Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need help solving 3 a) b) c) and d) using the info provided below info used to solve posted below unit data for bottling units

need help solving 3 a) b) c) and d) using the info provided below

info used to solve posted below

unit data for bottling

units data blending

the question is on top and all the data to solve is posted below

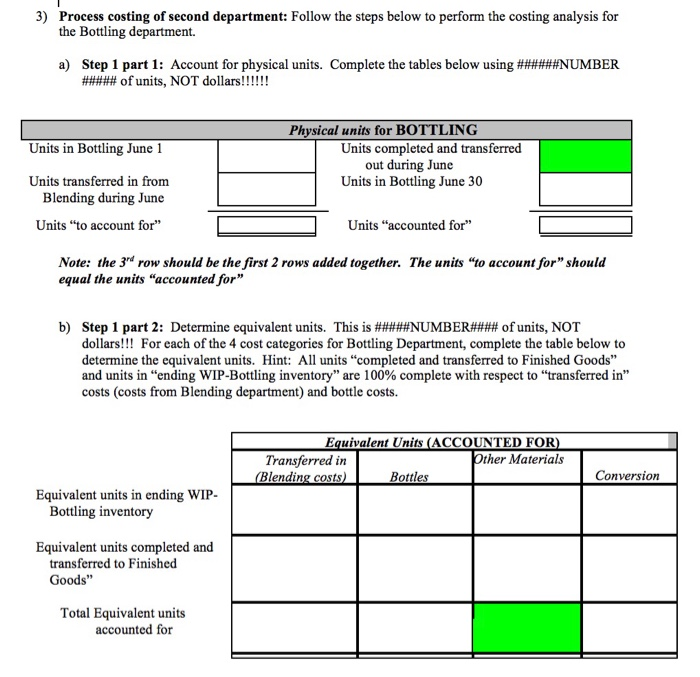

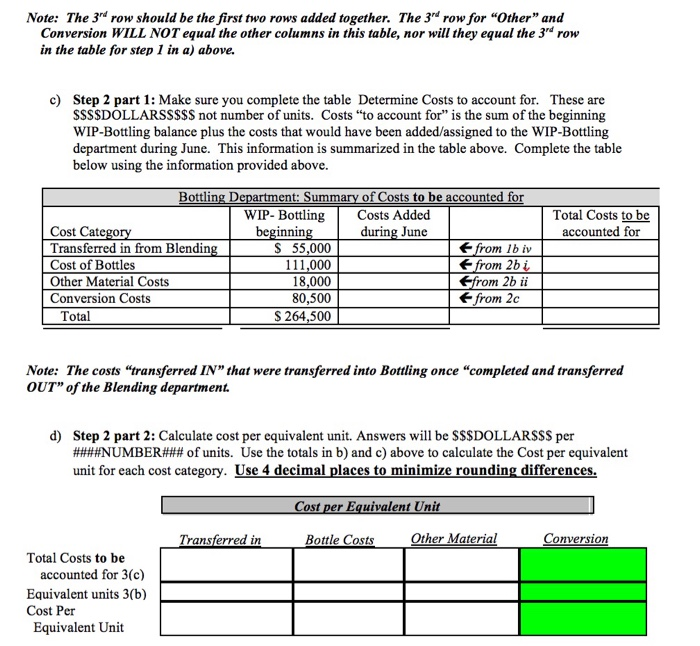

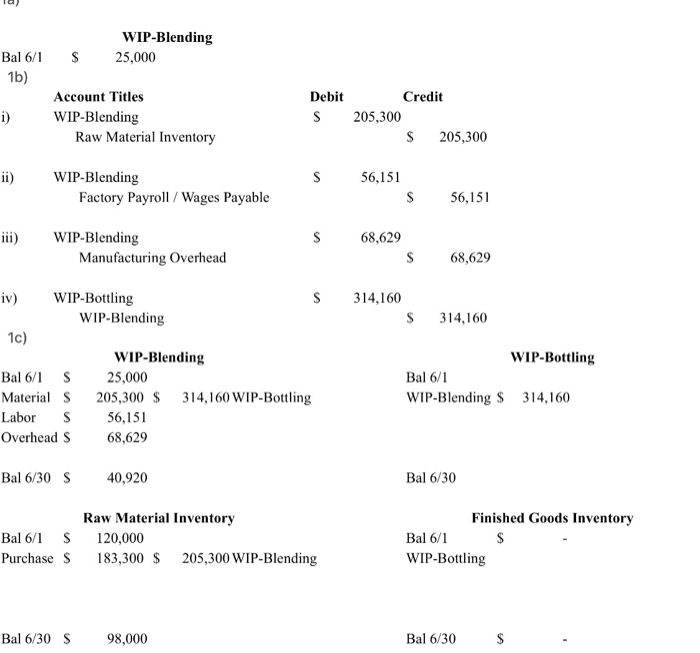

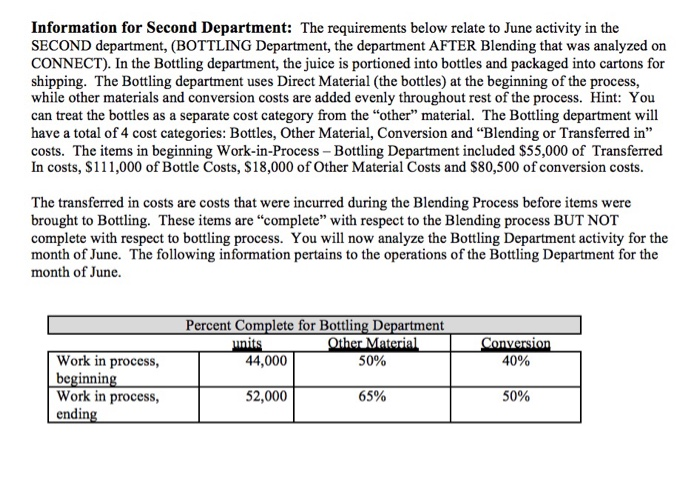

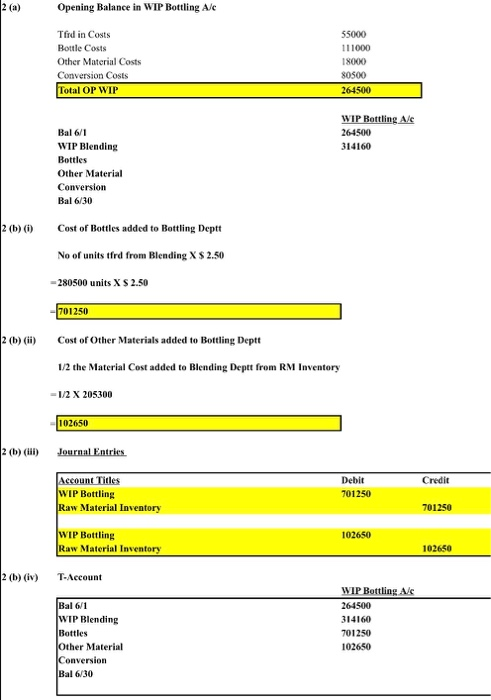

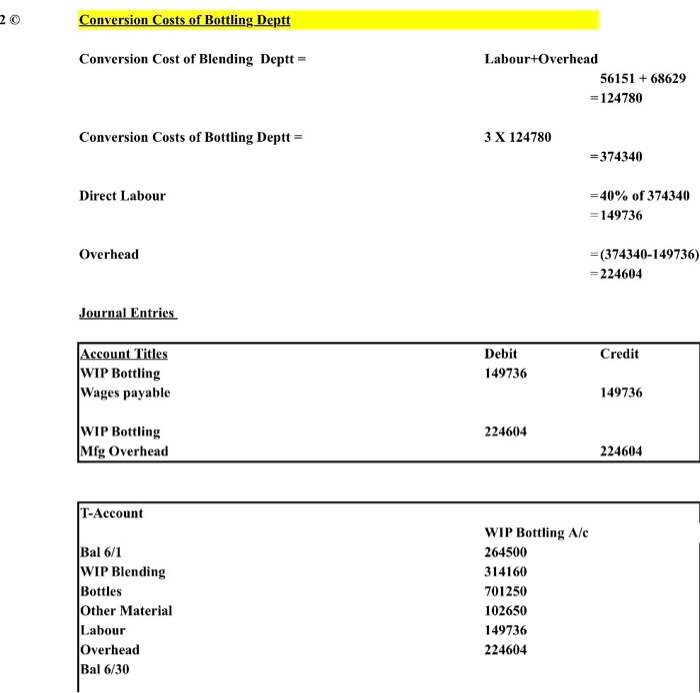

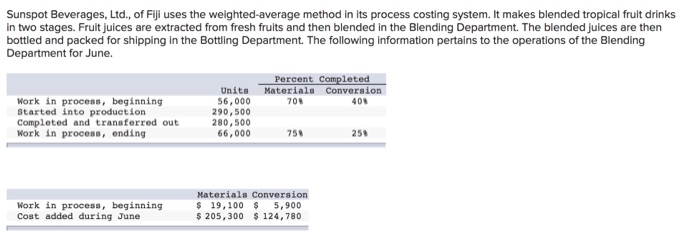

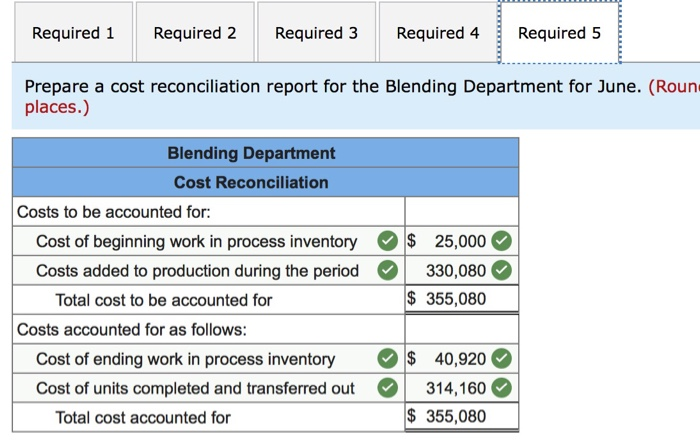

3) Process costing of second department: Follow the steps below to perform the costing analysis for the Bottling department. a) Step 1 part 1: Account for physical units. Complete the tables below using ######NUMBER ##### of units, NOT dollars!!!!!! Units in Bottling June 1 Units transferred in from Blending during June Units "to account for" Physical units for BOTTLING Units completed and transferred out during June Units in Bottling June 30 Units "accounted for" Note: the 3rd row should be the first 2 rows added together. The units "to account for" should equal the units "accounted for" b) Step 1 part 2: Determine equivalent units. This is #####NUMBER#### of units, NOT dollars!!! For each of the 4 cost categories for Bottling Department, complete the table below to determine the equivalent units. Hint: All units "completed and transferred to Finished Goods" and units in "ending WIP-Bottling inventory" are 100% complete with respect to transferred in" costs (costs from Blending department) and bottle costs. Equivalent Units (ACCOUNTED FOR) Transferred in Pther Materials (Blending costs) Bottles Conversion Equivalent units in ending WIP- Bottling inventory Equivalent units completed and transferred to Finished Goods" Total Equivalent units accounted for Note: The 3rd row should be the first two rows added together. The 3rd row for "Other" and Conversion WILL NOT equal the other columns in this table, nor will they equal the 3" row in the table for step 1 in a) above. c) Step 2 part 1: Make sure you complete the table Determine Costs to account for. These are SSS$DOLLARSS$$$ not number of units. Costs to account for" is the sum of the beginning WIP-Bottling balance plus the costs that would have been added/assigned to the WIP-Bottling department during June. This information is summarized in the table above. Complete the table below using the information provided above. Bottling Department: Summary of Costs to be accounted for WIP - Bottling Costs Added Total Costs to be Cost Category beginning during June accounted for Transferred in from Blending $ 55,000 from lb iv Cost of Bottles 111,000 from 2b i Other Material Costs 18,000 Efrom 2b it Conversion Costs 80,500 from 2c Total $ 264,500 Note: The costs "transferred IN that were transferred into Bottling once completed and transferred OUT" of the Blending department. d) Step 2 part 2: Calculate cost per equivalent unit. Answers will be $$$DOLLARSSS per ####NUMBER### of units. Use the totals in b) and c) above to calculate the cost per equivalent unit for each cost category. Use 4 decimal places to minimize rounding differences. Cost per Equivalent Unit Transferred in Bottle Costs Other Material Conversion Total Costs to be accounted for 3(c) Equivalent units 3(b) Cost Per Equivalent Unit WIP-Blending 25,000 $ Bal 6/1 1b) Account Titles WIP-Blending Raw Material Inventory Debit S i) Credit 205,300 $ 205,300 ii) S 56,151 WIP-Blending Factory Payroll/Wages Payable $ 56,151 iii) S 68,629 WIP-Blending Manufacturing Overhead S 68,629 iv) S 314,160 WIP-Bottling WIP-Blending $ 314,160 1c) WIP-Blending 25,000 205,300 $ 314,160 WIP-Bottling 56,151 68,629 WIP-Bottling Bal 6/1 WIP-Blending $ 314,160 Bal 6/1 S Materials Labor S Overhead s Bal 6/30 S 40,920 Bal 6/30 Bal 6/1 S Purchase s Raw Material Inventory 120,000 183,300 $ 205,300 WIP-Blending Finished Goods Inventory Bal 6/1 $ WIP-Bottling Bal 6/30 S 98,000 Bal 6/30 Information for Second Department: The requirements below relate to June activity in the SECOND department, (BOTTLING Department, the department AFTER Blending that was analyzed on CONNECT). In the Bottling department, the juice is portioned into bottles and packaged into cartons for shipping. The Bottling department uses Direct Material (the bottles) at the beginning of the process, while other materials and conversion costs are added evenly throughout rest of the process. Hint: You can treat the bottles as a separate cost category from the "other" material. The Bottling department will have a total of 4 cost categories: Bottles, Other Material, Conversion and "Blending or Transferred in" costs. The items in beginning Work-in-Process - Bottling Department included $55,000 of Transferred In costs, $111,000 of Bottle Costs, $18,000 of Other Material Costs and $80,500 of conversion costs. The transferred in costs are costs that were incurred during the Blending Process before items were brought to Bottling. These items are complete" with respect to the Blending process BUT NOT complete with respect to bottling process. You will now analyze the Bottling Department activity for the month of June. The following information pertains to the operations of the Bottling Department for the month of June. Percent Complete for Bottling Department units Other Material 44,000 50% Conversion 40% Work in process, beginning Work in process, ending 52,000 65% 50% 2 (a) Opening Balance in WIP Bottling A/C Tfrd in Costs Bottle Costs Other Material Costs Conversion Costs Total OP WIP 55000 111000 18000 80500 264500 WIP Bottling Ale 264500 314160 Bal 6/1 WIP Blending Bottles Other Material Conversion Bal 6/30 2 (b) (0) Cost of Bottles added to Bottling Deptt No of units tfrd from Blending X $ 2.50 -280500 units X $ 2.50 701250 2 (0) (0) Cost of Other Materials added to Bottling Deptt 1/2 the Material Cost added to Blending Deptt from RM Inventory -1/2 X 205300 102650 Journal Entries Credit Account Titles WIP Bottling Raw Material Inventory Debit 701250 701250 102650 WIP Bottling Raw Material Inventory 102650 2 (b)(iv) T-Account Bal 6/1 WIP Blending Bottles Other Material Conversion Bal 6/30 WIP Bottling Ale 264500 314160 701250 102650 20 Conversion Costs of Bottling Deptt Conversion Cost of Blending Deptt Labour+Overhead 56151 +68629 = 124780 Conversion Costs of Bottling Deptt = 3 X 124780 = 374340 Direct Labour = 40% of 374340 =149736 Overhead =(374340-149736) = 224604 Journal Entries Credit Account Titles WIP Bottling Wages payable Debit 149736 149736 224604 WIP Bottling Mfg Overhead 224604 T-Account Bal 6/1 WIP Blending Bottles Other Material Labour Overhead Bal 6/30 WIP Bottling A/c 264500 314160 701250 102650 149736 224604 Sunspot Beverages, Ltd., of Fiji uses the weighted-average method in its process costing system. It makes blended tropical fruit drinks in two stages. Fruit juices are extracted from fresh fruits and then blended in the Blending Department. The blended juices are then bottled and packed for shipping in the Bottling Department. The following information pertains to the operations of the Blending Department for June. Percent Completed Materials Conversion 700 400 Work in process, beginning Started into production Completed and transferred out Work in process, ending Units 56,000 290,500 280,500 66,000 750 251 Work in process, beginning Cost added during June Materials Conversion $ 19,100 $ 5,900 $ 205,300 $ 124,780 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's equivalent units of production for materials and conversion in June. Materials Equivalent units of production Conversion 297,000 330,000 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost per equivalent unit for materials and conversion in June. (Round your answers to 2 decimal places.) Cost per equivalent unit Materials Conversion 0.68 $ 0.44 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost of ending work in process inventory for materials, conversion, and in total for June. (Round your intermediate calculations to 2 decimal places.) Materials Conversion Total Cost of ending work in process 33,660 $ 7,260 inventory 40,920 S Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost of units transferred out to the Bottling Department for materials, conversion, and in total for June. (Round your intermediate calculations to 2 decimal places.) Materials Conversion Total Cost of units completed and transferred out $ 190,740 $ 123,420 $ 314,160 Required 1 Required 2 Required 3 Required 4 Required 5 Prepare a cost reconciliation report for the Blending Department for June. (Roun places.) Blending Department Cost Reconciliation Costs to be accounted for: Cost of beginning work in process inventory$ 25,000 Costs added to production during the period 330,080 Total cost to be accounted for $ 355,080 Costs accounted for as follows: Cost of ending work in process inventory $ 40,920 Cost of units completed and transferred out 314,160 Total cost accounted for $ 355,080 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Cost Accounting

Authors: Edward J. Vanderbeck

14th Edition

0324374178, 978-0324374179