need help solving number 4 b) c) d) and 5). use the following info below

post purchase to raw material t-account from 5) and post (COGS) to finished good T-account below from 4d)

questions needed to be solved below

extra info if needed

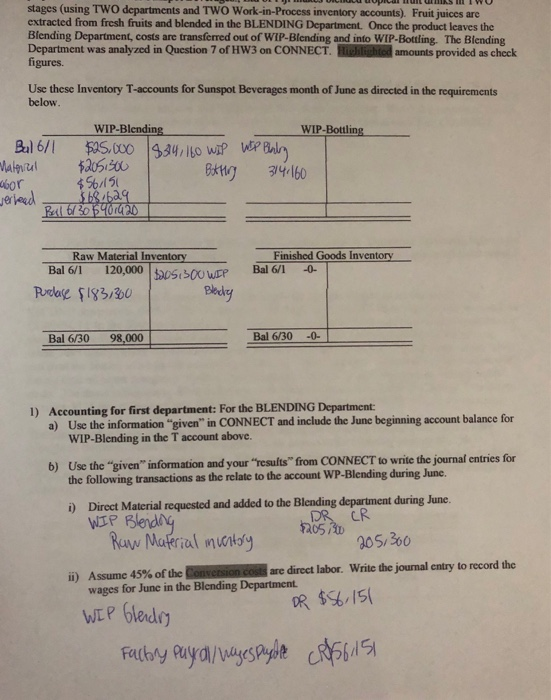

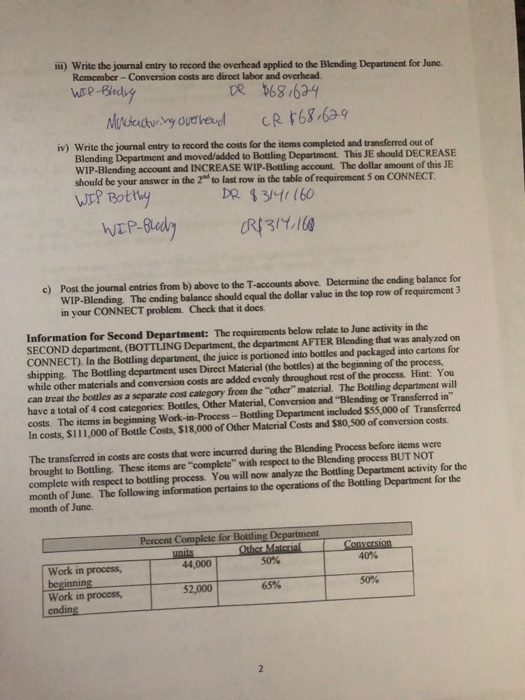

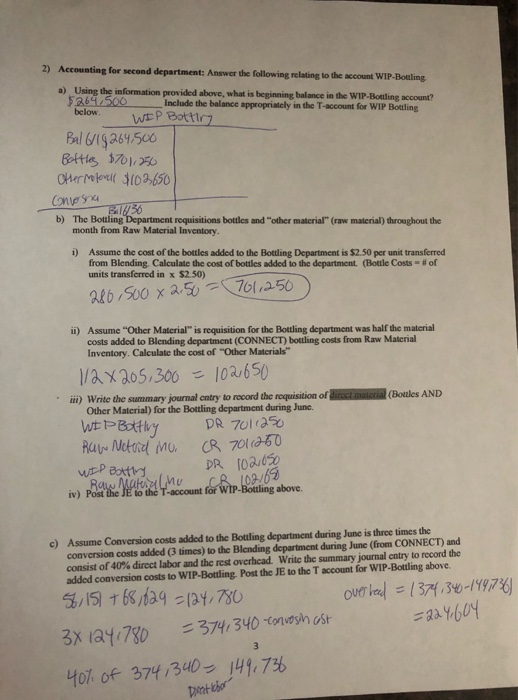

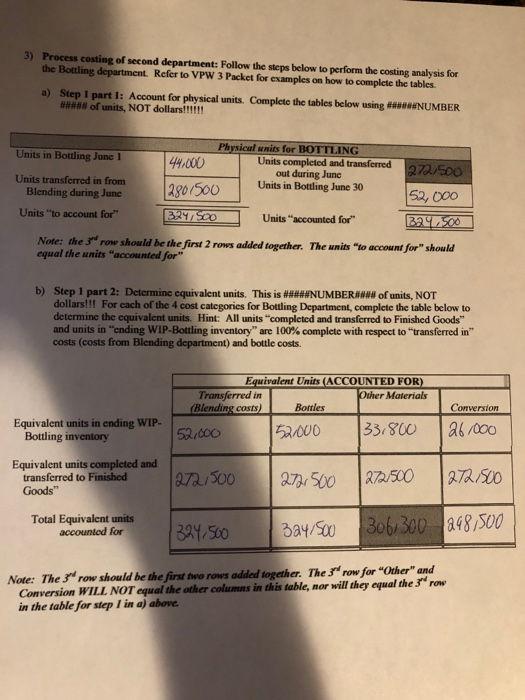

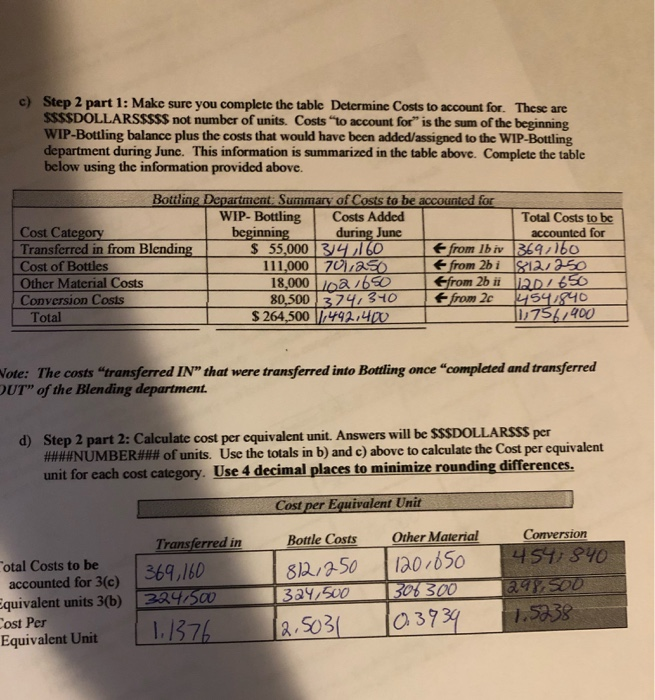

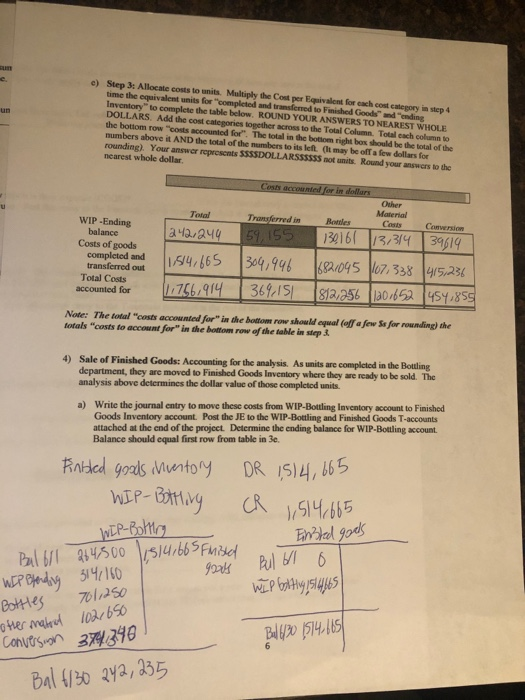

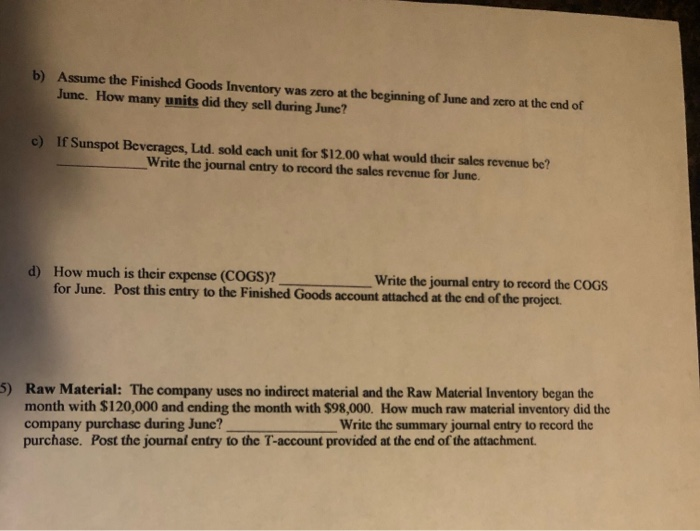

stages (using TWO departments and TWO Work-in-Process inventory accounts). Fruit juices are extracted from fresh fruits and blended in the BLENDING Department. Once the product leaves the Blending Department, costs are transferred out of WIP-Blending and into WIP-Bottling. The Blending Department was analyzed in Question 7 of HW3 on CONNECT. Richlighted amounts provided as check figures. Use these Inventory T-accounts for Sunspot Beverages month of June as directed in the requirements below. WIP-Blending WIP-Bottling Bal 6/1 $25,000 $14, 160 WIP WEP Balry Material $205,300 Bottery 34.160 abor $561151 werlead 3681629 Ball 6/30 540020 Finished Goods Inventory Bal 6/1 -0- Raw Material Inventory Bal 6/1 120,000 | 05 500 Purclase $183,300 Bledky Bal 6/30 98,000 Bal 6/30 -0- 1) Accounting for first department: For the BLENDING Department: a) Use the information "given" in CONNECT and include the June beginning account balance for WIP-Blending in the T account above. b) Use the "given" information and your "results from CONNECT to write the journal entries for the following transactions as the relate to the account WP-Blending during June. i) Direct Material requested and added to the Blending department during June. WIP Blending DR CR Raw Material inventory 52052 205,300 ii) Assume 45% of the Conversion costs are direct labor. Write the journal entry to record the wages for June in the Blending Department DR $56.151 WIP blendry Factory Puyall wayespuble (R56.151 iii) Write the journal entry to record the overhead applied to the Blending Department for June Remember - Conversion costs are direct labor and overhead $681624 WIR Blodry CR $68.629 Muutacturing overnand iv) Write the journal entry to record the costs for the items completed and transferred out of Blending Department and moved/added to Bottling Department. This JE should DECREASE WIP-Blending account and INCREASE WIP-Bottling account. The dollar amount of this JE should be your answer in the 2 to last row in the table of requirements on CONNECT WIP Botthy DR 83141160 WIP-Bledy R$ 314168 c) Post the journal entries from b) above to the T-accounts above. Determine the ending balance for WIP-Blending. The ending balance should equal the dollar value in the top row of requirement 3 in your CONNECT problem. Check that it does. Information for Second Department: The requirements below relate to June activity in the SECOND department, (BOTTLING Department, the department AFTER Blending that was analyzed on CONNECT). In the Bottling department, the juice is portioned into bottles and packaged into cartons for shipping. The Bottling department uses Direct Material (the bottles) at the beginning of the process, while other materials and conversion costs are added evenly throughout rest of the process. Hint: You can treat the bottles as a separate cost category from the other material. The Bottling department will have a total of 4 cost categories: Bottles, Other Material, Conversion and "Blending or Transferred in costs. The items in beginning Work-in-Process - Bottling Department included $55,000 of Transferred In costs, S111,000 of Bottle Costs, $18,000 of Other Material Costs and $80,500 of conversion costs. The transferred in costs are costs that were incurred during the Blending Process before items were brought to Bottling. These items are complete with respect to the Blending process BUT NOT complete with respect to bottling process. You will now analyze the Bottling Department activity for the month of June. The following information pertains to the operations of the Bottling Department for the month of June. Percent Complete for Bottling Department units Other Material 44,000 50% Conversion 40% 50% Work in process, beginning Work in process, ending 52,000 65% 2) Accounting for second department: Answer the following relating to the account WIP-Boutling a) Using the information provided above, what is beginning balance in the WIP-Bottling account? $269,500 Include the balance appropriately in the T-account for WIP Bottling below TP Bott 3 Bal (19 264,500 Bottles $701,250 Other roforall $102650 convosna B1/36 b) The Bottling Department requisitions bottles and other material" (raw material throughout the month from Raw Material Inventory. i) Assume the cost of the bottles added to the Bottling Department is $2.50 per unit transferred from Blending. Calculate the cost of bottles added to the department. (Bottle Costs = # of units transferred in x $2.50) 280,500 x 2.50 = 701,250 ii) Assume "Other Material is requisition for the Bottling department was half the material costs added to Blending department (CONNECT) bottling costs from Raw Material Inventory. Calculate the cost of "Other Materials 1/2x205,300 = 1021650 ) Write the summary journal entry to record the requisition of direct material (Bottles AND Other Material) for the Bottling department during June WE P Battiry DR 7011250 Raw Netvid no WIP Bathry DR Raw Materiche iv) Post the Je to the T-account for WIP-Bottling above. CR 7016260 102,050 CR.102.69 c) Assume Conversion costs added to the Bottling department during Junc is three times the conversion costs added (3 times) to the Blending department during June (from CONNECT) and consist of 40% direct labor and the rest overhead. Write the summary journal entry to record the added conversion costs to WIP-Bottling. Post the JE to the T account for WIP-Bottling above. 56,151 +68,629 = 124,780 overhead = 1374,340-1491736) 3X 1241780 =374,340-convosin cost = 224,604 3 40% of 374,340 - 149,736 Director 3) Process costing of second department: Follow the steps below to perform the costing analysis for the Bottling department. Refer to VPW 3 Packet for examples on how to complete the tables. a) Step 1 part 1: Account for physical units. Complete the tables below using ***NUMBER ### of units, NOT dollars!!!!!! Physical units for BOTTLING Units in Bottling June 1 44.000 Units completed and transferred 272/500 out during June Units transferred in from 12801500 Blending during June Units in Bottling June 30 52,000 Units to account for 324/ DO Units "accounted for" Note: the 3 row should be the first 2 rows added together. The units to account for" should equal the units "accounted for b) Step 1 part 2: Determine equivalent units. This is #WWWNUMBERW of units, NOT dollars!!! For each of the 4 cost categories for Bottling Department, complete the table below to determine the equivalent units. Hint: All units completed and transferred to Finished Goods" and units in "ending WIP-Bottling inventory" are 100% complete with respect to transferred in" costs (costs from Blending department) and bottle costs. Equivalent Units (ACCOUNTED FOR) Transferred in Other Materials (Blending costs) Bortles 52,000 52/000 33.800 Conversion 26/000 Equivalent units in ending WIP- Bottling inventory Equivalent units completed and transferred to Finished Goods" 272/500 272500 272/500 272/500 Total Equivalent units accounted for 324,500 3a4/500 306,300 298,500 Note: The 3 row should be the first two rows added together. The 3 row for "Other" and Conversion WILL NOT equal the other columns in this table, nor will they equal the 3 row in the table for step 1 in a) above. c) Step 2 part 1: Make sure you complete the table Determine Costs to account for. These are SSS$DOLLARSSSSS not number of units. Costs to account for" is the sum of the beginning WIP-Bottling balance plus the costs that would have been added/assigned to the WIP-Bottling department during June. This information is summarized in the table above. Complete the table below using the information provided above. Bottling Department: Summary of Costs to be accounted for WIP- Bottling Costs Added Total Costs to be Cost Category beginning during June accounted for Transferred in from Blending $ 55,000 314,160 from lb iv 369,160 Cost of Bottles 111,000 701,250 from 2bi 8121250 Other Material Costs 18,000 102 1650 Efrom 26 ir 120/650 Conversion Costs 80,500 374,340 from 2c 4541840 Total $ 264,500 1,492.400 11,756,400 Note: The costs "transferred IN" that were transferred into Bottling once "completed and transferred OUT" of the Blending department. d) Step 2 part 2: Calculate cost per equivalent unit. Answers will be SSSDOLLARSSS per ####NUMBER### of units. Use the totals in b) and e) above to calculate the Cost per equivalent unit for each cost category. Use 4 decimal places to minimize rounding differences. Cost per Equivalent Unit Other Material 120.650 Transferred in Cotal Costs to be accounted for 3(C) 369,160 Equivalent units 3(b) 324.500 Cost Per Equivalent Unit 1.1376 Bottle Costs 812 250 324,500 12.5031 Conversion 454,840 04300 7.5238 306 300 10.3934 e un e) Step 3: Allocate costs to units. Multiply the Cost per Equivalent for each cont category in step time the equivalent units for completed and transferred to Finished Goods and ending Inventory to complete the table below. ROUND YOUR ANSWERS TO NEAREST WHOLE DOLLARS. Add the cost categories together across to the Total Column. Total esch column to the bottom row costs accounted for". The total in the bottom right box should be the total of the numbers above it AND the total of the numbers to its left. (lit may be off a few dollars for rounding). Your answer represents SSSSDOLLARSS5555 not units. Round your answers to the nearest whole dollar Total WIP -Ending balance Costs of goods completed and transferred out Total Costs accounted for Transferred in 242,244 59,155 11,514,665 304,996 1.756,914 369,15 Other Material Bandles Costs Comwersion 139161 13,314 39619 821045 07:338 1415,236 812,256 120/652 454.855 Note: The total costs accounted for in the bottom row should equal (offfo Se for rounding the totals "costs to account for in the bottom row of the table in step 4) Sale of Finished Goods: Accounting for the analysis. As units are completed in the Bottling department, they are moved to Finished Goods Inventory where they are ready to be sold. The analysis above determines the dollar value of those completed units. a) Write the journal entry to move these costs from WIP-Botiling Inventory account to Finished Goods Inventory account. Post the JE to the WIP-Bottling and Finished Goods T-accounts attached at the end of the project Determine the ending balance for WIP-Bottling account. Balance should equal first row from table in 3e. Finbled goods inventory WIP- Bottling goods WIP efending 314,160 7011250 other matrol 102,650 DR 1514,665 CR WIP-Bolting 1,514,665 Bulbol 264,500 1,514,665 Finished Einsted goods Bul blo Bottles WIP byltingsluts conversion 374 340 Bult/70 1514.165 Bal6/30 242, 235 b) Assume the Finished Goods Inventory was zero at the beginning of June and zero at the end of Junc. How many units did they sell during June? c) If Sunspot Beverages, Ltd. sold cach unit for $12.00 what would their sales revenue be? Write the journal entry to record the sales revenue for June. d) How much is their expense (COGS)? Write the journal entry to record the COGS for June. Post this entry to the Finished Goods account attached at the end of the project. 5) Raw Material: The company uses no indirect material and the Raw Material Inventory began the month with $120,000 and ending the month with $98,000. How much raw material inventory did the company purchase during June? Write the summary journal entry to record the purchase. Post the journal entry to the T-account provided at the end of the attachment. Sunspot Beverages, Ltd., of Fiji uses the weighted-average method in its process costing system. It makes blended tropical fruit drinks in two stages. Fruit juices are extracted from fresh fruits and then blended in the Blending Department. The blended juices are then bottled and packed for shipping in the Bottling Department. The following information pertains to the operations of the Blending Department for June. Percent Completed Materials Conversion 700 400 Work in process, beginning Started into production Completed and transferred out Work in process, ending Units 56,000 290,500 280,500 66,000 750 251 Work in process, beginning Cost added during June Materials Conversion $ 19,100 $ 5,900 $ 205,300 $ 124,780 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's equivalent units of production for materials and conversion in June. Materials Equivalent units of production Conversion 297,000 330,000 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost per equivalent unit for materials and conversion in June. (Round your answers to 2 decimal places.) Cost per equivalent unit Materials Conversion 0.68 $ 0.44 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost of ending work in process inventory for materials, conversion, and in total for June. (Round your intermediate calculations to 2 decimal places.) Materials Conversion Total Cost of ending work in process 33,660 $ 7,260 inventory 40,920 S Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost of units transferred out to the Bottling Department for materials, conversion, and in total for June. (Round your intermediate calculations to 2 decimal places.) Materials Conversion Total Cost of units completed and transferred out $ 190,740 $ 123,420 $ 314,160 Required 1 Required 2 Required 3 Required 4 Required 5 Prepare a cost reconciliation report for the Blending Department for June. (Roun places.) Blending Department Cost Reconciliation Costs to be accounted for: Cost of beginning work in process inventory$ 25,000 Costs added to production during the period 330,080 Total cost to be accounted for $ 355,080 Costs accounted for as follows: Cost of ending work in process inventory $ 40,920 Cost of units completed and transferred out 314,160 Total cost accounted for $ 355,080 stages (using TWO departments and TWO Work-in-Process inventory accounts). Fruit juices are extracted from fresh fruits and blended in the BLENDING Department. Once the product leaves the Blending Department, costs are transferred out of WIP-Blending and into WIP-Bottling. The Blending Department was analyzed in Question 7 of HW3 on CONNECT. Richlighted amounts provided as check figures. Use these Inventory T-accounts for Sunspot Beverages month of June as directed in the requirements below. WIP-Blending WIP-Bottling Bal 6/1 $25,000 $14, 160 WIP WEP Balry Material $205,300 Bottery 34.160 abor $561151 werlead 3681629 Ball 6/30 540020 Finished Goods Inventory Bal 6/1 -0- Raw Material Inventory Bal 6/1 120,000 | 05 500 Purclase $183,300 Bledky Bal 6/30 98,000 Bal 6/30 -0- 1) Accounting for first department: For the BLENDING Department: a) Use the information "given" in CONNECT and include the June beginning account balance for WIP-Blending in the T account above. b) Use the "given" information and your "results from CONNECT to write the journal entries for the following transactions as the relate to the account WP-Blending during June. i) Direct Material requested and added to the Blending department during June. WIP Blending DR CR Raw Material inventory 52052 205,300 ii) Assume 45% of the Conversion costs are direct labor. Write the journal entry to record the wages for June in the Blending Department DR $56.151 WIP blendry Factory Puyall wayespuble (R56.151 iii) Write the journal entry to record the overhead applied to the Blending Department for June Remember - Conversion costs are direct labor and overhead $681624 WIR Blodry CR $68.629 Muutacturing overnand iv) Write the journal entry to record the costs for the items completed and transferred out of Blending Department and moved/added to Bottling Department. This JE should DECREASE WIP-Blending account and INCREASE WIP-Bottling account. The dollar amount of this JE should be your answer in the 2 to last row in the table of requirements on CONNECT WIP Botthy DR 83141160 WIP-Bledy R$ 314168 c) Post the journal entries from b) above to the T-accounts above. Determine the ending balance for WIP-Blending. The ending balance should equal the dollar value in the top row of requirement 3 in your CONNECT problem. Check that it does. Information for Second Department: The requirements below relate to June activity in the SECOND department, (BOTTLING Department, the department AFTER Blending that was analyzed on CONNECT). In the Bottling department, the juice is portioned into bottles and packaged into cartons for shipping. The Bottling department uses Direct Material (the bottles) at the beginning of the process, while other materials and conversion costs are added evenly throughout rest of the process. Hint: You can treat the bottles as a separate cost category from the other material. The Bottling department will have a total of 4 cost categories: Bottles, Other Material, Conversion and "Blending or Transferred in costs. The items in beginning Work-in-Process - Bottling Department included $55,000 of Transferred In costs, S111,000 of Bottle Costs, $18,000 of Other Material Costs and $80,500 of conversion costs. The transferred in costs are costs that were incurred during the Blending Process before items were brought to Bottling. These items are complete with respect to the Blending process BUT NOT complete with respect to bottling process. You will now analyze the Bottling Department activity for the month of June. The following information pertains to the operations of the Bottling Department for the month of June. Percent Complete for Bottling Department units Other Material 44,000 50% Conversion 40% 50% Work in process, beginning Work in process, ending 52,000 65% 2) Accounting for second department: Answer the following relating to the account WIP-Boutling a) Using the information provided above, what is beginning balance in the WIP-Bottling account? $269,500 Include the balance appropriately in the T-account for WIP Bottling below TP Bott 3 Bal (19 264,500 Bottles $701,250 Other roforall $102650 convosna B1/36 b) The Bottling Department requisitions bottles and other material" (raw material throughout the month from Raw Material Inventory. i) Assume the cost of the bottles added to the Bottling Department is $2.50 per unit transferred from Blending. Calculate the cost of bottles added to the department. (Bottle Costs = # of units transferred in x $2.50) 280,500 x 2.50 = 701,250 ii) Assume "Other Material is requisition for the Bottling department was half the material costs added to Blending department (CONNECT) bottling costs from Raw Material Inventory. Calculate the cost of "Other Materials 1/2x205,300 = 1021650 ) Write the summary journal entry to record the requisition of direct material (Bottles AND Other Material) for the Bottling department during June WE P Battiry DR 7011250 Raw Netvid no WIP Bathry DR Raw Materiche iv) Post the Je to the T-account for WIP-Bottling above. CR 7016260 102,050 CR.102.69 c) Assume Conversion costs added to the Bottling department during Junc is three times the conversion costs added (3 times) to the Blending department during June (from CONNECT) and consist of 40% direct labor and the rest overhead. Write the summary journal entry to record the added conversion costs to WIP-Bottling. Post the JE to the T account for WIP-Bottling above. 56,151 +68,629 = 124,780 overhead = 1374,340-1491736) 3X 1241780 =374,340-convosin cost = 224,604 3 40% of 374,340 - 149,736 Director 3) Process costing of second department: Follow the steps below to perform the costing analysis for the Bottling department. Refer to VPW 3 Packet for examples on how to complete the tables. a) Step 1 part 1: Account for physical units. Complete the tables below using ***NUMBER ### of units, NOT dollars!!!!!! Physical units for BOTTLING Units in Bottling June 1 44.000 Units completed and transferred 272/500 out during June Units transferred in from 12801500 Blending during June Units in Bottling June 30 52,000 Units to account for 324/ DO Units "accounted for" Note: the 3 row should be the first 2 rows added together. The units to account for" should equal the units "accounted for b) Step 1 part 2: Determine equivalent units. This is #WWWNUMBERW of units, NOT dollars!!! For each of the 4 cost categories for Bottling Department, complete the table below to determine the equivalent units. Hint: All units completed and transferred to Finished Goods" and units in "ending WIP-Bottling inventory" are 100% complete with respect to transferred in" costs (costs from Blending department) and bottle costs. Equivalent Units (ACCOUNTED FOR) Transferred in Other Materials (Blending costs) Bortles 52,000 52/000 33.800 Conversion 26/000 Equivalent units in ending WIP- Bottling inventory Equivalent units completed and transferred to Finished Goods" 272/500 272500 272/500 272/500 Total Equivalent units accounted for 324,500 3a4/500 306,300 298,500 Note: The 3 row should be the first two rows added together. The 3 row for "Other" and Conversion WILL NOT equal the other columns in this table, nor will they equal the 3 row in the table for step 1 in a) above. c) Step 2 part 1: Make sure you complete the table Determine Costs to account for. These are SSS$DOLLARSSSSS not number of units. Costs to account for" is the sum of the beginning WIP-Bottling balance plus the costs that would have been added/assigned to the WIP-Bottling department during June. This information is summarized in the table above. Complete the table below using the information provided above. Bottling Department: Summary of Costs to be accounted for WIP- Bottling Costs Added Total Costs to be Cost Category beginning during June accounted for Transferred in from Blending $ 55,000 314,160 from lb iv 369,160 Cost of Bottles 111,000 701,250 from 2bi 8121250 Other Material Costs 18,000 102 1650 Efrom 26 ir 120/650 Conversion Costs 80,500 374,340 from 2c 4541840 Total $ 264,500 1,492.400 11,756,400 Note: The costs "transferred IN" that were transferred into Bottling once "completed and transferred OUT" of the Blending department. d) Step 2 part 2: Calculate cost per equivalent unit. Answers will be SSSDOLLARSSS per ####NUMBER### of units. Use the totals in b) and e) above to calculate the Cost per equivalent unit for each cost category. Use 4 decimal places to minimize rounding differences. Cost per Equivalent Unit Other Material 120.650 Transferred in Cotal Costs to be accounted for 3(C) 369,160 Equivalent units 3(b) 324.500 Cost Per Equivalent Unit 1.1376 Bottle Costs 812 250 324,500 12.5031 Conversion 454,840 04300 7.5238 306 300 10.3934 e un e) Step 3: Allocate costs to units. Multiply the Cost per Equivalent for each cont category in step time the equivalent units for completed and transferred to Finished Goods and ending Inventory to complete the table below. ROUND YOUR ANSWERS TO NEAREST WHOLE DOLLARS. Add the cost categories together across to the Total Column. Total esch column to the bottom row costs accounted for". The total in the bottom right box should be the total of the numbers above it AND the total of the numbers to its left. (lit may be off a few dollars for rounding). Your answer represents SSSSDOLLARSS5555 not units. Round your answers to the nearest whole dollar Total WIP -Ending balance Costs of goods completed and transferred out Total Costs accounted for Transferred in 242,244 59,155 11,514,665 304,996 1.756,914 369,15 Other Material Bandles Costs Comwersion 139161 13,314 39619 821045 07:338 1415,236 812,256 120/652 454.855 Note: The total costs accounted for in the bottom row should equal (offfo Se for rounding the totals "costs to account for in the bottom row of the table in step 4) Sale of Finished Goods: Accounting for the analysis. As units are completed in the Bottling department, they are moved to Finished Goods Inventory where they are ready to be sold. The analysis above determines the dollar value of those completed units. a) Write the journal entry to move these costs from WIP-Botiling Inventory account to Finished Goods Inventory account. Post the JE to the WIP-Bottling and Finished Goods T-accounts attached at the end of the project Determine the ending balance for WIP-Bottling account. Balance should equal first row from table in 3e. Finbled goods inventory WIP- Bottling goods WIP efending 314,160 7011250 other matrol 102,650 DR 1514,665 CR WIP-Bolting 1,514,665 Bulbol 264,500 1,514,665 Finished Einsted goods Bul blo Bottles WIP byltingsluts conversion 374 340 Bult/70 1514.165 Bal6/30 242, 235 b) Assume the Finished Goods Inventory was zero at the beginning of June and zero at the end of Junc. How many units did they sell during June? c) If Sunspot Beverages, Ltd. sold cach unit for $12.00 what would their sales revenue be? Write the journal entry to record the sales revenue for June. d) How much is their expense (COGS)? Write the journal entry to record the COGS for June. Post this entry to the Finished Goods account attached at the end of the project. 5) Raw Material: The company uses no indirect material and the Raw Material Inventory began the month with $120,000 and ending the month with $98,000. How much raw material inventory did the company purchase during June? Write the summary journal entry to record the purchase. Post the journal entry to the T-account provided at the end of the attachment. Sunspot Beverages, Ltd., of Fiji uses the weighted-average method in its process costing system. It makes blended tropical fruit drinks in two stages. Fruit juices are extracted from fresh fruits and then blended in the Blending Department. The blended juices are then bottled and packed for shipping in the Bottling Department. The following information pertains to the operations of the Blending Department for June. Percent Completed Materials Conversion 700 400 Work in process, beginning Started into production Completed and transferred out Work in process, ending Units 56,000 290,500 280,500 66,000 750 251 Work in process, beginning Cost added during June Materials Conversion $ 19,100 $ 5,900 $ 205,300 $ 124,780 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's equivalent units of production for materials and conversion in June. Materials Equivalent units of production Conversion 297,000 330,000 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost per equivalent unit for materials and conversion in June. (Round your answers to 2 decimal places.) Cost per equivalent unit Materials Conversion 0.68 $ 0.44 Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost of ending work in process inventory for materials, conversion, and in total for June. (Round your intermediate calculations to 2 decimal places.) Materials Conversion Total Cost of ending work in process 33,660 $ 7,260 inventory 40,920 S Required 1 Required 2 Required 3 Required 4 Required 5 Calculate the Blending Department's cost of units transferred out to the Bottling Department for materials, conversion, and in total for June. (Round your intermediate calculations to 2 decimal places.) Materials Conversion Total Cost of units completed and transferred out $ 190,740 $ 123,420 $ 314,160 Required 1 Required 2 Required 3 Required 4 Required 5 Prepare a cost reconciliation report for the Blending Department for June. (Roun places.) Blending Department Cost Reconciliation Costs to be accounted for: Cost of beginning work in process inventory$ 25,000 Costs added to production during the period 330,080 Total cost to be accounted for $ 355,080 Costs accounted for as follows: Cost of ending work in process inventory $ 40,920 Cost of units completed and transferred out 314,160 Total cost accounted for $ 355,080