Answered step by step

Verified Expert Solution

Question

1 Approved Answer

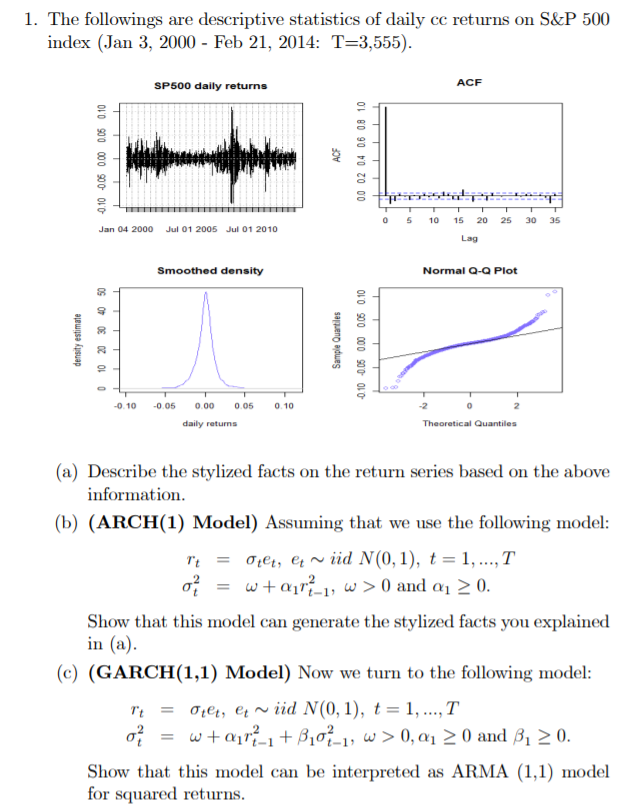

Need help with (a)(b)(c). 1. The followings are descriptive statistics of daily ce returns on S&P 500 index (Jan 3, 2000 - Feb 21, 2014:

Need help with (a)(b)(c).

1. The followings are descriptive statistics of daily ce returns on S&P 500 index (Jan 3, 2000 - Feb 21, 2014: T=3,555). ACE SP500 daily returns OIO 900 000 900 OFC 0.0 0.2 0.4 0.6 0.8 1.0 0 5 10 15 20 25 30 35 Jan 04 2000 Jul 01 2005 Jul 01 2010 Lag Smoothed density Normal Q-Q Plot 50 40 30 density estimate Sample Quantiles OL0 900 000 900010 20 10 0 -0.10 0.05 0.00 0.05 0.10 daily returns Theoretical Quantiles (a) Describe the stylized facts on the return series based on the above information. (b) (ARCH(1) Model) Assuming that we use the following model: Tt = 0tet, et ~ iid N(0,1), t = 1, ..., T 07 = w + Qur{-1, w >0 and au > 0. Show that this model can generate the stylized facts you explained in (a). (c) (GARCH(1,1) Model) Now we turn to the following model: rt = 040t, et ~iid N(0,1), t = 1, ...,T o = w+Q1r7-1 + 3102-1, w > 0,01 > 0 and Bi > 0. Show that this model can be interpreted as ARMA (1,1) model for squared returns. 1. The followings are descriptive statistics of daily ce returns on S&P 500 index (Jan 3, 2000 - Feb 21, 2014: T=3,555). ACE SP500 daily returns OIO 900 000 900 OFC 0.0 0.2 0.4 0.6 0.8 1.0 0 5 10 15 20 25 30 35 Jan 04 2000 Jul 01 2005 Jul 01 2010 Lag Smoothed density Normal Q-Q Plot 50 40 30 density estimate Sample Quantiles OL0 900 000 900010 20 10 0 -0.10 0.05 0.00 0.05 0.10 daily returns Theoretical Quantiles (a) Describe the stylized facts on the return series based on the above information. (b) (ARCH(1) Model) Assuming that we use the following model: Tt = 0tet, et ~ iid N(0,1), t = 1, ..., T 07 = w + Qur{-1, w >0 and au > 0. Show that this model can generate the stylized facts you explained in (a). (c) (GARCH(1,1) Model) Now we turn to the following model: rt = 040t, et ~iid N(0,1), t = 1, ...,T o = w+Q1r7-1 + 3102-1, w > 0,01 > 0 and Bi > 0. Show that this model can be interpreted as ARMA (1,1) model for squared returnsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Innovation And Technology

Authors: Nikos Vernardakis

1st Edition

0415676800, 978-0415676809