Need help on question 4 parts a-c please!

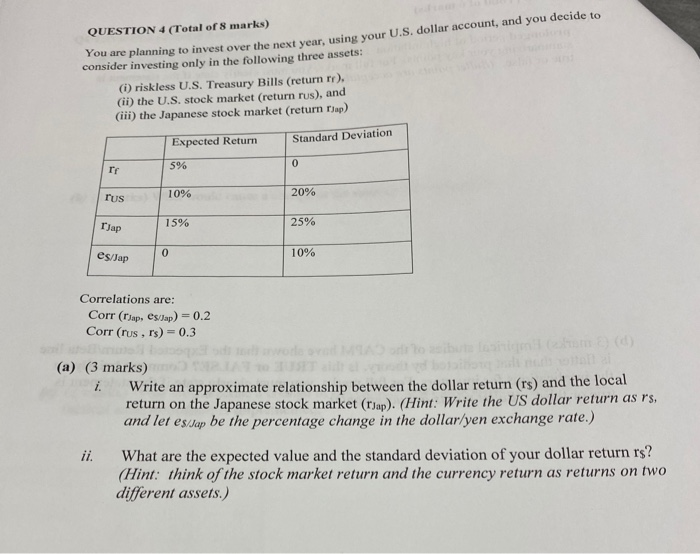

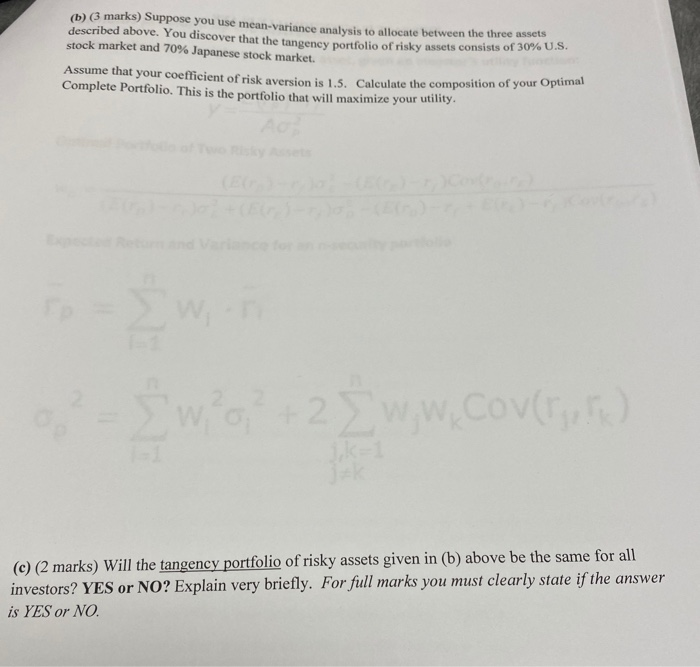

QUESTION 4 (Total of 8 marks) ou are planning to invest over the next year, using your U.S. dollar account, and you decide to consider investing only in the following three assets: (i) riskless U.S. Treasury Bills (return re), (ii) the U.S. stock market (return rus), and (iii) the Japanese stock market (return Tap) Expected Return Standard Deviation rr 59% rus 10% 20% Tap 15% 25% es/Jap 10% Correlations are: Corr (Tap, es lap) = 0.2 Corr (rus, rs) = 0.3 (a) (3 marks) i Write an approximate relationship between the dollar return (rs) and the local return on the Japanese stock market (Cap). (Hint: Write the US dollar return as 'S. and let es.ap be the percentage change in the dollar/yen exchange rate.) il What are the expected value and the standard deviation of your dollar return rs? (Hint: think of the stock market return and the currency return as returns on two different assets.) (b) (3 marks) Suppose you use mean-variance analysis to allocate between the three assets described above. You discover that the over that the tangency portfolio of risky assets consists of 30% U.S. stock market and 70% Japanese stock market. Assume that your coefficient of riskeri Calelate the composition of your op Complete Portfolio. This is the portfolio that will maximize your utility. (c) (2 marks) Will the tangency portfolio of risky assets given in (b) above be the same for all investors? YES or NO? Explain very briefly. For full marks you must clearly state if the answer is YES or NO. QUESTION 4 (Total of 8 marks) ou are planning to invest over the next year, using your U.S. dollar account, and you decide to consider investing only in the following three assets: (i) riskless U.S. Treasury Bills (return re), (ii) the U.S. stock market (return rus), and (iii) the Japanese stock market (return Tap) Expected Return Standard Deviation rr 59% rus 10% 20% Tap 15% 25% es/Jap 10% Correlations are: Corr (Tap, es lap) = 0.2 Corr (rus, rs) = 0.3 (a) (3 marks) i Write an approximate relationship between the dollar return (rs) and the local return on the Japanese stock market (Cap). (Hint: Write the US dollar return as 'S. and let es.ap be the percentage change in the dollar/yen exchange rate.) il What are the expected value and the standard deviation of your dollar return rs? (Hint: think of the stock market return and the currency return as returns on two different assets.) (b) (3 marks) Suppose you use mean-variance analysis to allocate between the three assets described above. You discover that the over that the tangency portfolio of risky assets consists of 30% U.S. stock market and 70% Japanese stock market. Assume that your coefficient of riskeri Calelate the composition of your op Complete Portfolio. This is the portfolio that will maximize your utility. (c) (2 marks) Will the tangency portfolio of risky assets given in (b) above be the same for all investors? YES or NO? Explain very briefly. For full marks you must clearly state if the answer is YES or NO