Need calculation details. Thank you

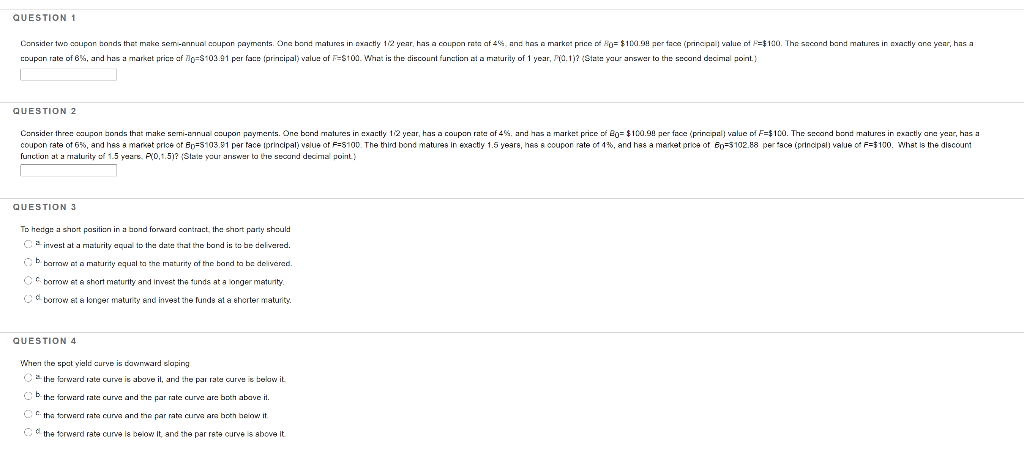

QUESTION 1 Consider two coupon hands that make semi-annual coupon payments. One band matures in exactly 12 year, has a coupon rate at 45, and has a market price of Ro= $10.99 per face principal value of F=$100. The second band matures in exactly are year, has a coupon rate of 6%, and has a market price of Bo=S 03.91 per face principal) value of P=S100. What is the discount function at a maturity of 1 year, P.1)? (State your answer to the second decimal point) QUESTION 2 Consider three caupon bonds that make semi-annual coupon payments. One band matures in exactly 1/2 year, has a coupon rate of 45, and has a market price of Bo= $100.99 per face principal value of F=$100. The second bond matures in exactly ane year, has a coupon rate of 6%, and has a marcat price of Bp=$103.81 per face principal value of $100. The third bond matures in exactly 1.5 years, has a coupon rate of 1%, and has a market price of En=$102.88 per face principal value of P=$100. What is the discount function at a maturity of 1.5 years, P10,1.51? (State your answer to the second decimal point) QUESTION 3 To henge a short position in a bond forward contract, the short party should invest at a maturity equal to the date that the bard is to be delivered. borrow not a maturity equal to the maturity of the band to be delivered Oborrow at a short maturity and invest the funds at a longer maturity Odborrow at a longer maturity and invest the funds at a shorter maturity: QUESTION 4 When the spat yield curve is daard sloping 2. the forward rate curveis abave it, and the par rate curve is below it b. the forward rate curve and the par rate curve are both abave it. tha forward rate curve and the par rate curve are both below it Od the forward rate curve is below it, and the parrete curve is above It QUESTION 1 Consider two coupon hands that make semi-annual coupon payments. One band matures in exactly 12 year, has a coupon rate at 45, and has a market price of Ro= $10.99 per face principal value of F=$100. The second band matures in exactly are year, has a coupon rate of 6%, and has a market price of Bo=S 03.91 per face principal) value of P=S100. What is the discount function at a maturity of 1 year, P.1)? (State your answer to the second decimal point) QUESTION 2 Consider three caupon bonds that make semi-annual coupon payments. One band matures in exactly 1/2 year, has a coupon rate of 45, and has a market price of Bo= $100.99 per face principal value of F=$100. The second bond matures in exactly ane year, has a coupon rate of 6%, and has a marcat price of Bp=$103.81 per face principal value of $100. The third bond matures in exactly 1.5 years, has a coupon rate of 1%, and has a market price of En=$102.88 per face principal value of P=$100. What is the discount function at a maturity of 1.5 years, P10,1.51? (State your answer to the second decimal point) QUESTION 3 To henge a short position in a bond forward contract, the short party should invest at a maturity equal to the date that the bard is to be delivered. borrow not a maturity equal to the maturity of the band to be delivered Oborrow at a short maturity and invest the funds at a longer maturity Odborrow at a longer maturity and invest the funds at a shorter maturity: QUESTION 4 When the spat yield curve is daard sloping 2. the forward rate curveis abave it, and the par rate curve is below it b. the forward rate curve and the par rate curve are both abave it. tha forward rate curve and the par rate curve are both below it Od the forward rate curve is below it, and the parrete curve is above It