are given below: North East West Non-current assets RM'000 RM'000 RM'000 Freehold property 10,000 1,000 Plant and equipment 6,100 7,400 8,550 Investments in companies 14,000 1,820 510 30,100 10,220 9,060 Current assets Inventories 1,660 680 600 Accounts receivable 1,040 580 Cash and cash equivalents 480 100 150 3,180 1,360 1,050 Current liabilities Accounts payable 1,240 2,120 750 Taxation 440 500 60 1,680 2,620 810 300 Net current assets 1,500 31,600 (1,260) 8,960 240 9,300 500 Financed by Ordinary shares capital 10,000 3,600 3,000 Retained profit b/f 12,000 3,260 4,500 Profit for the year 8,600 1,600 1,800 Non-current Liabilities 8% Loan note 1,000 10% Bonds 31,600 8,960 9,300 Additional information: (1) On February 2017, East declared and paid a net dividend of RM350,000 for the year 2016. North credited its income statement with its share of the dividend received (2) On 1 January 2019, North acquired 60% of the 10% bonds issued by East paying RM300,000 ...6/- BAC305/05 (3) On 1 January 2017, a piece of land of East had a fair value of RM240,000 in excess of its book value. The value this land had not changed since acquisition (4) During 2019, North sold goods to East for RM260,000. Two thirds of these goods were still in inventory of East at 31 December 2019. In November 2019 North sold inventory for RM130,000 to West and West has not sold any of these inventory. North transfers inventory to East and West at a mark up of 30% on cost (5) As at the end of the year, East had not provided for the second half-year interest on the 10% Bonds. (6) Included in accounts payable of East was an amount of RM70,000 due to North. However, North has factored without recourse, RM40,000 of these accounts receivable. (7) The group accounting policy for goodwill is to write it off on a straight-line basis over a period of five years with a proportionate charge where it arises part way through an accounting period. The amortisation of goodwill has not been recorded in the book yet. (8) Assume that income and expenses accrue evenly throughout the year. Required: (a) Prepare a consolidated statement of financial position for North Berhad and its subsidiary as at 31 December 2019, incorporating its associate in accordance with MFRS 128; (b) Lay out workings for (0) Goodwill (ii) Group retained earnings Minority interest; and (iv) Investment in associates. [20 marks) ...71- Question 3 (a) Tobaco Berhad, with the Ringgit Malaysia as its functional currency, purchases plant from a foreign entity for $18 million on 31 May 2019 when the exchange rate was $2 to RM1. The entity also sells goods to a foreign customer for $10.5million on 30 September 2019, when the exchange rate was $1.75 to RM1. At the entity's year end of 31 December 2019, both amounts are still outstanding and have not been paid. The closing exchange rate was $1.5 to RM1. Required: Explain the accounting treatment for both sale and purchases transactions for Tobacco Berhad [5 marks) (b) Truly Berhad has a 100%-owned foreign subsidiary, which has a carrying value at a cost of RM25 million. It sells the subsidiary on 31 December 2019 for $45million. As at 31 December 2019, the credit balance on the exchange reserve, which relates to this subsidiary, was RM6 million. The functional currency of the entity is the Ringgit Malaysia and the exchange rate on 31 December 2019 is RM1 to $1.5. The net asset value of the subsidiary at the date of disposal was RM28 million. Required: Explain the accounting treatment for the disposal transaction. [4 marks) (c) Public Bhd, a company incorporated in Malaysia, whose functional currency is the Ringgit Malaysia (RM) and whose year ends on 31 December, has two overseas subsidiaries. Public is preparing to finalise its financial statements for the year ended 31 December 2019 and has the following inter-company accounts with the two subsidiaries: (0) A loan of INR8 million to Republic, a company in India whose functional currency is the Indian Rupee (INR), which has been outstanding since the acquisition of Republic in 2015 and which it does not regard as repayable in the foreseeable future. (ii) A trade receivables account balance amounting to RM300,000 from Private, a foreign company whose functional currency is the Rupiah, held in the books of Private at 725 million Rupiah. (ii) A short-term loan of INR4 million to Private taken out on 30 June 2019 and repayable on 30 June 2020. .8/- The relevant exchange rates are as follows: At 31 December 2018 RM1 = INR2.2 At 30 June 2019 RM1 = INR2 INR1 = 1,500 Rupiah RM1 = 2,570 Rupiah At 31 December 2019 RM1 = INR1.7 INR1 = 1,750 Rupiah RM1 = 2,400 Rupiah Required: (1) Compute the exchange differences, if any, to be recognised in 2019 for the above items and explain their respective treatment in the separate financial statements of: (1) Public (2) Republic (3) Private [6 marks] (i) Public's presentation currency is the Ringgit Malaysia (RM). Explain, stating your reasons, how the above exchange difference in (a) above should be treated in the consolidated financial statements of Public. (5 marks) END OF QUESTION PAPER

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Surviving An OSHA Audit A Managent Guide

Authors: Frank R. Spellman

1st Edition

0367579340, 978-0367579340