Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need answers for 1 - 5. a full explanation isn't necessary, just general sentences and simple explanations. MICRO CASE 1: ALLOWANCE FOR UNCOLLECTIBLE ACCOUNTS You

need answers for 1 - 5. a full explanation isn't necessary, just general sentences and simple explanations.

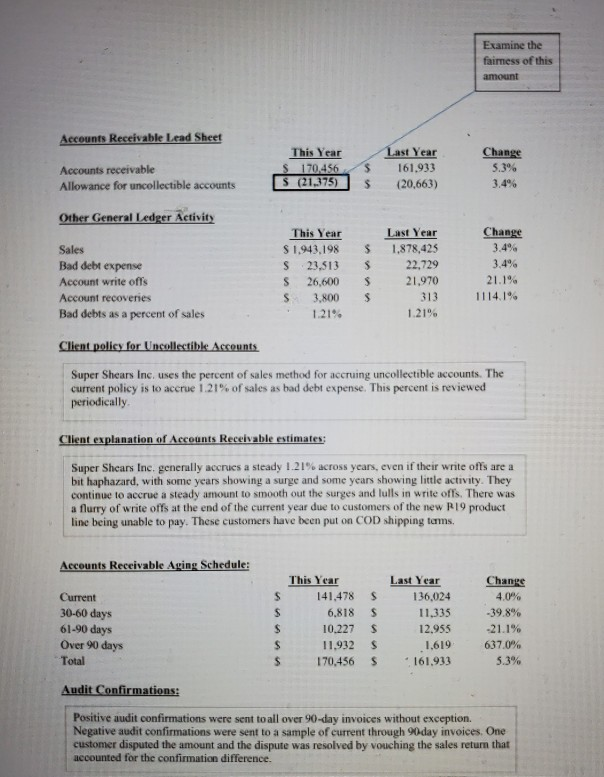

MICRO CASE 1: ALLOWANCE FOR UNCOLLECTIBLE ACCOUNTS You have been assigned to audit a routine management estimate: the allowance for uncollectible accounts. The client has provided the lead sheet, and a member of your audit staff, who was pulled to work on another job, has completed the audit program and gathered considerable evidence regarding the estimate. Your job is to review the evidence and conclude about the reasonableness of the client's estimate. Prior to reviewing the evidence, refresh yourself on how the estimate works by looking over the t-account and journal entries provided in Exhibit A. If this is not enough to help you remember the accounting for bad debts, stop and consult your intermediate textbook or other resources. After all, it is your job to ensure that the client's financial statements are presented in accordance with GAAP, so you must be familiar with current GAAP to perform the audit. Once you have completed your review, answer the pre-requisite questions in Exhibit A. You can check your answers by using Exhibit E to make sure your understanding is correct. You are now ready to proceed to Exhibit B to review the lead sheet, a listing of the balances under audit, and the evidence gathered. Required 1. Identify the evidence that supports the estimate. What facts, tests, or balances indicate that management's accrual is reasonable? That is what evidence supports the accrual? Defend your choices. 2. Identify the evidence that contradicts the estimate. What facts, tests, or balances indicate that the accrual may not be reasonable? That is, what evidence is "disconfirming," indicating that an audit adjustment may be needed? Defend your choices. 3. Identify the irrelevant evidence (neither supports nor contradicts the estimate). What facts, tests, or balances are irrelevant or not helpful in determining the reasonableness of the allowance for uncollectible accounts? Defend your choices. 4. Balance the persuasiveness of the supporting evidence against the persuasiveness of the contradictory evidence. Overall, rate the reasonableness of management's estimate on a scale of 0-10, with 10 - very reasonable and 0 = not reasonable at all. Defend your rating. 5. What other evidence would you gather, if any? Examine the faimess of this amount Accounts Receivable Lead Sheet Accounts receivable Allowance for uncollectible accounts This Year $ 170,456 S (21,375) S $ Last Year 161.933 (20,663) Change 5.3% 3.4% Other General Ledger Activity Change $ Sales Bad debt expense Account write offs Account recoveries Bad debts as a percent of sales This Year $ 1.943.198 S 23,513 S 26,600 $ 3.800 1.21% Last Year 1,878,425 22.729 21.970 313 1.21% $ 21.1% 1114.1% Client policy for Uncollectible Accounts Super Shears Inc, uses the percent of sales method for accruing uncollectible accounts. The current policy is to accrue 1.21% of sales as bad debt expense. This percent is reviewed periodically Client explanation of Accounts Receivable estimates: Super Shears Inc, generally accres a steady 1.21% across years, even if their write offs are a bit haphazard, with some years showing a surge and some years showing little activity. They continue to accrue a steady amount to smooth out the surges and lulls in write ofls. There was a flurry of write offs at the end of the current year due to customers of the new R19 product line being unable to pay. These customers have been put on COD shipping terms. Accounts Receivable Aging Schedule: Current 30-60 days 61-90 days Over 90 days Total This Year 141,478 6.818 10.227 11.932 170,456 S 5 S S S Last Year 136,024 11,335 12,955 . 1.619 161.933 Change 4.0% -39.8% -21.1% 637.0% 5.3% Audit Confirmations: Positive audit confirmations were sent to all over 90-day invoices without exception. Negative audit confirmations were sent to a sample of current through 90day invoices. One customer disputed the amount and the dispute was resolved by vouching the sales return that accounted for the confirmation difference. MICRO CASE 1: ALLOWANCE FOR UNCOLLECTIBLE ACCOUNTS You have been assigned to audit a routine management estimate: the allowance for uncollectible accounts. The client has provided the lead sheet, and a member of your audit staff, who was pulled to work on another job, has completed the audit program and gathered considerable evidence regarding the estimate. Your job is to review the evidence and conclude about the reasonableness of the client's estimate. Prior to reviewing the evidence, refresh yourself on how the estimate works by looking over the t-account and journal entries provided in Exhibit A. If this is not enough to help you remember the accounting for bad debts, stop and consult your intermediate textbook or other resources. After all, it is your job to ensure that the client's financial statements are presented in accordance with GAAP, so you must be familiar with current GAAP to perform the audit. Once you have completed your review, answer the pre-requisite questions in Exhibit A. You can check your answers by using Exhibit E to make sure your understanding is correct. You are now ready to proceed to Exhibit B to review the lead sheet, a listing of the balances under audit, and the evidence gathered. Required 1. Identify the evidence that supports the estimate. What facts, tests, or balances indicate that management's accrual is reasonable? That is what evidence supports the accrual? Defend your choices. 2. Identify the evidence that contradicts the estimate. What facts, tests, or balances indicate that the accrual may not be reasonable? That is, what evidence is "disconfirming," indicating that an audit adjustment may be needed? Defend your choices. 3. Identify the irrelevant evidence (neither supports nor contradicts the estimate). What facts, tests, or balances are irrelevant or not helpful in determining the reasonableness of the allowance for uncollectible accounts? Defend your choices. 4. Balance the persuasiveness of the supporting evidence against the persuasiveness of the contradictory evidence. Overall, rate the reasonableness of management's estimate on a scale of 0-10, with 10 - very reasonable and 0 = not reasonable at all. Defend your rating. 5. What other evidence would you gather, if any? Examine the faimess of this amount Accounts Receivable Lead Sheet Accounts receivable Allowance for uncollectible accounts This Year $ 170,456 S (21,375) S $ Last Year 161.933 (20,663) Change 5.3% 3.4% Other General Ledger Activity Change $ Sales Bad debt expense Account write offs Account recoveries Bad debts as a percent of sales This Year $ 1.943.198 S 23,513 S 26,600 $ 3.800 1.21% Last Year 1,878,425 22.729 21.970 313 1.21% $ 21.1% 1114.1% Client policy for Uncollectible Accounts Super Shears Inc, uses the percent of sales method for accruing uncollectible accounts. The current policy is to accrue 1.21% of sales as bad debt expense. This percent is reviewed periodically Client explanation of Accounts Receivable estimates: Super Shears Inc, generally accres a steady 1.21% across years, even if their write offs are a bit haphazard, with some years showing a surge and some years showing little activity. They continue to accrue a steady amount to smooth out the surges and lulls in write ofls. There was a flurry of write offs at the end of the current year due to customers of the new R19 product line being unable to pay. These customers have been put on COD shipping terms. Accounts Receivable Aging Schedule: Current 30-60 days 61-90 days Over 90 days Total This Year 141,478 6.818 10.227 11.932 170,456 S 5 S S S Last Year 136,024 11,335 12,955 . 1.619 161.933 Change 4.0% -39.8% -21.1% 637.0% 5.3% Audit Confirmations: Positive audit confirmations were sent to all over 90-day invoices without exception. Negative audit confirmations were sent to a sample of current through 90day invoices. One customer disputed the amount and the dispute was resolved by vouching the sales return that accounted for the confirmation differenceStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Journey Into Auditing Culture

Authors: Grant Thornton United Kingdom, Susan Jex, Eddie J. Best

1st Edition

1634540565, 978-1634540568