Answered step by step

Verified Expert Solution

Question

1 Approved Answer

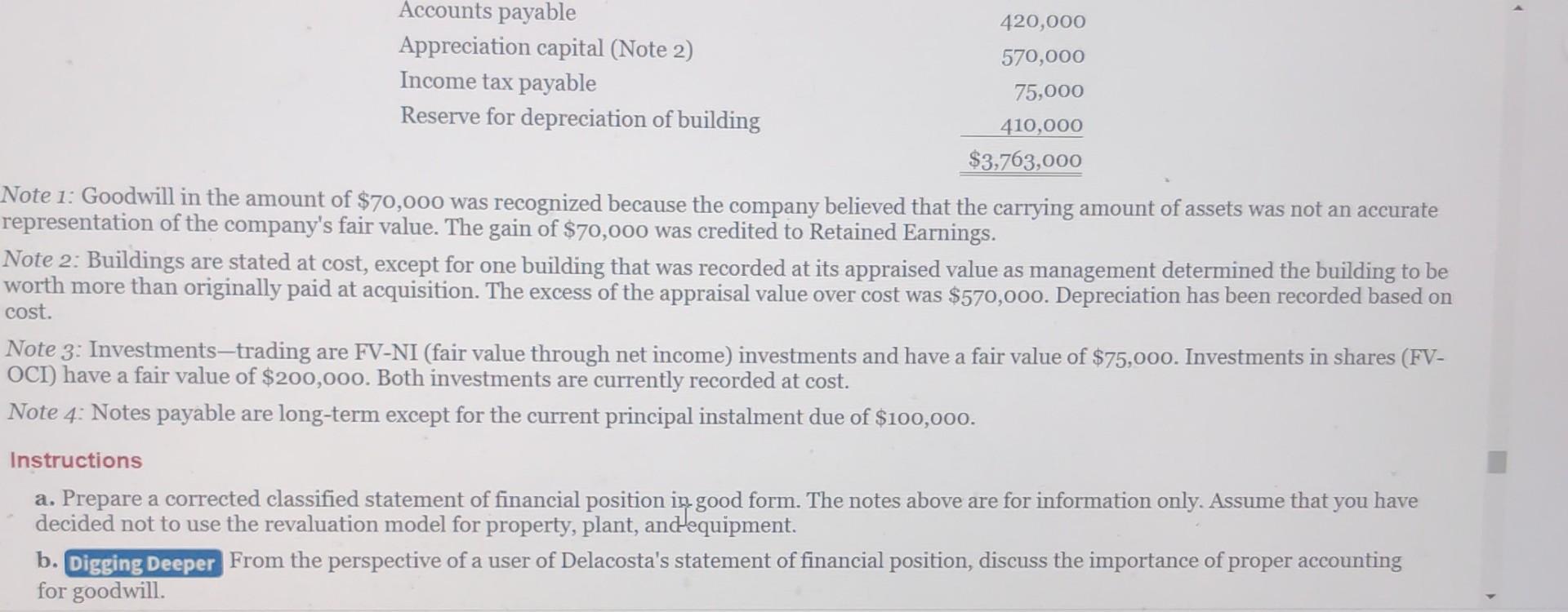

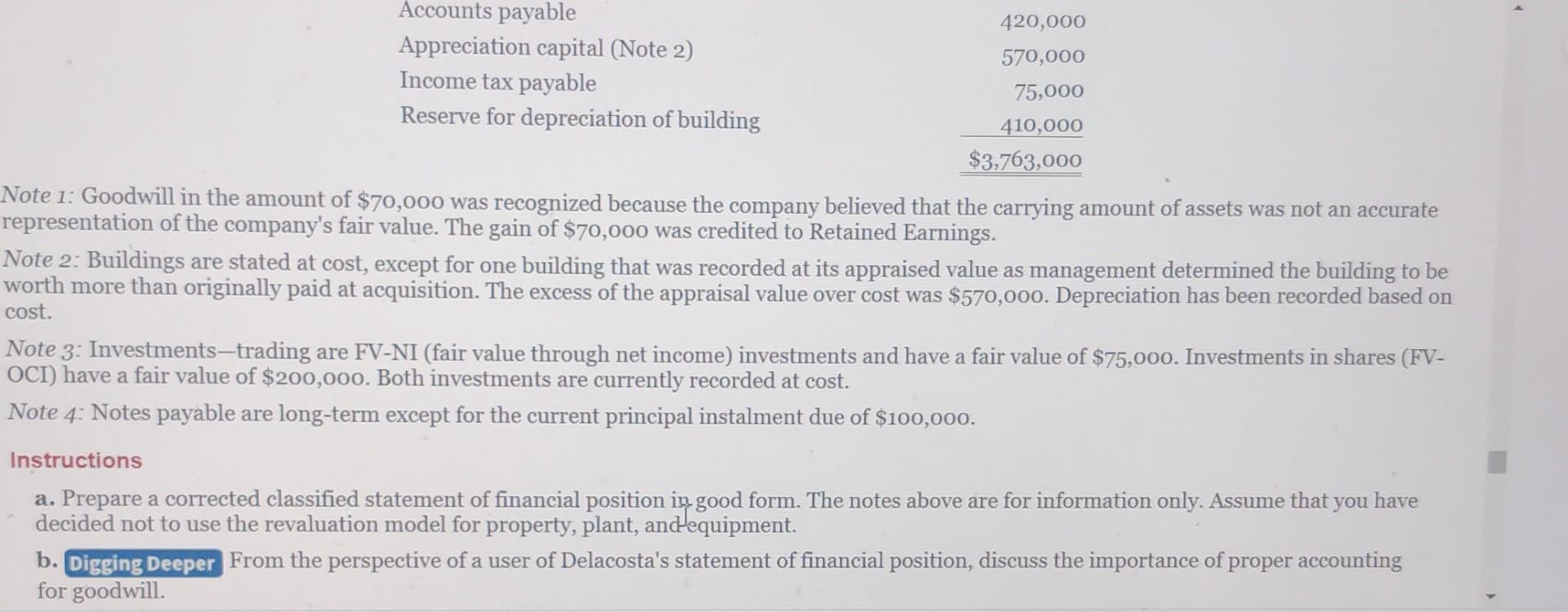

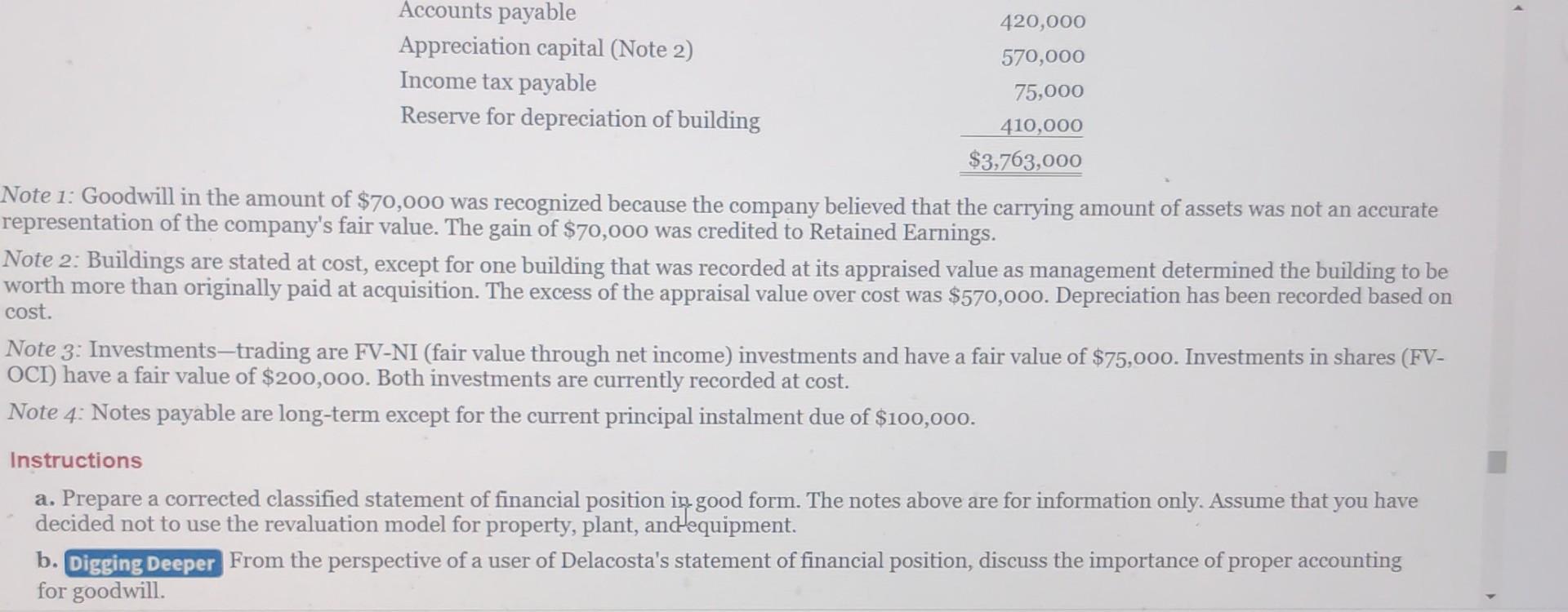

need help in both parts Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note

need help in both parts

Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note 1: Goodwill in the amount of $70,000 was recognized because the company believed that the carrying amount of assets was not an accurate representation of the company's fair value. The gain of $70,000 was credited to Retained Earnings. Note 2: Buildings are stated at cost, except for one building that was recorded at its appraised value as management determined the building to be worth more than originally paid at acquisition. The excess of the appraisal value over cost was $570,000. Depreciation has been recorded based on cost. Note 3: Investments-trading are FV-NI (fair value through net income) investments and have a fair value of $75,000. Investments in shares (FV- OCI) have a fair value of $200,000. Both investments are currently recorded at cost. Note 4: Notes payable are long-term except for the current principal instalment due of $100,000. Instructions a. Prepare a corrected classified statement of financial position in good form. The notes above are for information only. Assume that you have decided not to use the revaluation model for property, plant, and equipment. b. Digging Deeper From the perspective of a user of Delacosta's statement of financial position, discuss the importance of proper accounting for goodwill. 4 Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note 1: Goodwill in the amount of $70,000 was recognized because the company believed that the carrying amount of assets was not an accurate representation of the company's fair value. The gain of $70,000 was credited to Retained Earnings. Note 2: Buildings are stated at cost, except for one building that was recorded at its appraised value as management determined the building to be worth more than originally paid at acquisition. The excess of the appraisal value over cost was $570,000. Depreciation has been recorded based on cost. Note 3: Investments-trading are FV-NI (fair value through net income) investments and have a fair value of $75,000. Investments in shares (FV- OCI) have a fair value of $200,000. Both investments are currently recorded at cost. Note 4: Notes payable are long-term except for the current principal instalment due of $100,000. Instructions a. Prepare a corrected classified statement of financial position in good form. The notes above are for information only. Assume that you have decided not to use the revaluation model for property, plant, and equipment. b. Digging Deeper From the perspective of a user of Delacosta's statement of financial position, discuss the importance of proper accounting for goodwill. 4 Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note 1: Goodwill in the amount of $70,000 was recognized because the company believed that the carrying amount of assets was not an accurate representation of the company's fair value. The gain of $70,000 was credited to Retained Earnings. Note 2: Buildings are stated at cost, except for one building that was recorded at its appraised value as management determined the building to be worth more than originally paid at acquisition. The excess of the appraisal value over cost was $570,000. Depreciation has been recorded based on cost. Note 3: Investments-trading are FV-NI (fair value through net income) investments and have a fair value of $75,000. Investments in shares (FV- OCI) have a fair value of $200,000. Both investments are currently recorded at cost. Note 4: Notes payable are long-term except for the current principal instalment due of $100,000. Instructions a. Prepare a corrected classified statement of financial position in good form. The notes above are for information only. Assume that you have decided not to use the revaluation model for property, plant, and equipment. b. Digging Deeper From the perspective of a user of Delacosta's statement of financial position, discuss the importance of proper accounting for goodwill. 4 Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note 1: Goodwill in the amount of $70,000 was recognized because the company believed that the carrying amount of assets was not an accurate representation of the company's fair value. The gain of $70,000 was credited to Retained Earnings. Note 2: Buildings are stated at cost, except for one building that was recorded at its appraised value as management determined the building to be worth more than originally paid at acquisition. The excess of the appraisal value over cost was $570,000. Depreciation has been recorded based on cost. Note 3: Investments-trading are FV-NI (fair value through net income) investments and have a fair value of $75,000. Investments in shares (FV- OCI) have a fair value of $200,000. Both investments are currently recorded at cost. Note 4: Notes payable are long-term except for the current principal instalment due of $100,000. Instructions a. Prepare a corrected classified statement of financial position in good form. The notes above are for information only. Assume that you have decided not to use the revaluation model for property, plant, and equipment. b. Digging Deeper From the perspective of a user of Delacosta's statement of financial position, discuss the importance of proper accounting for goodwill. 4 Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note 1: Goodwill in the amount of $70,000 was recognized because the company believed that the carrying amount of assets was not an accurate representation of the company's fair value. The gain of $70,000 was credited to Retained Earnings. Note 2: Buildings are stated at cost, except for one building that was recorded at its appraised value as management determined the building to be worth more than originally paid at acquisition. The excess of the appraisal value over cost was $570,000. Depreciation has been recorded based on cost. Note 3: Investments-trading are FV-NI (fair value through net income) investments and have a fair value of $75,000. Investments in shares (FV- OCI) have a fair value of $200,000. Both investments are currently recorded at cost. Note 4: Notes payable are long-term except for the current principal instalment due of $100,000. Instructions a. Prepare a corrected classified statement of financial position in good form. The notes above are for information only. Assume that you have decided not to use the revaluation model for property, plant, and equipment. b. Digging Deeper From the perspective of a user of Delacosta's statement of financial position, discuss the importance of proper accounting for goodwill. 4 Accounts payable 420,000 Appreciation capital (Note 2) Income tax payable 570,000 75,000 Reserve for depreciation of building 410,000 $3,763,000 Note 1: Goodwill in the amount of $70,000 was recognized because the company believed that the carrying amount of assets was not an accurate representation of the company's fair value. The gain of $70,000 was credited to Retained Earnings. Note 2: Buildings are stated at cost, except for one building that was recorded at its appraised value as management determined the building to be worth more than originally paid at acquisition. The excess of the appraisal value over cost was $570,000. Depreciation has been recorded based on cost. Note 3: Investments-trading are FV-NI (fair value through net income) investments and have a fair value of $75,000. Investments in shares (FV- OCI) have a fair value of $200,000. Both investments are currently recorded at cost. Note 4: Notes payable are long-term except for the current principal instalment due of $100,000. Instructions a. Prepare a corrected classified statement of financial position in good form. The notes above are for information only. Assume that you have decided not to use the revaluation model for property, plant, and equipment. b. Digging Deeper From the perspective of a user of Delacosta's statement of financial position, discuss the importance of proper accounting for goodwill. 4Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Comparative international accounting

Authors: Christopher nobes, Robert parker

9th Edition

273703579, 978-0273703570