Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Need answer for question 3 and 4 1.Suppose that Jungho and Jungyae enter into a pooling arrangement. Assume that both have the following loss distribution

Need answer for question 3 and 4

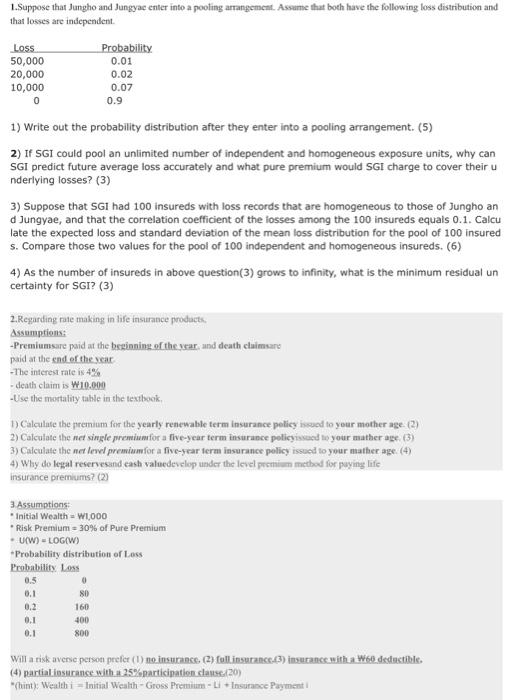

1.Suppose that Jungho and Jungyae enter into a pooling arrangement. Assume that both have the following loss distribution and that losses are independent Loss 50,000 20,000 10,000 0 Probability 0.01 0.02 0.07 0.9 1) Write out the probability distribution after they enter into a pooling arrangement. (5) 2) If SGI could pool an unlimited number of independent and homogeneous exposure units, why can SGI predict future average loss accurately and what pure premium would SGI charge to cover their u nderlying losses? (3) 3) Suppose that SG1 had 100 insureds with loss records that are homogeneous to those of Jungho an d Jungyae, and that the correlation coefficient of the fosses among the 100 insureds equals 0.1. Calcu late the expected loss and standard deviation of the mean loss distribution for the pool of 100 insured s. Compare those two values for the pool of 100 independent and homogeneous insureds. (6) 4) As the number of insureds in above question(3) grows to infinity, what is the minimum residual un certainty for SGI? (3) 2. Regarding rate making in life insurance products, Assumptions: -Premiumsaure paid at the beginning of the year and death claimana paid at the end of the near -The interest rate is 4% - death claim is W10.000 - Use the mortality table in the textbook 1) Calculate the premium for the yearly renewable term Insurance policy red to your mother age (2) 2) Calculate the net single premium for a five-year term insurance policy issued to your mather age. (3) 3) Calculate the nat level premiumfor a five-year ferm insurance policy issued to your mather age (4) 4) Why do legal reservesand cash valuedevelop under the level premium method for paying life insurance premiums? (2) 3. Assumptions "Initial Wealth = W1,000 * Risk Premium = 30% of Pure Premium U(W) - LOG(W) Probability distribution of Loss Probability Loss 0.5 0 0.1 80 0.2 160 0.1 400 0.1 800 Will a risk averse person prefer (1) no insurance (2) fall insurance (3) insurance with a W60 detectible. (4) partialios rance with a 25%participation classe (20) "Chint Wealth i ---Initial Wealth - Gross Premium - Li + Insurance Payment Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis And Portfolio Management

Authors: Frank K. Reilly, Keith C. Brown

6th Edition

003025809X, 978-3540014386