Answered step by step

Verified Expert Solution

Question

1 Approved Answer

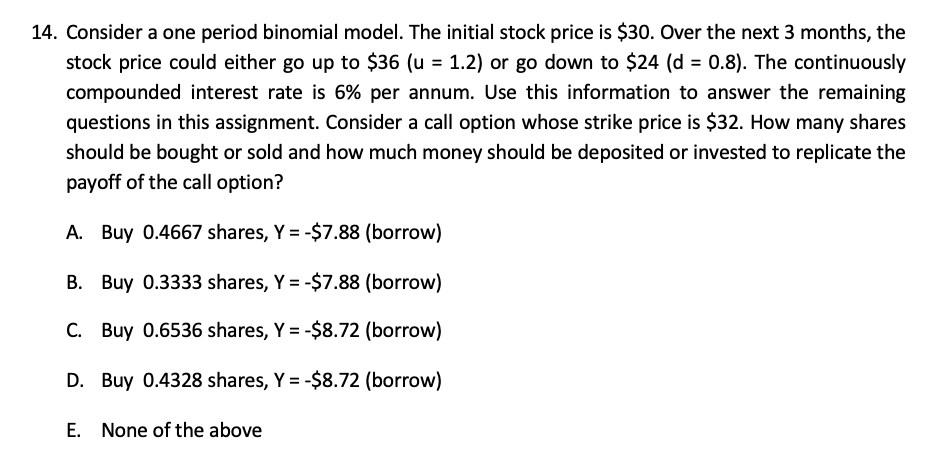

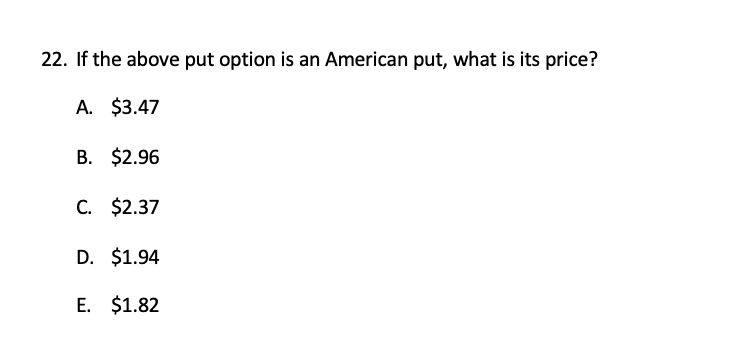

NEED HELP WITH ALL QUESTIONS PLEASE!!!!! 14. Consider a one period binomial model. The initial stock price is $30. Over the next 3 months, the

NEED HELP WITH ALL QUESTIONS PLEASE!!!!!

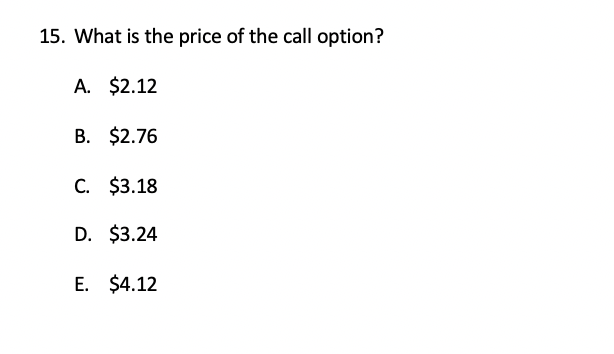

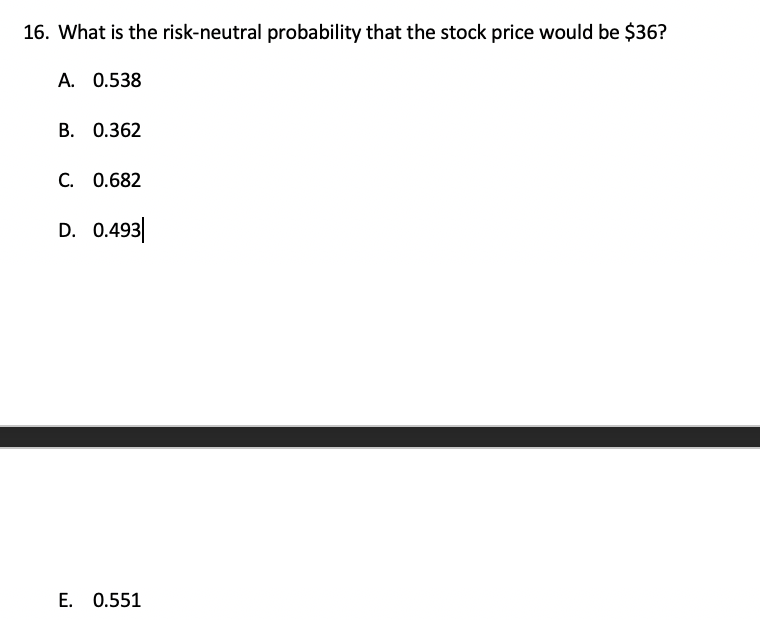

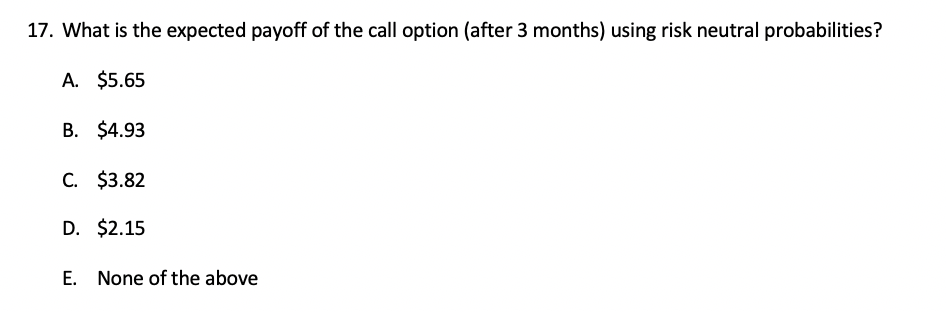

14. Consider a one period binomial model. The initial stock price is $30. Over the next 3 months, the stock price could either go up to $36 (u = 1.2) or go down to $24 (d = 0.8). The continuously compounded interest rate is 6% per annum. Use this information to answer the remaining questions in this assignment. Consider a call option whose strike price is $32. How many shares should be bought or sold and how much money should be deposited or invested to replicate the payoff of the call option? A. Buy 0.4667 shares, Y = -$7.88 (borrow) B. Buy 0.3333 shares, Y = -$7.88 (borrow) C. Buy 0.6536 shares, Y = -$8.72 (borrow) D. Buy 0.4328 shares, Y = -$8.72 (borrow) E. None of the above 15. What is the price of the call option? A. $2.12 B. $2.76 $3.18 D. $3.24 E. $4.12 16. What is the risk-neutral probability that the stock price would be $36? A. 0.538 B. 0.362 C. 0.682 D. 0.493 E. 0.551 17. What is the expected payoff of the call option (after 3 months) using risk neutral probabilities? A. $5.65 B. $4.93 C. $3.82 D. $2.15 E. None of the above 18. Suppose you wish to form a risk free portfolio by selling a call and buying a certain number of shares. How many shares should be bought for every call sold? A. 0.6240 B. 0.5813 C. 0.4212 D. 0.3333 E. 0.2128 19. Now consider a two period binomial model. Use the same information as in question 16 but now the call option expires after 3 + 3 = 6 months. What is the price of the call option? A. $2.28 B. $2.62 C. $3.14 D. $3.92 E. $4.27 20. Consider a European put option using the one period binomial model as in question 16. The strike price of the put is $28. What is the price of the put option? A. $1.82 B. $2.14 C. $2.63 D. $3.87 E. $4.12 21. Consider a two period binomial model using the information in question 16. The put option is will expire after 3 + 3 = 6 months. What is the price of the European put option with a strike price of $28? A. $3.47 B. $2.96 $2.37 $1.94 E. $1.82 22. If the above put option is an American put, what is its price? A. $3.47 B. $2.96 cu w C. $2.37 D. $1.94 E. $1.82Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

AI In The Financial Markets

Authors: Federico Cecconi

1st Edition

3031265173, 978-3031265174