Question

Natalie Warren is a single woman in her late 20s. She is renting an apartment in the fashionable part of town for $1,300 a month.

Natalie Warren is a single woman in her late 20s. She is renting an apartment in the fashionable part of town for $1,300 a month. After much thought, she's seriously considering buying a condominium for $330,000. She intends to put 20 percent down and expects that closing costs will amount to another $6,000; a commercial bank has agreed to lend her money at the fixed rate of 6 percent on a 15-year mortgage. Natalie would have to pay an annual condominium owner's insurance premium of $590 and property taxes of $1,300 a year (she's now paying renter's insurance of $550 per year). In addition, she estimates that annual maintenance expenses will be about 0.5 percent of the price of the condo (which includes a $30 monthly fee to the property owners' association). Natalie's income puts her in the 24 percent tax bracket (she does not itemize her deductions on her tax returns), and she earns an after-tax rate of return on her investments of around 4 percent. Assume that the standard deduction for a single person is $12,000.

Given the information provided, use Worksheet 5.2 to evaluate and compare Natalie's alternatives of remaining in the apartment or purchasing the condo. (Note: Assume Natalie does not have any security deposit.) Round your answers to the nearest cent.

Annual ownership cost:$ ??

Annual rental cost:$ ??

Working with a friend who is a realtor, Natalie has learned that condos like the one she's thinking of buying are appreciating in value at the rate of 3.5 percent a year and are expected to continue doing so. Would such information affect the rent-or-buy decision made in Question 1? yes or no?

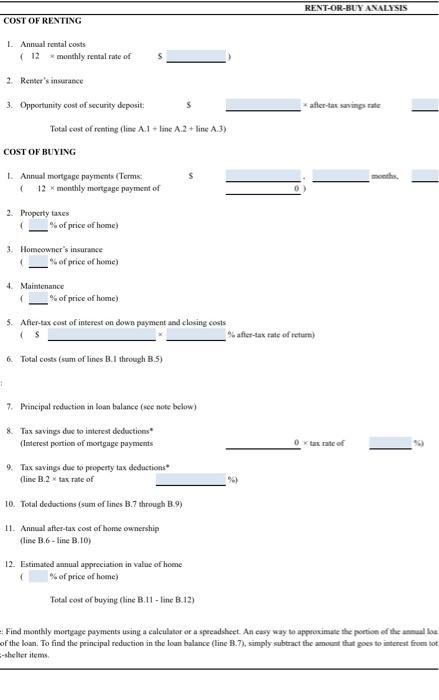

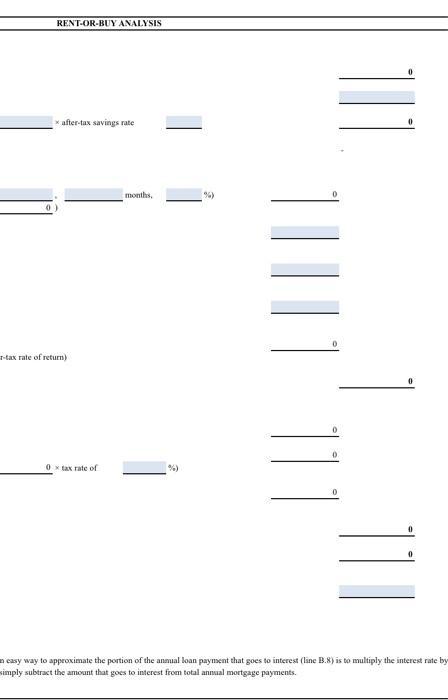

RENT-OR-BUY ANALYSIS COST OF RENTING I. Annual rental costs ( 12 monthly rental rate of 2. Renter's insurance 3. Opportunity cost of security deposit: after-tar savings rate Total cost of renting (line A.I line A.2 + line A.3) COST OF BUYING L. Annual mortgage payments (Terms: ( 12 x monthly mortgage payment of months 2. Property taxes % of price of home) 3. Homeowner's insurance % of price of home) 4. Maintenance % of price of home) 5. After-tax cost of interest on down payment and closing costs % after-tax rate of return) 6. Total costs (sum of lines B.I through B.5) 7. Principal reduction in loan balance (see note below) 8. Tax savings due to interest deductions (Interest portion of mortgage payments Ox tax rate ef 9. Tax savings due to property tax deductions (line B.2 x tax rate of 10. Total deductions (sum of lines B.7 through B.9) 11. Annual after-tax cost of home ownership (line B.6 - line B.10) 12. Estimated annual appreciation in value of home % of price of home) Total cost of buying (line B.11 - line B.12) Find monthly mortgage payments using a calculator or a specadsheet. An casy way to approximate the portion of the annual loa of the loan. To find the principal reduction in the loan balance (line B.7), simply subtract the amount that goes to interest from tot --shelter items.

Step by Step Solution

3.51 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

Annual Ownership Cost 49310 Annual Rental Cost 13750 Annual Ownership Cost Particulars Amount ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Law The Ethical Global and E-Commerce Environment

Authors: Jane Mallor, James Barnes, Thomas Bowers, Arlen Langvardt

15th edition

978-0073524986, 73524980, 978-0071317658